Innovative Economy: Analysis And Management Of Business-Processes On Sales Funnel Concept

Abstract

The innovative economy today makes adjustments not only in the activities of high-tech enterprises, but also in the daily life of all economic entities. The events of 2020 served as a catalyst for the development of digital methods, revealing significant shortcomings of conservative approaches to the analysis and management of enterprise business processes. The sales funnel is one of the most popular tools for analyzing and managing the sales process of a business. It has received a lot of practical coverage both abroad and in Russia due to its undeniable advantages: reliability, ease of compilation and use, relevance, effectiveness against the background of low costs for its operation, which is provided thanks to digital services. Using this tool, it is possible to significantly increase the efficiency of the sales process, ensure more efficient use of enterprise resources, and increase the profitability and competitiveness of the business. At the same time, excessive popularization and commercialization of this concept is dangerous for its existence and development, since in the dynamic world of high-tech ideas, as a rule, there is a process of skimming the cream and switching attention to other, no less promising ideas and developments. Therefore, this concept can be considered not only as a marketing tool, but as a conceptual approach to the analysis and management of key business processes of an enterprise, moreover that the current level of technology development allows to do this.

Keywords: Business analysisconversionfinancial analysissales analysissales funnel

Introduction

A sales funnel is a marketing concept model that describes all stages of the sales process, taking into account the number of remaining and retired customers, which allows to correlate the number of people who received information about a product or service with the number of end customers (Banerjee & Bhardwaj, 2019).

The concept of a sales funnel is extremely popular today and is actively developing both in practice and in theory. software products are being developed that are integrated into modern CRM systems and function separately from them. The current popularity of this concept does not mean that it was developed in the current environment. On the contrary, its origins date back to 1896, the first attempt at modeling was made in 1921 (the AIDA (Attention-Interest-Desire-Action) model, and in 1959 this process was graphically illustrated in the form of a funnel (Kolosova, 2019). Nevertheless, it has only just been actively developed. This was made possible by universal automation, the penetration of information technologies into the mass segment, and the availability of technologies for small and medium-sized businesses.

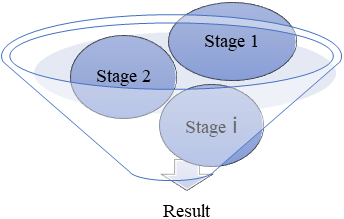

Most of the ready-made solutions in the methodology of applying this concept are concentrated in the field of e-commerce and agency sales systems, or where the individual service model is used and it is possible to record all stages of transformation of a potential client into a buyer. Nevertheless, in methodological terms there is quite a lot of questions and blank spots, especially in the retail offline trade, which today also stands on rails automation and informatization, which is, unfortunately, not as request business efficiency tools, and as the following of legal orders. The classic schematic representation of the sales funnel is shown in Figure

Source: authors.

Stage 1-initial familiarization of the population with the offer of a specific seller of goods or services (advertising in the media and the Internet, outdoor advertising). The maximum capacity of the stage includes both those for whom the information is relevant and those who do not need this information;

Stage 2 - initial contact of the interested part of the population with the seller (phone call, social media appeal, visit to the store). The capacity of the stage is wide and consists of customers who are interested in the product or service, but do not yet have accurate ideas and wishes;

Stages i - a set of stages of interaction with potential customers that precede the transaction: informing, demonstrating, selecting convenient lending programs, documenting the purchase, and so on. It requires creating maximum informational, aesthetic and economic comfort for the client.

Result - the fact of the transaction, characterized by the final fulfillment of the parties obligations.

The development of a sales funnel, its formation has already become a very common recommendation for existing businesses, as well as a very highly paid service of various consultants and business coaches. Of course, a significant breakthrough in this concept was made solely due to the development of information technologies and online commerce, and the replication of this concept is due to the active formation of online sales segments by representatives of small and medium-sized businesses. Excessive practical interest in this concept, its replication and popularization can seriously narrow the boundaries of its application and do not provide an opportunity to develop into an independent scientific direction. Understanding that only a certain percentage of the original customers reach the result (actually completed purchase and sale transaction) is also characteristic of considering this issue from the position of principle, which states that 80% of the effort accounts for only 20% of the result. Based on this fundamental principle, the concept of a sales funnel can be considered as a promising scientific direction. In this regard, the sales funnel is really able to indicate the places of maximum "narrowing", i.e. the maximum loss of efficiency.

This illustrates the application of the sales funnel as a process management tool. At the same time, the formation of a sales funnel can be considered as the result of economic and mathematical modeling of the sales process, which is necessary for its formal detailing and analysis in order to identify the full range of factors and assess their impact on the resulting one.

In the most abstract form, it is possible to present the economic model of the sales funnel in its natural form:

where

NP - the number of purchases made in physical terms;

k1,...,n-1 - percentage of potential customers who have moved on to the next stage, including the transaction completion stage (conversion);;

kn - percentage of customers who have concluded a transaction, fulfilled their obligations and have no claims against the supplier (performer).

The model of the sales funnel in value form can be represented as follows:

where:

R - revenue

AR- average receipt, a calculated indicator obtained as the arithmetic mean of sales made by the seller.

A careful study of practical recommendations for the formation of a sales funnel at a particular enterprise allowed us to conclude that most of the methods determine the final stage (result) of the sales process - the conclusion of a transaction. In turn, the author's position is that this approach is wrong and does not reflect the goal of the company as a whole, but only what is within the competence of the sales Department. Thus, this reduces the significance of the concept, the usefulness of the results obtained, and hinders the improvement of the efficiency and competitiveness of activities. Correction of the identified defect is possible if the final stage is the full fulfillment (actual and documented) by the parties of all their obligations. This allows you to more fully and in detail present the costs and financial losses of each stage, determine the scale of their impact on the financial result, as well as their effectiveness.

Problem Statement

The sales funnel is not only a marketing tool that allows to increase sales of the company, or an element of control over the work of the sales department. The analytical application of the sales funnel is much more diverse. So, from the point of view of the study, the sales funnel can be considered as a tool for:

–managing the sales process with setting specific KPI for performers that characterize not only the quantitative aspect of interaction between the manager and the buyer, but also the quality (depth) of this interaction;

–increase profits by reducing commercial expenses, which is the result of a more efficient expenditure of the marketing budget, which it is possible to direct to solving problems that worsen a specific component of the sales process;

–increase the efficiency of the sales process through the use of more targeted sales (marketing) activities;

–forecasting the volume of revenue from sales, as well as the future financial result;

–identify reserves for increasing sales by increasing the conversion rate of each stage.

Moreover, the principle underlying the sales funnel concept can be applied not only to analyze and manage the sales process, but also to most of the company's key processes.

Research Questions

The problem posed to the research requires answers to questions in several directions:

- what quality KPI are necessary for analytical support of decision-making in the innovative economy?

- what expenses are specific to a particular stage of the product sales process?

- what influences the conversion rate of each stage of the sales process?

- how suitable are the data obtained during the analysis of the sales funnel for forecasting?

- in what other business processes can the principle underlying the sales funnel be applied?

Thus, the key tasks facing the research can be distributed in the following planes:

1. "Vertical" research of all the properties of the sales funnel as an analytical tool used to improve the sales process, which implies improving and deepening the methodological tools.

2. "Horizontal" research of all directions and processes in which the principle underlying the sales funnel can be applied. In other words, it is necessary to identify how applicable the "funnel" principle is in the analysis of business processes of an enterprise.

Purpose of the Study

The purpose of the research is to develop methods for forming and analyzing the sales funnel, develop approaches to the formation of comprehensive balanced KPIs that quantitatively and qualitatively reflect the sales process of the enterprise (Huarng et al., 2018). This is necessary not only to increase the efficiency of the company's sales efforts and commercial expenses, but also as a leading indicator in the context of forecasting the company's performance. This direction is in highly demand by enterprises today. Also, the research is supposed to formulate the principle of business process funnel, which reflects the conversion of each stage of business activity, assesses the losses and costs of each stage, and develops recommendations for increasing the efficiency of business activities. Potential applications of this concept include analysis of production processes and financial analysis. Improving the efficiency of business processes by increasing the conversion rate of the transition to the next stage of the process will ultimately help to increase the return on resource use, adjust approaches to business management, and increase profitability. This is a necessary element of increasing competitiveness in an innovative economy that allows many small businesses to compete effectively with market leaders, providing a level playing field in communication with consumers.

Research Methods

The key research method is the abstraction method, which allows formalizing business processes for their conceptual description, as well as for forming economic and mathematical models necessary for analysis and management of the enterprise. Since the sales funnel principle was widely used due to the development of digital technologies, the first companies to apply this method in practice are just innovative enterprises that in many ways had to not compete for the consumer, but, on the contrary, form a need. This largely explains the attention paid to conversion losses in this concept.

An in-depth study of the sales funnel as an analytical tool was conducted using the following methods:

- development of mathematical models that reflect the principle of forming a sales funnel;

- conceptual description of the generated models;

- abstracting and identifying risks that reduce conversion when switching between different stages;

- formation of forecast models based on the sales funnel to assess future revenue and profit, which is associated with the development of a system of leading and lagging indicators;

- development of methodological prerequisites for finding reserves for increasing sales using information generated within the sales funnel.

methodological development of applying the "funnel" principle to other key business processes of the enterprise involves the following elements:

- conducting a survey of representatives of innovative enterprises in order to identify the relevance of extrapolating the funnel principle to key business processes;

- identification of potential applications of the funnel approach in the management of innovative enterprises.

Findings

As noted above, one of the key aspects of this research is the development of a mechanism within the sales funnel that increases the efficiency of efforts and resources (including commercial expenses) spent on the functioning of the sales process. Optimizing the costs of each stage of the sales process is usually not the responsibility of employees in sales departments that are revenue centers, not profit centers. In this case, the sales funnel shows its potential as not only a marketing tool, but also a comprehensive tool for managing all enterprise processes, with the ability to develop and approve sets of key performance indicators (KPI).

Thus, it is advisable to evaluate the cost effectiveness for each stage in the sales funnel using the coefficient of elasticity of changes (Ei) using the formula:

where:

Ei-elasticity of change of the i-th stage

∆ ki - growth rate (in %) of the share of potential customers of the i-th stage

∆ pi - growth rate (in %) of expenses for increasing the conversion of the i-th stage.

In cases where the value of the elasticity coefficient exceeds 1, expenses for the considered stage of the sales funnel are appropriate if they are equal to or less than one - expenses are not able to bring the desired effect. In the Table

Source: authors.

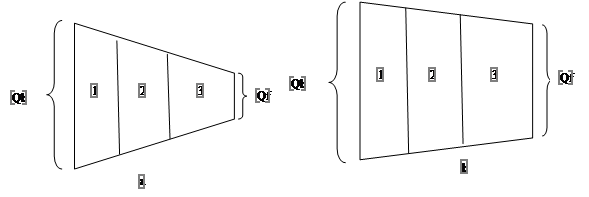

Thus, a more detailed presentation of information contributes to an integrated approach to resource allocation and ensuring maximum efficiency of their use. Therefore, the use of this tool is advisable not only from the point of view of increasing sales, but also to ensure the efficient use of enterprise resources, which will increase the profitability of the business and its competitiveness. The effectiveness of managing the sales funnel is to reduce customer losses during the transition from one stage to another.in terms of relative indicators, this is reflected in the form of increasing conversion rates for each stage, and graphically - reducing the angle of narrowing of the funnel. In Figure

Source: authors.

The classic scheme of an inefficient sales funnel looks like a large number of incoming customers / resources (Qb) and a significantly smaller amount of the final result (Qf). It is possible to describe an inefficient sales funnel in the following way:

Qb - Qf → + ∞

or

→ 0

An effective sales funnel is represented by a figure in which the significant difference between incoming resources and the final result is minimal, which can be described as follows:

Qb - Qf → 0

or

→ 1

KPI determination is an important element not only in the enterprise management process, but also in the analysis of its activities (Pérez-Álvarez et al., 2018). As part of the analysis of e-commerce, which is inherent in most innovative enterprises, a fairly wide set of indicators has been formed, which in business practice is called the KPI metric. In most cases, data is collected and processed automatically using the built-in counters and metric tracking services, the most popular of which are Yandex.Metrix and Google.Analytics. Modern services allow not just collect large amounts of data about customers in general: the total number of visitors to the resource, the number of formed baskets, completed purchases, bounces, the average time on the web-site, and generate "heat" maps, i.e. site locations that are most attractive to visitors. Most of these indicators are absolute and have a quantitative assessment that characterizes customers as a whole. This approach is the basis for the functioning of the sales funnel.

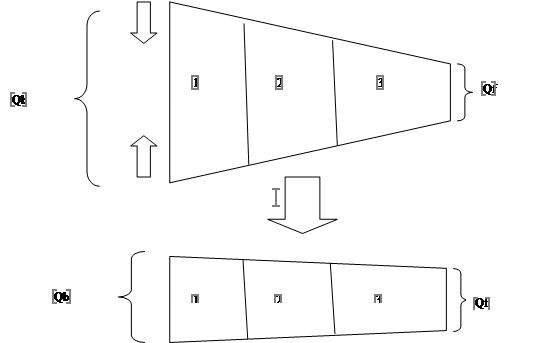

However, it is worth noting that the modern development of technology allows to record and analyze not only aggregated data, but also personalized data, due to the ability to track the IP addresses of customers, or in the establishment of accounts on the resource. This provides an opportunity, first of all, for the sales departments of the enterprise to increase business revenue by offering more relevant products and services to the client, as well as to save resources by minimizing the cost of working with customers who have a low conversion rate and for whom the product or service is irrelevant. Thus, there is a first approach to improving the efficiency of the sales funnel and increasing the company's profit by reducing the array of processed information and specializing in a small number of ready-to-deal and loyal customers, which is schematically shown in Figure

Source: authors.

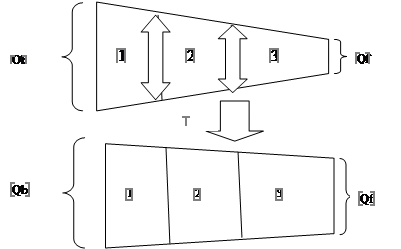

According to Figure

Source: authors.

In the Figure

The second area of research - the formation of the "funnel" principle and its adaptation to other business processes of the enterprise should be considered through the prism of a survey conducted by the authors using the Google Forms service, whose respondents were 75 representatives of small innovative businesses in the Samara, Nizhny Novgorod regions and the Republic of Tatarstan. The formulated question: "Where do you think the main bottlenecks of the company's business processes are?", the survey results should be presented in the form of an analytical Table

Thus, according to the survey, most of the problems of business processes lie in the area of subjective internal problems that the enterprise has the ability to influence. Also, the survey revealed that the key problem is low productivity, which is associated with either the labor resources or the technologies and resources used. This information can be considered as a request from business representatives to expand the methodological functionality of the funnel principle to other key business processes. Thus, the funnel principle can be considered in the context of analyzing existing fixed assets that are directly involved in the production process and form the capital return of the entire business (Lu, 2017). However, the existing equipment is only an integral part of the installed equipment, and it, in turn, is part of the existing equipment of the enterprise. Considering this issue from the perspective of the information obtained in the analysis of figures

Also very interesting from a methodological point of view is the expansion of the financial analysis apparatus due to the "funnel" principle. For example, a statement of financial results prepared in accordance with both Russian and international financial reporting standards implies the following chain, which has a logical connection, but, unlike other processes considered, stochastic: "gross profit - profit from sales - profit before tax - net profit". In this context, it is also possible to identify gaps between stages, identify factors that affect the size of deviations and make decisions aimed at reducing the impact of negative factors, which ultimately leads to an increase in the result indicator-net profit.

Conclusion

The main conclusions of the study include the following:

- despite the fact that the first works in the field of forming the sales funnel methodology were published more than 100 years ago, this concept has gained popularity only today, when the necessary technological base was formed;

- wide practical application, popularization for the purpose of commercialization of the sales funnel without adequate fundamental methodological study by the scientific community, carries great risks for the concept under consideration;

- describes mathematically and graphically the situation of an effective and inefficient sales funnel;

- formulated key directions for improving the efficiency of the sales funnel;

- proposed indicators that characterize the sensitivity of each stage of the sales process to changes in its costs, which allows us to judge the feasibility of applying certain measures;

-the necessity of adapting the funnel principle not only for analyzing the company's sales, but also for other key business processes is justified;

- the funnel approach to the analysis of the efficiency of the use of fixed assets of the enterprise, as well as financial results, is considered.

An approach to analyzing and managing key processes from the perspective of the funnel principle helps to increase resource efficiency, reduce costs, and increase profits and business competitiveness, which is the main condition for survival in an innovative economy. Currently, the results of the study are more relevant to modern innovative enterprises that operate in online channels using CRM systems, which allows you to collect and analyze information without unnecessary costs and without significant time and resource costs. There is no practical possibility of implementing the considered proposals at conservative offline enterprises that only keep accounting records, due to the lack of information collected. Further areas of research are planned to deepen the consideration of the conceptual foundations of the funnel principle, the ability to apply them to most business processes of the enterprise. The innovative economy is seriously tightening competition, and the issues of limited resources are extremely relevant today. Information becomes a key resource, a source of increasing competitiveness, and a driver for implementing changes. The development of modern technologies allows us to put into practice many of the theoretical developments of the past years, which not only have not lost their relevance, but on the contrary, are gaining international popularity.

References

- Banerjee, S., & Bhardwaj, P. (2019). Aligning marketing and sales in multi-channel marketing: Compensation design for online lead generation and offline sales conversion. Journal of Business Research, 105, 293-305.

- Hassani, F., & Gahnouchi, S. A. (2017). A framework for business process data management based on big data approach. Procedia Computer Science, 121, 740-747.

- Huarng, K.-H., Rey-Martí, A., & Miquel-Romero, M.-J. (2018). Quantitative and qualitative comparative analysis in business. Journal of Business Research, 89, 171-174.

- Kolosova, V. (2019). Mechanism for building an effective marketing strategy based on the use of a digital sales funnel. Vestnik Moscow Region University, Series: Economics, 1, 43-51.

- Lu, Y. (2017). Industry 4.0: A survey on technologies, applications and open research issues. Journal of Industrial Information Integration, 6, 1-10.

- Pérez-Álvarez, J. M., Maté, A., Gómez-López, M. T., & Trujillo, J. (2018). Tactical business-process-decision support based on KPIs monitoring and validation. Computers in Industry, 102, 23-39.

- Pokki, H., Virtanen, J., & Karvinen, S. (2018). Comparison of economic analysis with financial analysis of fisheries: Application of the perpetual inventory method to the Finnish fishing fleet. Marine Policy, 95, 239-247.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

30 April 2021

Article Doi

eBook ISBN

978-1-80296-105-8

Publisher

European Publisher

Volume

106

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1875

Subjects

Socio-economic development, digital economy, management, public administration

Cite this article as:

Grabozdin, Y. P., Denisova, O. N., & Tatarovsky, Y. A. (2021). Innovative Economy: Analysis And Management Of Business-Processes On Sales Funnel Concept. In S. I. Ashmarina, V. V. Mantulenko, M. I. Inozemtsev, & E. L. Sidorenko (Eds.), Global Challenges and Prospects of The Modern Economic Development, vol 106. European Proceedings of Social and Behavioural Sciences (pp. 1439-1449). European Publisher. https://doi.org/10.15405/epsbs.2021.04.02.171