Accounting Curriculum in the Sustainbility Era: Employability of Future Accountants

Abstract

This paper discusses the issues surrounding the accounting curriculum when taking into account the sustainability era. It presents the concerns raised by employers about the need to maintain, revise, or improve the accounting curriculum to keep it relevant. This paper discusses the skills needed by future accountants in terms of hard and soft skills and the concept of human capital for future accountants. Specifically, the hard skills include content syllabus covering topics such as corporate reporting, ethics, and technologies applicable to financial reporting whilst the soft skills include communication, leadership, problem solving and critical thinking. Therefore, this paper suggests revising the accounting curriculum in order to enhance the graduates’ employability so they can sustain themselves in the sustainable era. The findings shed light on the attempts to comprehend the challenges and employability of future accountants within the context of Malaysia as an emerging market and from the perspective of a developing country. This paper also contributes to the body of knowledge by extending the existing literature and providing a better understanding of the prevalent issue.

Keywords: Accounting Education, Expectation Gap, Employability, Sustainability

Introduction

In the last three decades, Malaysia has experienced remarkable economic growth. Additionally, the thriving education industry contributes to the national economy. Therefore, Malaysia must continue to invest in human capital in order to attain a sustainable development trend. The astronomical increase in the number of higher education institutions (HEIs) over the past 15 years is proof that the government has focused its investment efforts on the education sector thus far, particularly the higher education sector (Reza, 2016). Along with the aspiration for sustainability, Education for Sustainable Development (ESD) has been adopted and steered by the United Nations (Boeve-de Pauw et al., 2015), with the aim of instilling the concept of sustainable development in the minds of society and fostering the best practises and attitudes towards the environment. Numerous nations throughout the globe have incorporated ESD into their educational systems.

In the realisation that the world must progress towards sustainability, Malaysia has also significantly contributed to the implementation of education for sustainable development to instil knowledge, values and attitudes among graduates as the future leadership rests in their hands. However, despite the establishment of accounting learning, HEIs have been criticised for failing to effectively respond to the sustainability agenda (Hommel et al., 2013). The criticism ranged from their failure to prepare professionals for the future (Cornuel, 2007) to their failure to address societal issues such as sustainability (Snelson-Powell et al., 2016; Wall et al., 2017).

The findings of a study conducted by Rahman et al. (2007) demonstrate evidence suggesting that the higher institutions in Malaysia also have failed to emphasize the necessity of abilities demanded by the marketplace in a comprehensive manner. As a consequence of this, graduates in accounting are being provided with an insufficient amount of knowledge and skills, which potentially brings a negative impact on the employability. Among others, studies by (Ghani et al., 2018; Howcroft, 2017; Heang et al., 2019) also yield similar result, which further strengthen the claim on the unsettling gaps that potentially exists between employers and educators.

Therefore, this paper presents the challenges in the integration of sustainability and the expectation gap between employers and the current education curriculum amidst the sustainability era. This paper helps shed light on the attempt to comprehend the challenges and employability of future accountants within the context of the skills required by graduates. It also explores how well the current education curriculum fits in with the changing requirements and expectations of the accounting profession. As they seek to educate professionals and maintain their relevance in the 21st century, HEIs must consider these questions and issues.

The remaining sections of this paper are organised as follows: Section 2 explains the development of the sustainability era in Malaysia, followed by Section 3, which highlights the challenges of integrating sustainability into education. Section 4 presents the mismatch between the employers’ expectations and the qualities of the fresh graduates produced. Section 5 entails a discussion on the skill expectation gaps between the employers and the HEIs. The final section, Section 6, concludes this paper.

Development Of Sustainability Era And The Accounting Profession In Malaysia

The year 1987 marked the introduction of the first sustainable development report in Malaysia. In 2006, the Corporate Social Responsibility (CSR) reporting framework, which incorporates corporate social involvement and the implications of business operations on the environment and society, further bolstered the efforts. It was then succeeded in 2015 by the Sustainability Framework, which integrates firms' disclosure across three primary pillars: environmental, social, and governance (ESG) practises (Wan Mohammad & Wasiuzzaman, 2021). Throughout the years, Malaysia has further placed sustainability at the forefront of its national focus with numerous initiatives as well as the policies as set out in Table 1.

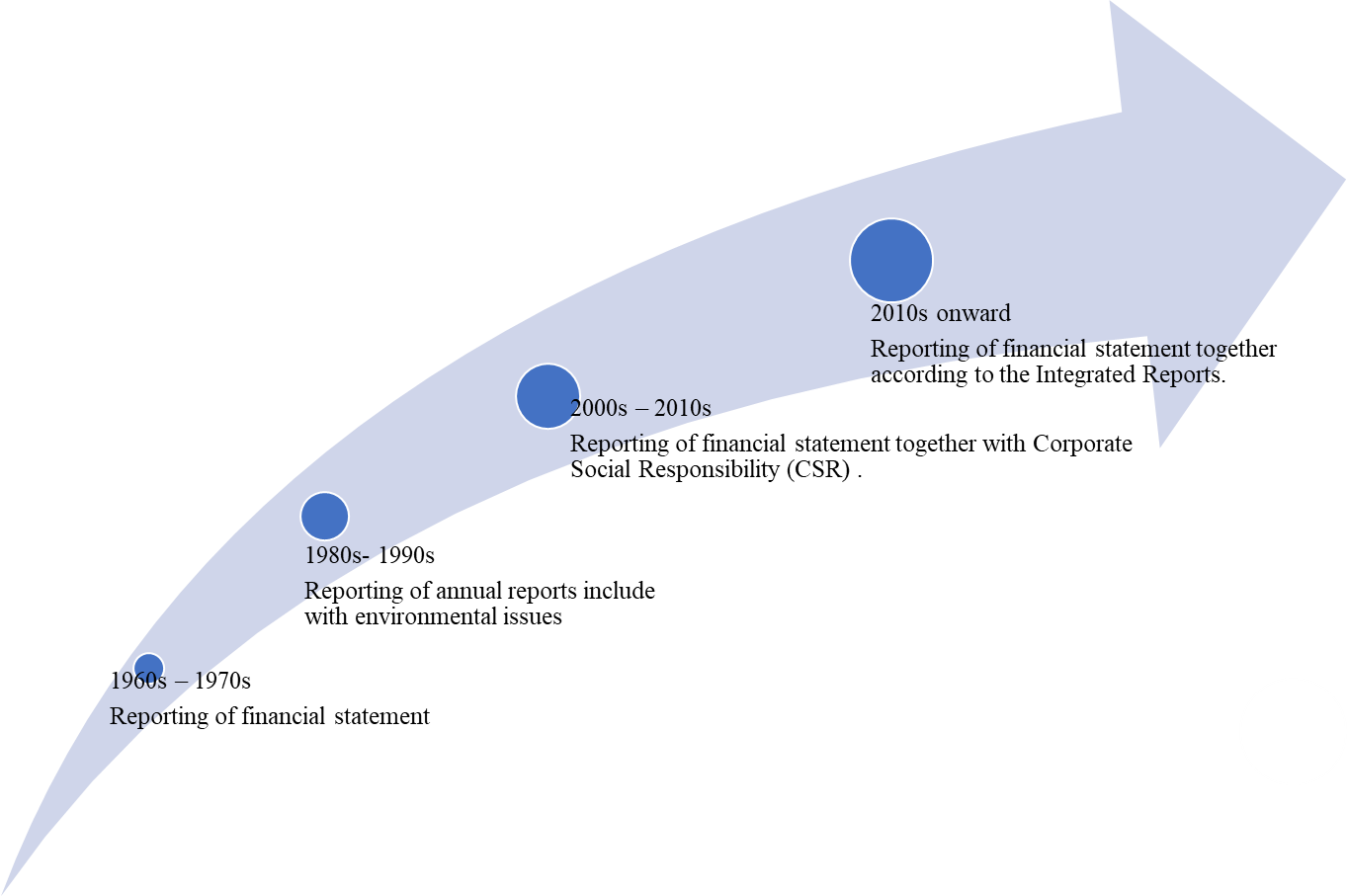

As the environment in which accounting is practised evolves in response to changes in the business landscape and demands from stakeholders, the demand for novel competencies among accounting graduates has been extensively discussed (Rahman et al., 2007). As illustrated in Figure 1, financial reporting has also evolved over the last fifty years from a solely financial statement perspective to a model that addresses internal and external issues of governance and sustainability in corporate social responsibility reports (Lusher et al., 2012).

In line with the advancement of the business landscape, there has been a corresponding increase in the requirements placed on professional accountants. They will require the competences, skills, and perspective that will enable them to fulfil the growing demand for information that is both comprehensive and forward-looking, as well as the growing demand for more frequent ad hoc reporting from a broader range of stakeholders (Association of Chartered Certified Accountants, 2018). HEIs play a crucial role in the process of acquiring and developing these competencies. They are the ones who have been charged with the responsibility of revising the accounting curriculum in order to incorporate the skills that the market expects accounting professionals to have (Carvalho & Almeida, 2022). HEIs should design their programmes in such a way that graduates achieve an intermediate level of proficiency in four different professional skill sets. These skill sets are organisation, personal, interpersonal, communication, and intellectual, as set in the latest framework of the Malaysia Institute of Accountancy (MIA) Competency Framework. However, Peeters et al. (2019) noted that HEIs’ responsibilities to equip graduates with the appropriate knowledge and skills are fraught with obstacles.

Challenges In Sustaining Accounting Education

According to Hanapi and Nordin (2014), human capital is the value that is placed on the capabilities and knowledge of a workforce, and it plays a crucial part in deciding whether or not a nation is successful economically. In a similar vein, the Malaysian Ministry of Higher Education (MOHE) also asserted that having high-quality human capital is crucial for the nation's sustainable economic development and stability (Ngoo et al., 2015). Singh et al. (2013) argued that employees are required to maintain a current knowledge of global economics in light of the dynamism of the labour market and the technological improvement that has occurred in recent years.

Education has generally been seen as the cornerstone of a flourishing society. Therefore, the accounting curriculum must equip graduates with not just the required competence and certificates but also the understanding to use those skills. Complementarily, it ought to provide students with the knowledge, the ability to engage in critical thinking, and the ethics that are required to make the most appropriate decisions at the appropriate times (Bressler & Pence, 2019). Nevertheless, the establishment of accounting learning standards with the purpose of elevating the standing and credibility of accounting as a profession and discipline continues to be criticised for producing graduates who are ill-equipped to meet current and emerging industry demands and employer needs (Williams et al., 2019).

In light of the present changes in the financial reporting landscape, ESD has been gaining traction and taking place around the globe. However, it must be noted that there is still a minimal level of integration of sustainability in education due to its challenges. It is possible that the intrinsic complexity of sustainable development is one of the reasons why it has not yet made its way into mainstream academics and the administration of higher education institutions (HEIs). Sustainable development involves systemic change in addition to adaptation (Bauer et al., 2018). Therefore, taking the challenge of sustainability education seriously will increase conflicts, obstacles, and, consequently, complexity.

Failure to recognise the need for change is one of many barriers pertinent to both individual and organisational change (Foley, 2020). If educators do not comprehend and value the need for change, their desire to maintain the present state will prevail over their willingness to embrace changes. Fullan (2001) and Greenberg and Baron (2000) also found that disruption in instructional practises can result in a dread of the unknown due to habit and a sense of security from doing things in a familiar manner. Rather than developing new skills and accepting these changes, it is simpler to continue teaching in the same manner (Foley, 2020).

According to studies by Giesenbauer and Müller-Christ (2020), international rankings and leadership in specialised fields play a major role in determining the success of HEIs. Therefore, the advancement of interdisciplinary topics such as sustainable development would be frequently compromised. Mburayi and Wall (2018) suggested that faculty compensation systems that do not appropriately acknowledge skills in the field of sustainability had a detrimental influence on the faculty's dedication to research and development in this area. It is also possible that faculty resistance stems from the fact that widely accepted research metrics, such as journal rankings and impact factors, do not adequately recognise sustainability research (Hopkins et al., 2017). In addition, sustainability is an ethical topic, and Rasche et al. (2013) asserted that ethics cannot be taught.

Employability Of Future Accountants

Generally, the term "employability" refers to an individual's capacity to seek and retain a job that satisfies their needs (Hillage & Pollard, 1998). In a broader sense, employability can be defined as the capacity to navigate the labour market in an independent manner in order to realise one's potential through employment. According to Azmi et al. (2018), personal attitudes and attributes that reflect a person's capacity to acquire desired work and be competitive in their career are also defined as employability, while Azmi et al. (2018) briefly explained employability as work readiness skills. Likewise, studies from Smith et al. (2013) and Yorke and Knight (2006) also further described employability as the collection of skills, knowledge, experiences, and personal characteristics that increase a person's likelihood of obtaining employment in their desired field.

"Employability" in the workplace and labour market refers to the possibility that a person will be recruited by an organisation because their capabilities match the demands and expectations of prospective employers (Azmi et al., 2018). Notably, the identification of 'employability' as 'employment rate' is strengthened by the fact that several governments, like the United Kingdom and Malaysia, have utilised employment rate as a criterion for judging universities' effectiveness in boosting employability. As a result, several academics have referred to 'employability' as 'employment rate' in their study.

The concept of employability has garnered a great deal of scrutiny from policymakers, academics, and practitioners, and it has been studied in numerous disciplines such as employment development, education, management, and psychology (Vanhercke et al., 2014). Smith (2010) and Peeters et al. (2019) classified employability into two distinct categories: (1) human capital, which refers to generic skills and work experiences (Clarke, 2018), and (2) social capital, which refers to the reputation and ranking of HEIs themselves together with one’s personal networks (Succi & Canovi, 2020). It must be noted that this paper focuses only on human capital as it seeks a better understanding of the skills gaps. Table 2 simplifies the concept of employability based on the concept of human capital.

Given that Malaysia is also undergoing significant technological change and is currently anticipating the Fourth Industrial Revolution (4IR) as well as the sustainability era, IT proficiency and generic skills among accounting graduates have become essential skills required by the industry (Heang et al., 2019). Consequently, it is fair to conclude that the minimal level of ESD implemented in the HEIs could potentially affect graduates’ employability due to the mismatch between employers’ expectations and the skills and knowledge required by graduates Mian et al. (2020) also supported this point of view, as one of the greatest obstacles faced by the majority of nations is related to the required skills of the workforce.

Nevertheless, previous research by Mastracchio (2017) indicates that formal accounting education in universities is ineffective and inadequate for preparing students for the workforce. The actual performance of accounting graduates in Malaysia is significantly below average, according to the study by Norman et al. (2018). This further demonstrates that accounting graduates lack the majority of skills and knowledge necessary for executing accounting tasks. In connection with this circumstance, a significant emphasis is placed on the vital role that accounting education plays in creating graduates with compatible and relevant abilities, in particular those related to information technology and sustainability.

Bridging Skill Expectation Gaps Between Employers And Higher Education Institutions

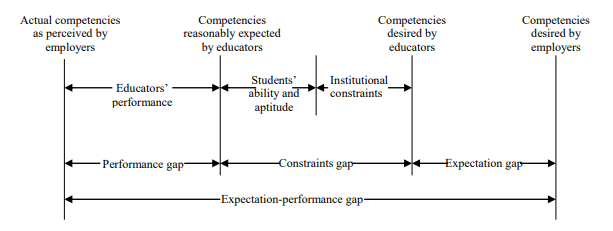

Prior researchers have cited and explored a number of challenges and factors for accounting education's failure to adequately equip accounting graduates with the expected competencies (Ghani et al., 2018; Heang et al., 2019). In light of this, Bui and Porter (2010) constructed a framework describing the gap between the competencies that accounting graduates are (1) expected to possess by employers and (2) perceived to possess by the profession. As shown in Figure 2, its components reflect the literature-identified contributing factors, and this framework has been extensively used in the literature with regards to this issue.

In the context of this paper, this study focuses on identifying the hard and soft skills – collectively referred to as 'skills' required to enhance the employability of accounting graduates. Succi and Canovi (2020) asserted that the notion of a "skills gap" refers to the mismatch between university graduates' abilities and the skills required by employers. The extent and severity of the skills gap depend on whether the appropriate skills are embedded in the syllabus and how they are introduced and assessed (Tan & Laswad, 2018; Tsiligiris & Bowyer, 2021). Table 3 provides a summary of the hard skills that may need to be taken into considerations when developing the accounting curriculum.

According to the findings of Archer and Davison (2008), employers prioritised soft skills such as communication skills and problem-solving skills over hard skills that entail technical knowledge. This could be due to the fact that soft skills are transferable (Freudenberg et al., 2011), unlike technical skills, which can become outdated (Kavanagh & Drennan, 2008). However, amidst the rapid and recent changes in the business environment, these findings may not be relevant, as can be argued.

In the recent studies by Bayerlein and Timpson (2017), they found that employees are expected to be equipped with a vast array of skills, both hard and soft skills, such as cognitive abilities, analytical thinking, and decision-making ability, to embrace and cater to the challenges. For example, Jørgensen et al. (2022) stated that the premise of materiality is becoming increasingly essential for measuring and reporting sustainability performance. There is broad consensus that materiality is critical in the sense that firms should identify, prioritise, and disclose information on material sustainability issues. Therefore, employers’ expectations nowadays are not only to focus on the technical skills relevant to the business but also on soft skills to communicate the financial and non-financial data to all stakeholders.

Cernușca (2020) also posited that accounting graduates need to possess a powerful set of soft skills in addition to the hard skills to maintain the relevancy of accounting professions in the era of digitalization and sustainability. Studies from Berry and Routon (2020) and Malan and Dyk (2021) discovered that the majority of employers are generally satisfied with the technical knowledge of accounting graduates, but greater emphasis must be put on the soft skills of the graduates as they are reportedly lacking in these areas. Table 4 summarises the soft skills that are needed by future accountants and have been discussed and cited by the majority of recent studies.

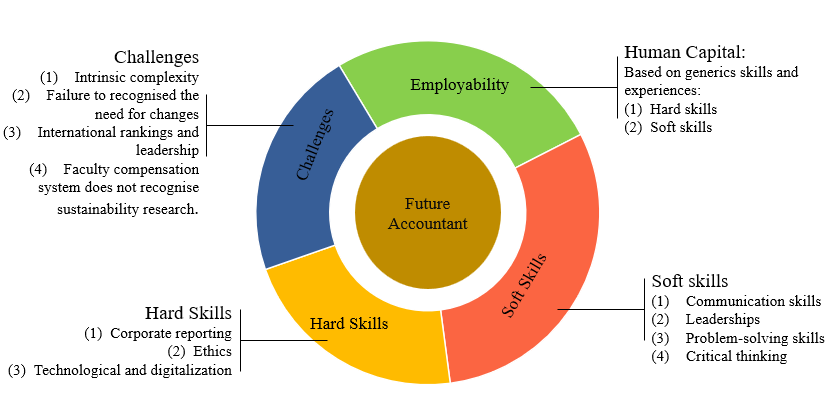

The globalisation of markets necessitated the development of a new set of skills for accountants in order for them to be successful and relevant across the changes in the business environment (Winterton & Turner, 2019). The majority of studies collectively agree that it is increasingly important to adapt to changing circumstances and acquire new skills, particularly in the field of information technology. However, recent studies by Kwarteng and Mensah (2022), Edeigba (2022) provided further evidence that HEIs are still failing to produce graduates equipped with appropriate capabilities to match opportunities. This assertion implied that graduates of higher education institutions lacked the required employment skills (Kwarteng & Mensah, 2022). Figure 3 presents the framework of the study.

Conclusion

This paper examines the issues surrounding the accounting curriculum in light of the era of sustainability. It outlines the concerns raised by employers regarding the need to maintain, revise, or enhance the accounting curriculum to ensure its continued relevance. This paper discusses the hard and emotional skills required of future accountants as well as the concept of human capital for future accountants. This paper posits that future accountants must be able to comprehend the potential in addition to the constraints of a rapidly changing business environment in the context of sustainability as well as the digitalization era, not just in the accounting industry. The evidence suggests that future accountants must possess a balance of skills, with soft skills gaining in importance. In the future, where cognitive skills will be highly valued and adjustments are made away from traditional accountancy work in the direction of more business advisory, it is believed that accountants will need soft skills on top of the hard skills.

Despite the challenges in sustaining the accounting education along with the rapid changes, there is a pressing need for the Malaysian accounting education system to be called for reform to minimise unsettling and unaddressed gaps in the competencies of the accounting graduates. The findings can be further enriched by addressing the gaps from the perspective of two critical stakeholders, which are employers and educators. This paper suggests that future studies should address the vast research gaps identified in the literature, allowing them to make clearer and more significant findings about perceived competencies.

References

Archer, W., & Davison, J. (2008). Graduate Employability: What do employers think and want? The Council for Industry and Higher Education.

Asonitou, S. (2022). Impediments and pressures to incorporate soft skills in Higher Education accounting studies. Accounting Education, 31(3), 243-272.

Association of Chartered Certified Accountants. (2016, June). Professional accountants – The future: Drivers of change and future skills. The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

Association of Chartered Certified Accountants. (2018). Drivers of change and future skills. Retrieved August 2, 2023 from: https://www.accaglobal.com/content/dam/members-beta/docs/ea-patf-drivers-of-change-and-future-skills.pdf

Azmi, I. A. G., Hashim, R. C., & Yusoff, Y. M. (2018). The Employability Skills of Malaysian University Students. International Journal of Modern Trends in Social Sciences, 1(3), 1–14. http://www.ijmtss.com/PDF/IJMTSS-2018-03-09-01.pdf

Bauer, M., Bormann, I., Kummer, B., Niedlich, S., & Rieckmann, M. (2018). Sustainability Governance at Universities: Using a Governance Equalizer as a Research Heuristic. Higher Education Policy, 31(4), 491-511.

Bayerlein, L., & Timpson, M. (2017). Do accredited undergraduate accounting programmes in Australia meet the needs and expectations of the accounting profession? Education + Training, 59(3), 305-322.

Berry, R., & Routon, W. (2020). Soft skill change perceptions of accounting majors: Current practitioner views versus their own reality. Journal of Accounting Education, 53, 100691.

Boeve-de Pauw, J., Gericke, N., Olsson, D., & Berglund, T. (2015). The Effectiveness of Education for Sustainable Development. Sustainability, 7(11), 15693-15717.

Bressler, L., & Pence, D. (2019). Skills Needed by New Accounting Graduates in a Rapidly Changing Technological Environment. Journal of Organizational Psychology, 19(2).

Bui, B., & Porter, B. (2010). The Expectation-Performance Gap in Accounting Education: An Exploratory Study. Accounting Education, 19(1-2), 23-50.

Carvalho, C., & Almeida, A. C. (2022). The Adequacy of Accounting Education in the Development of Transversal Skills Needed to Meet Market Demands. Sustainability, 14(10), 5755.

Cernușca, L. (2020). Soft and Hard Skills in Accounting Field-Empiric Results and Implication for the Accountancy Profession. Studia Universitatis „Vasile Goldis" Arad - Economics Series, 30(1), 33-56.

Clarke, M. (2018). Rethinking graduate employability: the role of capital, individual attributes and context. Studies in Higher Education, 43(11), 1923-1937.

Cornuel, E. (2007). Challenges facing business schools in the future. Journal of Management Development, 26(1), 87-92.

Dwaase, D. A., Awotwe, E., & Smith, E. O. (2020). Skills requirements of the professional accountant in a changing work environment. IOSR Journal of Humanities and Social Science, 25(12), 12-17.

Edeigba, J. (2022). Employers' expectations of accounting skills from vocational education providers: The expectation gap between employers and ITPs. The International Journal of Management Education, 20(3), 100674. https://doi.org/10.1016/j.ijme.2022.100674

Foley, H. (2020). Education for Sustainable Development Barriers. Journal of Sustainable Development, 14(1), 52.

Freudenberg, B., Brimble, M., Cameron, C., & English, D. M. (2011). Professionalising accounting education–the WIL experience. Journal of Cooperative Education and Internships, 45(1), 80–92

Fullan, M. (2001). Leading in a culture of change. San Francisco: Jossey-Bass.

Ghani, E. K., Rappa, R., & Gunardi, A. (2018). Employers' Perceived Accounting Graduates' Soft Skills. Academy of Accounting and Financial Studies Journal, 22(5), 1-11.

Giesenbauer, B., & Müller-Christ, G. (2020). University 4.0: Promoting the Transformation of Higher Education Institutions toward Sustainable Development. Sustainability, 12(8), 3371.

Greenberg, J., & Baron, R. A. (2000). Behaviour in organizations (7th ed.). Upper Saddle River, NJ: Prentice Hall.

Hanapi, Z., & Nordin, M. S. (2014). Unemployment among Malaysia Graduates: Graduates'Attributes, Lecturers' Competency and Quality of Education. Procedia - Social and Behavioral Sciences, 112, 1056-1063.

Heang, L. T., Ching, L. C., Mee, L. Y., & Huei, C. T. (2019). University Education and Employment Challenges: An Evaluation of Fresh Accounting Graduates in Malaysia. International Journal of Academic Research in Business and Social Sciences, 9(9).

Hillage, J., & Pollard, E. (1998). Employability: developing a framework for policy analysis. Labour Market Trends, 107, 83–84.

Hommel, U., Painter-Morland, M., & Wang, J. (2013). Gradualism prevails and perception outbids substance. In EFMD insights into sustainability and social responsibility (Vol. 119, No. 122, pp. 119-122). European Foundation for Management Development (EFMD) in association with GSE Research.

Hopkins, E. A., Read, D. C., & Goss, R. C. (2017). Promoting sustainability in the United States multifamily property management industry. Journal of Housing and the Built Environment, 32(2), 361-376.

Howcroft, D. (2017). Graduates' vocational skills for the management accountancy profession: exploring the accounting education expectation-performance gap. Accounting Education, 26(5-6), 459-481.

Institute of Chartered Accountants in England and Wales. (2023). Skills and traits the accountancy profession needs most at. https://www.icaew.com/insights/viewpoints-on-the-news/2023/feb-2023/skills-and-traits-the-accountancy-profession-needs-most

Jørgensen, S., Mjøs, A., & Pedersen, L. J. T. (2022). Sustainability reporting and approaches to materiality: tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal, 13(2), 341-361.

Kavanagh, M. H., & Drennan, L. (2008). What skills and attributes does an accounting graduate need? Evidence from student perceptions and employer expectations. Accounting & Finance, 48(2), 279-300. https://doi.org/10.1111/j.1467-629x.2007.00245.x

Kwarteng, J. T., & Mensah, E. K. (2022). Employability of accounting graduates: analysis of skills sets. Heliyon, 8(7), e09937.

Lai, A., & Stacchezzini, R. (2021). Organisational and professional challenges amid the evolution of sustainability reporting: a theoretical framework and an agenda for future research. Meditari Accountancy Research, 29(3), 405-429.

Lansdell, P., Marx, B., & Mohammadali-Haji, A. (2020). Professional skills development during a period of practical experience: Perceptions of accounting trainees. South African Journal of Accounting Research, 34(2), 115-139.

Lusher, A. L., Way, M., & Rock, S. (2012). What is the accounting profession’s role in accountability of economic, social, and environmental issues. International Journal of Business and Social Science, 3(15), 13-19.

Malan, M., & Dyk, V. V. (2021). Students' experience of pervasive skills acquired through sponsored projects in an undergraduate accounting degree. South African Journal of Accounting Research, 35(2), 130-150.

Mastracchio, N. J., Jr. (2017). A positive look at accounting education. The CPA Journal, 87(9), 32-35.

Mburayi, L., & Wall, T. (2018). Sustainability in the professional accounting and finance curriculum: an exploration. Higher Education, Skills and Work-Based Learning, 8(3), 291-311.

Mhlongo, F. (2020). Pervasive skills and accounting graduates' employment prospects: Are South African employers calling for pervasive skills when recruiting? Journal of Education(80).

Mian, S. H., Salah, B., Ameen, W., Moiduddin, K., & Alkhalefah, H. (2020). Adapting Universities for Sustainability Education in Industry 4.0: Channel of Challenges and Opportunities. Sustainability, 12(15), 6100.

Mohammad, W. M. W., & Wasiuzzaman, S. (2021). Environmental, Social and Governance (ESG) disclosure, competitive advantage and performance of firms in Malaysia. Cleaner Environmental Systems, 2, 100015. https://doi.org/10.1016/j.cesys.2021.100015

Ngoo, Y. T., Tiong, K. M., & Pok, W. F. (2015). Bridging the gap of perceived skills between employers and accounting graduates in Malaysia. American Journal of Economics, 5(2), 98-104.

Norman, S. N., Latiff, A. R. A., & Said, R. M. (2018). Employers‟ Perception on Skill Competencies and the Actual Performance of Bachelor of Accounting Graduates in Malaysia. International Academic Journal of Accounting and Financial Management, 05(02), 88-95.

Peeters, E., Nelissen, J., De Cuyper, N., Forrier, A., Verbruggen, M., & De Witte, H. (2019). Employability Capital: A Conceptual Framework Tested Through Expert Analysis. Journal of Career Development, 46(2), 79-93.

Rahman, M. R. C. A., Abdullah, T. A. T., Agus, A., & Rahmat, M. M. (2007). Universities – Workplace Competency Gaps: A Feedback from Malaysian Practising Accountants. Journal of Financial Reporting and Accounting, 5(1), 119–137.

Rasche, A., Gilbert, D. U., & Schedel, I. (2013). Cross-Disciplinary Ethics Education in MBA Programs: Rhetoric or Reality? Academy of Management Learning & Education, 12(1), 71-85.

Reza, M. I. H. (2016). Sustainability in Higher Education: Perspectives of Malaysian Higher Education System. SAGE Open, 6(3), 215824401666589.

Singh, P., Thambusamy, R., Ramly, A., Abdullah, I. H., & Mahmud, Z. (2013). Perception Differential between Employers and Instructors on the Importance of Employability Skills. Procedia - Social and Behavioral Sciences, 90, 616-625.

Smith, M., Duncan, M., & Cook, K. (2013). Graduate employability: Student perceptions of PBL and its effectiveness in facilitating their employability skills. Practice and Evidence of the Scholarship of Teaching and Learning in Higher Education, 8(3), 217-240.

Smith, V. (2010). Review article: Enhancing employability: Human, cultural, and social capital in an era of turbulent unpredictability. Human Relations, 63(2), 279-300.

Snelson-Powell, A., Grosvold, J., & Millington, A. (2016). Business School Legitimacy and the Challenge of Sustainability: A Fuzzy Set Analysis of Institutional Decoupling. Academy of Management Learning & Education, 15(4), 703-723.

Succi, C., & Canovi, M. (2020). Soft skills to enhance graduate employability: comparing students and employers' perceptions. Studies in Higher Education, 45(9), 1834-1847.

Tan, L. M., & Laswad, F. (2018). Professional skills required of accountants: what do job advertisements tell us? Accounting Education, 27(4), 403-432.

Tsiligiris, V., & Bowyer, D. (2021). Exploring the impact of 4IR on skills and personal qualities for future accountants: a proposed conceptual framework for university accounting education. Accounting Education, 30(6), 621-649. https://doi.org/10.1080/09639284.2021.1938616

Tsiligkiris, V., & Economics, W. (2020). The impact of technology on accounting technicians and bookkeepers.

Vanhercke, D., De Cuyper, N., Peeters, E., & De Witte, H. (2014). Defining perceived employability: a psychological approach. Personnel Review, 43(4), 592-605.

Vitolla, F., Raimo, N., & Rubino, M. (2019). Appreciations, criticisms, determinants, and effects of integrated reporting: A systematic literature review. Corporate Social Responsibility and Environmental Management, 26(2), 518-528.

Wall, T., Bellamy, L., Evans, V., & Hopkins, S. (2017). Revisiting impact in the context of workplace research: a review and possible directions. Journal of Work-Applied Management, 9(2), 95-109.

Williams, B., Horner, C., & Allen, S. (2019). Flipped v's traditional teaching perspectives in a first year accounting unit: an action research study. Accounting Education, 28(4), 333-352.

Winterton, J., & Turner, J. J. (2019). Preparing graduates for work readiness: an overview and agenda. Education + Training, 61(5), 536-551.

Yorke, M., & Knight, P. T. (2006). Embedding employability into the curriculum (Vol. 3). Higher Education Academy.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

15 November 2023

Article Doi

eBook ISBN

978-1-80296-130-0

Publisher

European Publisher

Volume

131

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1281

Subjects

Technology advancement, humanities, management, sustainability, business

Cite this article as:

Rosley, N. A., Muhammad, K., Ali, M. M., Ghani, E. K., & Ilias, A. (2023). Accounting Curriculum in the Sustainbility Era: Employability of Future Accountants. In J. Said, D. Daud, N. Erum, N. B. Zakaria, S. Zolkaflil, & N. Yahya (Eds.), Building a Sustainable Future: Fostering Synergy Between Technology, Business and Humanity, vol 131. European Proceedings of Social and Behavioural Sciences (pp. 1151-1163). European Publisher. https://doi.org/10.15405/epsbs.2023.11.93