Evaluation of the Internal Control Systems in the Malaysian Public Sector

Abstract

Internal control systems are critical for organizations to ensure that their objectives are achieved, providing a check and balance in their operations. The Committee of Sponsoring Committee Framework (COSO) is a widely used approach to evaluate the effectiveness of internal control systems. The general assumption is that the control environment is the most significant factor that affects the overall performance of internal control systems. The control environment refers to the importance of integrity and ethical values set by the organization's leaders, emphasizing the need for a strong and supportive environment to implement successful internal control systems. This paper presents a case study on how public sector organisations in Malaysia implement control measures for efficiency. This article discusses the importance of internal control systems in ensuring an organization's efficiency and operations. The COSO framework, which includes five components, helps to achieve efficacy in internal control systems. However, excessive control can lead to a bureaucratic and inflexible culture, impede innovation, and decrease employee motivation and productivity. Furthermore, too much emphasis on control can result in a narrow focus on compliance rather than performance, which can hinder organizational goals. Therefore, a balance in control measures is necessary in the public sector to achieve optimal output. This, in turn, leads to stakeholder confidence and assurance that the organization is operating effectively to achieve its objectives.

Keywords: Control Environment, COSO Framework, Internal control systems, Public Sector Governance

Introduction

The process of internal control involves the planned coordination of procedures that organizations implement to achieve their objectives and maintain their effectiveness, as defined by Grady in 1957 (Grady, 1957). Over time, the definition of internal control has evolved into a more comprehensive concept that impacts an organization's overall performance. One of the primary functions of internal control systems is the systems approach, which involves taking various parts of the organization and processing them through the COSO framework. This framework is based on five components: the control environment, risk assessment, control activities, information, and monitoring activities. Lord (2013) emphasizes the importance of improving the control environment related to the components of internal control systems to enhance the current systems approach (Lord, 2013).

According to Hassan et al. (2015), the use of internal control systems is closely related to an organization's objectives (Nadiah Hassan et al., 2015). An effective internal control system can improve the efficiency and effectiveness of the government, thereby enhancing the governance mechanisms within the organization itself. Good internal control systems can help organizations achieve their goals and reduce inefficiencies, resulting in greater dependability and compliance with rules and regulations. Compliance with internal control systems is assumed to make an organization compliant with rules and regulations, further adding to its dependability.

The public sector has developed several methods to ensure control, with the aim of generating specific types of output for their organizations (Aziz et al., 2015; Evans & Bellamy, 1995; Vašiček & Roje, 2019). A single public sector organization may have several departments, including procurement, accounting, human resources, administration, and operations. For instance, a basic representation of a public sector organizational chart in Malaysia, the most critical part of the section is the leader of the unit. Public sector organizations operate using their own systems, which differ from those used by private organizations to achieve their performance targets. Public sector organizations have different goals and objectives, and their actions are not motivated by profits (van der Kolk et al., 2019). While private organizations use management control systems to ensure that they achieve their targets, the public sector focuses on generating specific outputs to fulfill their objectives. When there are failures in the government, such as weak internal control systems, there are instances where corruption occurs due to opportunities to exploit the system (Nazirah Hassan, 2021; Said et al., 2018; Zahari et al., 2022).

Governments and public sector organizations have a responsibility to ensure that the taxpayers' money is being used effectively and efficiently to achieve their objectives (Vašiček & Roje, 2019). To accomplish this, they use various forms of control mechanisms such as management control, auditing, and effective governance. The new public management approach focuses on using incentives to increase the levels of production or output of public sector employees, which has progressed strongly over the years (Kapucu, 2006). The use of control systems, information systems, management control measures, governance, and accountability are all critical components of the public sector's operations. They help to ensure that public sector organizations are meeting their intended goals and objectives, while also providing taxpayers with the assurance that their money is being used wisely. For instance, effective management control measures help to optimize the use of public sector resources, while robust auditing processes ensure that public sector organizations are complying with legal and regulatory requirements.

In summary, the use of control mechanisms in the public sector is essential to achieve objectives, optimize the use of resources, and provide accountability to taxpayers. Therefore, public sector organizations must continue to evolve and adapt their control mechanisms to ensure that they remain relevant and effective in an ever-changing environment.

Problem Statement

Public sector organizations are responsible for providing essential services to the public, but they often face a challenging environment with limited resources (Plant, 2006). Public sector organizations, facing the challenge of providing services in a dynamic and resource-constrained environment, have been under increasing pressure to innovate and improve their performance. In this context, they have started to explore the innovation of new management methods and tools, including Management Control Systems (MCS), auditing, and effective governance. While the adoption of these control systems has been widely studied in the private and non-profit sectors, there is a lack of research on the use of these systems in the public sector (Lapuente & Van de Walle, 2020). Therefore, this study aims to investigate the adoption and impact of MCS in a sample of public organizations, in order to determine their effectiveness in improving public sector performance.

Malaysian Public Sector

In Malaysia, there is a federal constitutional monarchy system with a bicameral federal legislature and unicameral state legislatures (Ostwald, 2017). The Malaysian Public Sector pertains to the various governmental agencies and organizations that provide public services to the Malaysian people. It is responsible for enforcing government policies, laws, and regulations, and delivering public goods and services such as healthcare, education, infrastructure, and security. The Malaysian public sector comprises different government levels, including federal, state, and local governments, as well as government-linked corporations and statutory bodies (Department of Information Malaysia, 2017). It is a substantial employer in Malaysia and a vital contributor to the country's economic development and social progress. The public sector operates within a legal and regulatory framework designed to promote accountability, transparency, and good governance, and to ensure that the public sector serves the best interest of the Malaysian people.

The study aims to investigate the effectiveness and implementation of control systems, such as management control, auditing, and governance, in the Malaysian public sector. With the government's increasing emphasis on promoting transparency and good governance, the public sector in Malaysia is expected to operate in a more open and accountable manner. The study aims to investigate how the public sector in Malaysia is implementing accountability and transparency measures to ensure good governance, and how effective these measures are in achieving their intended outcomes. The study will also examine the challenges and barriers faced by the public sector in implementing these measures, and identify opportunities for improvement. Ultimately, the study seeks to provide insights and recommendations for policymakers and stakeholders in the public sector to enhance accountability, transparency, and good governance in the Malaysian public sector.

Public Sector Control Systems

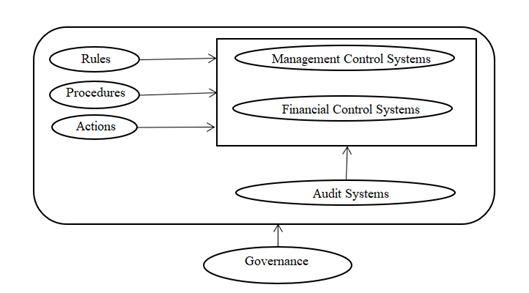

Public sector control systems are a collection of rules, procedures, and actions that are implemented to guarantee that public sector institutions function efficiently, effectively, and in accordance with legal and regulatory obligations (Heinrich, 2004). Control systems in the public sector include financial control systems, which ensure that financial transactions are recorded accurately and that the use of public funds is adequately supervised (van der Kolk et al., 2019; Vašiček & Roje, 2019). They also encompass management control systems, which monitor and control the performance of public sector organizations and ensure that they accomplish their goals (Bracci & Tallaki, 2021). Additionally, the public sector utilizes auditing as a control mechanism to evaluate the effectiveness of control systems and to assure stakeholders that public sector organizations are complying with legal and regulatory requirements. Effective governance is another control system that involves utilizing policies, procedures, and practices to guarantee that public sector organizations are administered transparently, responsibly, and ethically.

Each section of the public sector control system plays an important role in ensuring efficiency and performance. Governance is the foundation of the public sector's overall performance, as those in leadership positions are crucial in achieving organizational goals and objectives (Staicu et al., 2013). Therefore, leadership effectiveness is critical in any public sector structure. The audit process in government organizations serves as a check and balance to ensure that performance targets are met, and governments place heavy emphasis on this to ensure continuity of achievements and consistency of results. Figure 1 reflects how governance, the basic set of management control systems, and the actions taken by any public sector employees or organizations are interrelated.

Research Method

The research study utilized the case study method as it offers an opportunity to gain a comprehensive understanding of the different types of controls and their effects on organizational performance (Scapens, 1990). This approach is particularly beneficial for exploratory research, where theory can be used to explain observed phenomena and inform further development of theory (Creswell & Poth, 2018). Scholars have also acknowledged the advantages of case study research in management accounting practice, though the challenge lies in connecting numerous intricate experiences to core academic theory.

Interviews were an important part of the case study research due to the newness of the issues being discussed (Longhurst, 2003). The researcher initially had uncertainties regarding which questions were most important to ask. To develop the interview questions, a literature review of management control systems was conducted. The results of the review were used to create a series of semi-structured interviews, along with less structured discussions. This interview format provided flexibility for the interviewees to express their concerns and ideas more openly. Additionally, the approach allowed for the generation of supplementary questions for later interviews based on key issues identified by staff within the organization that were not covered in the initial literature review.

The data was based on interviews with representatives of similar departments in the Malaysian Public Sector, which provided various insights and information on key measurements of performance control. These questions included inquiries on how government control systems operate, what the standard achievements are, and what the drawbacks of such control systems are.

Case Study of a Malaysian Department Public Sector Control Systems

The control systems in Malaysian government departments are mainly based on performance-based appraisals. This study examines the usage of one such method of appraisals in ensuring government efficiency and governance. It is focused on the approach of Figure 1 in each of the systems used in the Malaysian government public sector.

Rules, Procedures, and Action

The conduct of public sector employees is largely predetermined by the Public Services Codes of Conduct that must be adhered to by each individual employed by the government. Those serving in government departments are mainly from the Federal Department Government Service, State Department Government Service, joint public service for the Federal Government and one or more state governments or joint public service for two or more state governments excluding the Federal Government. Those who are in service are mainly under the purview of the Malaysian Public Service Department.

Government employees are required to abide by the Public Service Codes of Conduct, which include the Code of Conduct for public service officers provided in Regulation 1993, General Orders, Service Circulars, Circular Letters, Regulations, and other rules issued by His Majesty the King from time to time (Kerajaan, 2006). This mostly covers the rules and procedures that must be adhered to by each government employee to ensure that there are sufficient controls in place.

The Malaysian government, like any other country, ensures heavy penalties for employees who do not follow such strict rules and regulations (Mankidy, 1994). Any criminal conduct or actions against the law or constitution would result in the termination of the government employee's service. Various methods of penalties are employed for government employees, such as cessation of pension schemes when they are involved in serious cases (Faruqi, 2011). The most stringent controls are when government employees are issued with a notice of discipline when they act against their organization. For example, an employee not coming to work for a period of six months would be issued a notice of discipline that can result in heavy penalties. These methods are needed to ensure that government employees do not take their responsibility lightly and act with the utmost care in their services.

Management Control Systems

The Malaysian government management control systems utilises performance measurement appraisals in their organisations. The method of the system is similar to private sector performance indicators. These indicators and appraisals are with the intention of the public sector employee giving their all in achieving such goals and objectives. These appraisals are managed through a system using the Human Resource Management Information Systems (HRMIS) with it managing the public sector employees (Wahab, 2011).

HRMIS is a human resource management system that integrates technology to simplify and combine the best practices of global human resource management (Masrek, 2009). This pioneering project was developed as part of the Electronic Government initiative. The main purpose of HRMIS is to automate human resource management operations, enable effective workforce planning and determine the size of the public service using human resource management information. It also aims to develop integrated and updated human resource information for effective human resource planning, provide an open and flexible human resource information system that is updated to meet management needs at various agency levels, contribute to a paperless environment, facilitate horizontal communication and integration, and align human resource processes through a single window.

The benefits of HRMIS in the public sector include improving user satisfaction by enabling users to check every transaction made through the HRMIS application (Shahibi et al., 2016). It eliminates the need to repeatedly enter basic personnel information and service profiles when dealing through the application, indirectly reduces manual and overlapping activities, and is user-friendly. The streamlined processes in this application can play a more strategic role and improve processing time, especially operational functions, through the use of digital technologies. The centralized and integrated database can also be viewed through this application, ensuring the standardization of implementation and centralized data collection for easier analysis and generation of statistical reports. Ultimately, this e-government application makes users and HRMIS management more effective and efficient

The HRMIS system is mostly based on individual evaluations, whereas organisation levels of evaluations of efficiency are based on a set of key performance indicators that are set by the related ministries of each department. The Malaysian government had initially started these performance indicators through a Performance Management and Delivery Unit (PEMANDU) that was under the purview of the Prime Ministers Department of Malaysia (Government Transformation Programme Annual Report, 2010). The process was that government ministries were required to identify strategic results areas that are of importance and strategic approach in these key performance indicators (Siddiquee, 2014). By utilizing performance measurement, particularly the key performance indicators system, the government was able to enhance their performance and demonstrate accountability to their citizens.

Audit Systems

The Malaysian government National Audit Department is largely responsible for auditing government organisations and departments. The Malaysian National Audit Department (NAD) is responsible for independently ensuring and accounting for the use of public funds and resources (Ahmad et al., 2009). Its primary function is to audit and assess the financial and operational performance of government agencies at the federal and state levels, as well as public sector organizations, such as local authorities and statutory bodies. The NAD's goal is to foster good governance, transparency, and accountability by delivering impartial and trustworthy audit reports to Parliament and the public, which can help identify areas for improvement and ensure efficient and effective use of public resources. Moreover, the NAD offers advisory and technical assistance to government agencies to improve their financial and operational management practices. In summary, the NAD plays a crucial role in promoting accountability and ensuring that public resources are utilized in the best interest of the Malaysian people.

COSO Framework evaluations

The COSO Framework can be a useful tool for the Malaysian Public Service Department (PSD) to assess and improve its internal control systems. The framework provides a comprehensive approach to evaluating the effectiveness of internal controls, which can help the PSD identify areas for improvement and strengthen its operations.

Specifically, the COSO Framework's five components, control environment, risk assessment, control activities, information and communication, and monitoring can be reflected in the PSD's internal control systems. For example:

Overall, the COSO Framework can be a useful tool for the PSD to strengthen its internal control systems, promote good governance and accountability, and ensure that public funds are used effectively and efficiently. The information obtained from government departments indicates that these control factors are implemented in the context of a COSO framework, as indicated in Table 1. Each of the components shows that there are methods of control applications used by the government for each of the active or inactive measures of ensuring performance and efficiency.

Discussion and Conclusion

Internal control systems are crucial to ensure an organization's efficiency and operations by providing a system of checks and balances (Länsiluoto et al., 2016). Such systems are also necessary in the public sector where government departments are responsible for executing policies and achieving objectives for the public's benefit. The COSO framework comprises five components, namely control environment, risk assessment, control activities, information communication, and monitoring activities, all of which contribute to the efficacy of internal control systems (INTOSAI, 2016). In addition to improving efficiency, internal control systems have been found to impact other aspects of an organization, such as internal audit effectiveness (Badara & Saidin, 2013). Meaning that when there is an effective control system in place, the organization is expected to perform as indicated in the performance measurements.

There are drawbacks of when there is too much control in place. It can lead to a bureaucratic and inflexible culture, where innovation and creativity may be stifled. Excessive control can also create a sense of mistrust and demotivate employees, leading to decreased job satisfaction and productivity (Oomsels et al., 2019). Additionally, too much emphasis on control may result in a narrow focus on compliance rather than performance, which can impede the achievement of organizational goals. Finally, an overly controlled environment can result in a lack of transparency and accountability, as decision-making is centralized and insulated from external scrutiny. Therefore, having a correct balance in control measures would ensure a more optimal output in the public service department. It can not be expected that every employee would outperform each other as there are always limited results for any organization.

In conclusion, internal control systems play a vital role in ensuring the efficiency and effectiveness of organizations, including those in the public sector. The COSO framework provides a comprehensive approach to evaluating and implementing these systems, encompassing various components that contribute to their success (Wardani, 2019). However, it is important to strike a balance in control measures, as excessive control can have drawbacks such as stifling innovation, demotivating employees, and hindering organizational performance (Hoai et al., 2022). A rigid and overly controlled environment may also compromise transparency and accountability. Therefore, organizations, especially those in the public service sector, should strive for an optimal balance in their control systems to foster a culture of accountability, innovation, and performance. It is important to recognize that not every employee can consistently outperform each other, as outcomes will always be limited within any organization.

Acknowledgments

The authors would like to thank the Universiti Poly-Tech Malaysia, grant code: 100-TNCPI/PRI 16/6/2 (056/2022), the Accounting Research Institute, and the Malaysian Ministry of Higher Education for providing the necessary financial assistance for this study. This study was made possible under the Internal Research Grant KUPTM 2022. We appreciate the reviews and comments made by academicians on earlier drafts of the paper. Special thanks to the participants that had been involved in the project. This study was made possible through the cooperation of various government departments in Malaysia. We would like to thank the Accounting Research Institute (ARI) again for supporting the research subject on control systems evaluations.

References

Ahmad, N., Othman, R., Othman, R., & Jusoff, K. (2009). The Effectiveness of Internal Audit in Malaysian Public Sector. Journal of Modern Accounting and Auditing, 5(9), 53.

Aziz, M. A. A., Rahman, H. A., Alam, M. M., & Said, J. (2015). Enhancement of the Accountability of Public Sectors through Integrity System, Internal Control System and Leadership Practices: A Review Study. Procedia Economics and Finance, 28, 163-169. DOI:

Badara, M. S., & Saidin, S. Z. (2013). Impact of the Effective Internal Control System on the Internal Audit Effectiveness at Local Government Level. Journal of Social and Development Sciences, 4(1), 16–23.

Bracci, E., & Tallaki, M. (2021). Resilience Capacities and Management Control systems in Public Sector Organisations. Journal of Accounting & Organizational Change, 17(3), 332–351. DOI:

Creswell, J. W., & Poth, C. N. (2018). Qualitative Inquiry and Research Design: Choosing among five approaches. https://uk.sagepub.com/en-gb/asi/qualitative-inquiry-and-research-design/book246896

Department of Information Malaysia. (2017). Malaysia 2017. http://www.penerangan.gov.my/dmdocuments/malaysia_2017/files/downloads/malaysia_2017.pdf

Evans, P., & Bellamy, S. (1995). Performance Evaluation in the Australian Public Sector: The role of management and cost accounting control systems. International Journal of Public Sector Management, 8(6), 30–38. DOI:

Faruqi, S. S. (2011, July). The Laws Relating to Staff Discipline at Malaysian Universities. In Kertas Kerja Seminar Perundangan Sumber Manusia, Universiti Sains Malaysia pada (Vol. 13).

Government Transformation Programme Annual Report. (2010). “Performance Management and Delivery Unit (PEMANDU). Retrieved from https://pemandu.org/wp-content/uploads/2023/05/2010-Government-Transformation-Programme-Annual-Report-English.pdf.

Grady, P. (1957). The Broader Concept of Internal Control. The Journal of Accountancy, (May), 41.

Hassan, N. (2021). Corruption within Law Enforcement in Southeast Asia: A Scoping Review. E-BANGI Journal, 18(8).

Hassan, N., Rahmat, M. M., & Muhammadun Mohamed, Z. (2015). Sistem Kawalan Dalaman, Sokongan Pengurusan dan Keberkesanan Audit Dalaman Sektor Awam Di Malaysia [Effectiveness of Internal Control System and Public Sector Internal Audit]. Asian Journal of Accounting and Governance, 6, 1-12. DOI:

Heinrich, C. J. (2004). Improving Public-sector Performance Management: One step forward, two steps back? Public Finance and Management, 4(3), 317–351.

Hoai, T. T., Hung, B. Q., & Nguyen, N. P. (2022). The impact of internal control systems on the intensity of innovation and organizational performance of public sector organizations in Vietnam: the moderating role of transformational leadership. Heliyon, 8(2), e08954. DOI:

INTOSAI. (2016). Guidelines for Internal Control Standards for the Public Sector. http://www.issai.org/media/13329/intosai_gov_9100_e.pdf

Kapucu, N. (2006). New Public Management: Theory, ideology, and practice. In Handbook of Globalization, Governance, and Public Administration (pp. 915–928). Routledge.

Kerajaan, W. (2006). Conduct and Discipline Act 1993 and its amendment in 2002. Retrieved on 21-10-2023 from https://docs.jpa.gov.my/docs/pu/pua111.pdf

Länsiluoto, A., Jokipii, A., & Eklund, T. (2016). Internal control effectiveness - a clustering approach. Managerial Auditing Journal, 31(1), 5-34. DOI:

Lapuente, V., & Van de Walle, S. (2020). The effects of new public management on the quality of public services. Governance, 33(3), 461-475. DOI:

Longhurst, R. (2003). Semi-structured Interviews and Focus Groups. Key Methods in Geography, 3(2), 143–156.

Lord, S. (2013). An overview of COSO’s 2013 Internal Control-Integrated Framework. McGladrey LLP. https://www.studeersnel.nl/nl/document/fontys/bestuurlijke-informatievoorziening/01-coso-2013-overview/44121024

Mankidy, J. (1994). Disciplinary Rules and Procedures: India, Malaysia, Philippines (Vol. 9). International Labour Organization.

Masrek, M. N. (2009). Reinventing Public Service Delivery: The Case of Public Information Systems Implementation in Malaysia (Informative paper). International Journal of Public Information Systems, 5(1).

Oomsels, P., Callens, M., Vanschoenwinkel, J., & Bouckaert, G. (2019). Functions and Dysfunctions of Interorganizational Trust and Distrust in the Public Sector. Administration & Society, 51(4), 516–544. DOI:

Ostwald, K. (2017). Federalism Without Decentralization: Power Consolidation in Malaysia. SSRN Electronic Journal. DOI:

Plant, T. (2006). Public sector strategic planning: An emergent approach: Public Sector Strategic Planning. Performance Improvement, 45(5), 5-6. DOI:

Said, J., Alam, M. M., Karim, Z. A., & Johari, R. J. (2018). Integrating Religiosity into Fraud Triangle Theory: Findings on Malaysian police officers. Journal of Criminological Research, Policy and Practice, 4(2), 111–123. DOI:

Scapens, R. W. (1990). Researching Management Accounting Practice: The role of case study methods. The British Accounting Review, 22(3), 259–281. DOI:

Shahibi, M. S., Saidin, A., & Izhar, T. A. T. (2016). Evaluating User Satisfaction on Human Resource Management Information System (HRMIS): A Case of Kuala Lumpur City Hall, Malaysia. International Journal of Academic Research in Business and Social Sciences, 6(10). DOI:

Siddiquee, N. A. (2014). Malaysia’s Government Transformation Programme: A preliminary assessment. Intellectual Discourse, 22(1).

Staicu, A. M., Tatomir, R. I., & Lincă, A. C. (2013). Determinants and Consequences of “Tone at the Top”. International Journal of Advances in Management and Economics, 2, 76–88.

van der Kolk, B., van Veen-Dirks, P. M. G., & ter Bogt, H. J. (2019). The Impact of Management Control on Employee Motivation and Performance in the Public Sector. European Accounting Review, 28(5), 901-928. DOI:

Vašiček, V., & Roje, G. (2019). Public Sector Accounting, Auditing and Control in South Eastern Europe. Springer.

Wahab, N. A. (2011). The Effectiveness of Human Resource Management Information System (HRMIS) Application in Managing Human Resource at the Perlis State Secretary Office. Universiti Utara Malaysia.

Wardani, M. K. (2019). The Effectiveness of Internal Control System and Role of Internal Audit on Local Government Performance. Journal Of International Conference Proceedings, 2(2), 112–122. DOI:

Zahari, A. I., Said, J., & Muhamad, N. (2022). Public Sector Fraud: The Malaysian perspective. Journal of Financial Crime, 29(1), 309–324. DOI:

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

15 November 2023

Article Doi

eBook ISBN

978-1-80296-130-0

Publisher

European Publisher

Volume

131

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1281

Subjects

Technology advancement, humanities, management, sustainability, business

Cite this article as:

Zahari, A. I., Said, J., Muhamad, N., & Ramly, S. M. (2023). Evaluation of the Internal Control Systems in the Malaysian Public Sector. In J. Said, D. Daud, N. Erum, N. B. Zakaria, S. Zolkaflil, & N. Yahya (Eds.), Building a Sustainable Future: Fostering Synergy Between Technology, Business and Humanity, vol 131. European Proceedings of Social and Behavioural Sciences (pp. 472-482). European Publisher. https://doi.org/10.15405/epsbs.2023.11.40