Digitalization As A Factor In Increasing The Profitability Of Agricultural Production

Abstract

The digital transformation of a major part of human activities is the basis for the development of modern society. Digitalization of the economy is important in general and for agriculture in the context of changes in production under the influence of digitalization, identification and inclusion of existing innovative potential. Existing research and practice on the use of digital technologies in agriculture show many positive effects, but agribusiness owners, employees, and government agencies are ultimately interested in only one effect: profit and profitability of production. The authors consider the mechanism of indirect influence of digital technologies and software application on profitability indicators in agriculture. The article provides the generalized data on the profitability of agriculture for certain branches of agriculture in Russia, which indicate a significant fluctuation in values. In such a case, the focus is on the variety of profitability indicators. Based on the peculiarities of the production process in agriculture, the author substantiates the need to use both digital agents and programs for managing agricultural production, which will have a significant impact on the volume of production, product quality (sales price) and cost of production. As a result of the increase in profit, the value of assets and capital is expected to increase. The effect of using digital technologies in agriculture will be an increase in the profitability of agriculture, and, consequently, its investment attractiveness. Thus, the article substantiates the positive impact of digitalization of agriculture on all indicators of profitability, but to varying degrees.

Keywords: Agricultural efficiency, digitalization of agriculture, profitability

Introduction

Profitability is one of the key positions in the overall system for evaluating the performance of an economic entity. It characterizes the economic stability and financial independence of the enterprise. The cost-efficient activity of the organization assumes constant profit generation, including satisfaction of employees needs, guarantees the fulfillment of obligations to the institutions of the financial and credit system, and is the main source of funding for the scientific, technical and social mechanism of organizations activities. Payments from profit to the budget form the main part of the state finances, and the economic development of the country as a whole, including living standards, depends on the rate of their growth. In this regard, it is necessary to comprehensively contribute to increasing the profitability of organizations. This requires organizing an effective profit management system at enterprises, providing for the adoption of targeted organizational and technical decisions. There is a powerful potential for economic growth in digital technologies, thanks to new opportunities for accuracy and automation of management. Agriculture is becoming more and more high-tech every day: information comes from digital agents located in the field, on the farm, from agricultural machinery, weather stations, satellites, drones. Incoming information is collected in one place from different participants of the production processes, forming an information field. Transition of the economy to a management system is based on the use of a large array of data generated by digital technologies. These data allow making more informed decisions based on operational data, the features of the processes and used equipment by a particular agricultural organization. The digital technologies used in this case will help to increase the profitability of agricultural production.

The study of aspects of agricultural modernization in the conditions of transition to the digital economy is reflected in the multiple reteach papers. However, the problems of agricultural modernization in the transition to the digital economy are not sufficiently developed, and in many aspects have not been studied.

Problem Statement

When analyzing the indicators of agricultural production profitability and, in general, economic efficiency, it is necessary to take into account all the existing features and unforeseen circumstances in this industry. In the agricultural sector, the profitability of production is always or in most cases lower than in other industries, because of production seasonality, high cost of labor and other material and monetary resources, and dependence on weather and biological conditions. Features of agricultural production also include the following:

- the main and irreplaceable means of production is land, which, with proper care of its fertile layer, will improve its quality characteristics;

- the production process mainly involves living organisms – plants, animals – developing on the basis of biological laws;

- the result of production depends on natural and climatic conditions;

- production is seasonal, which undoubtedly has a significant impact on labor management, equipment and production cycle;

- products that have already been produced are used in further production as its tools (feed, young cattle, seeds, fertilizers, etc.);

- the tools of production – tractors, combine harvesters, machines are moved, but the objects of labor remain in place;

- demand for agricultural products is not elastic;

- the products of this industry always remain one of the most important and are in high demand, and there are quite a large number of companies operating in this area, so there is high competition in this market.

These features have a significant impact on the fluctuation of agricultural profitability over the years (table 1).

In comparison with 2000, the profitability of agriculture, including by industry, has increased significantly, but from 2014 to 2018, the spread in indicator value for agriculture as a whole is 8.1 pp., in crop production, the spread was 18.2 pp, in livestock production - 8.5 pp. With such significant fluctuations in profitability, there is a problem of financial stability and the ability of agricultural organizations to carry out medium and long-term planning and financing using borrowed capital. Despite all the difficulties and dependence on natural and climatic conditions, it is necessary to strive to ensure the growth of profitability and reduce its volatility.

Agricultural production, with its specific features, dictates the widespread use of digital technologies (Chernikova, 2019). Thus, the participation of living organisms in the technological process, the connection of technical equipment with plants, animals and people can lead to random changes in certain parameters of the production process and uncertainty of control and management in agricultural facilities. In this case, the use of appropriate software (for example, for the preparation of feeding rations) will make it possible to level out this issue. The problem of distribution of parameters controlled in crop and livestock production over a large area can be solved by using digital agents. Thus, the use of digital technologies in agriculture will help to level out some of the agriculture features. In this regard, all suppliers of software for agriculture talk about reducing costs and increasing profitability when installing software. However, the mechanism of the impact of digitalization on the profitability of an agricultural organization remains unclear.

Research Questions

In most modern researches devoted to agricultural modernization, attention has been paid to technical and technological modernization, and the problem of transition to the use of digital technologies remains isolated and studied in fragments.

- The object of the research is the modernization of agriculture in the context of digital economy, which provides an improvement in the management quality of agricultural organizations.

- The subject of the research is the influence mechanism of agriculture digitalization on profitability indicators of agricultural organizations.

Purpose of the Study

The purpose of the research is to study the impact of agriculture digitalization on profitability indicators.

Research Methods

In this research, taking into account the multidimensional nature of the problem under study, general scientific methods of analysis, synthesis, induction, deduction, comparison, logical and systematic approaches were used.

Findings

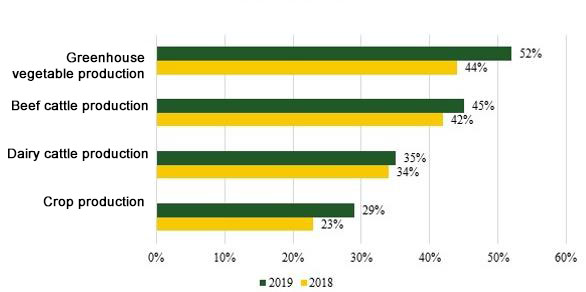

In table 1, we provided data from the Federal State Statistics Service on agricultural profitability. At the same time, it is necessary to cite the data of joint-stock company Russian Agricultural Bank, which, on the basis of its data, conducted an analysis of the profitability of the agro-industrial complex of Russia in the context of sub-sectors based on the results of 2019 (Russian Agricultural Bank, 2020). It is noted that in 2019, the profitability of the Russian agro-industrial complex as a whole was 20% (Figure 01), which exceeds the results of 2018 (according to JSC Russian Agricultural Bank - 19%). The difference in the values of profitability indicators is due to the difference in calculations.

It should be noted that there is no common terminology and methodology for calculating profitability. Thus, Minakov defines profitability as cost-effectiveness of an enterprise, where income is a part of the cost of gross output remaining after reimbursing of its production costs. Minakov, emphasizes that when describing the economic efficiency of agricultural production, a system of natural (crop yield and animal productivity) and cost indicators (gross and commodity products, gross and net income, profit and production profitability) is used, and natural indicators are the basis for calculating cost indicators. The authors Volodin and Samsonov note that the profitability indicator can be used for profit forecasting, correlating the profit with the amount of invested capital. According to Epstein, profitability is a category that shows how profitable a company is. Moreover, the scientist also notes that the higher the profitability indicators, the more successful the activity. According to Savitskaya, profitability is the degree of profitability, efficiency, and business earning capacity (Baetova, 2019).

Summarizing, we can define the category of profitability, as a relative indicator of production efficiency, which characterizes the level of cost return and the degree of resource use. Profitability indicators characterize the formation of income and the profit amount of the enterprise in the actual environment.

In general, all profitability indicators can be combined into 3 general groups:

- Profitability indicators based on the cost approach:

- profitability of certain types of products;

- profitability of operating activities;

- profitability of investment activities and investment projects;

- profitability of ordinary operations.

The profitability of costs for the enterprise as a whole or for certain types of products is calculated by the ratio of the profit from the sales to the costs:

(1)

profit from product sales, thousand rubles;

cost of products sold, thousand rubles

2) profitability indicators that characterize the profitability of sales:

- profitability of sales of certain products;

- total profitability of sales

Profitability of sales is characterized by the ratio of profit from product sales to sales volume:

(2)

– profit from product sales, thousand rubles;

РП - sales volume, thousand rubles.

3) profitability Indicators based on the resource approach:

- profitability of total assets;

- profitability of the operating capital involved in the main activity;

- profitability of equity, etc.

The level of these indicators is determined by the ratio of the profit of the reporting year to the average annual cost of fixed and working capital:

(3)

– profit for the reporting period, thousand rubles;

fixed capital of the organization, thousand rubles;

working capital of the organization, thousand rubles.

We will provide more detailed characteristics of certain types of profitability in table 2.

The listed indicators make it possible to assess the dynamics of economic performance, determine the trends and structure of these changes, take timely measures to eliminate existing problems and use the opportunities for their solution.

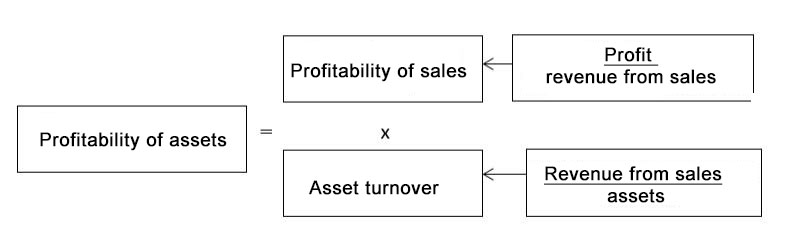

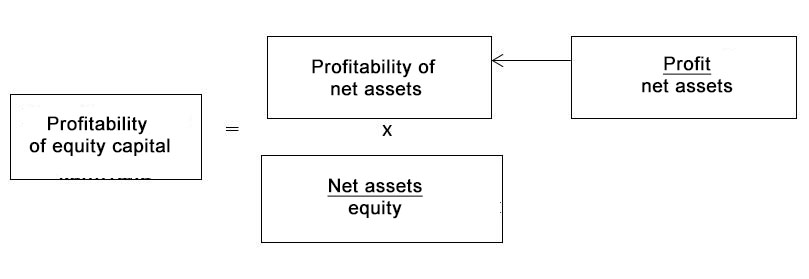

The most commonly used indicators are the profitability of assets of the enterprise (capital), profitability of net assets, sales of products and equity. The dependence of profitability indicators is shown in figures 2 and 3 (Timofeeva et al., 2014).

Analysis of profitability indicators given above is based on calculating the profitability and assessing the impact of the sales profitability, efficient use of working and fixed capital to changes in the profitability of the enterprise.

The negative dynamics of the assets profitability indicator shows a decrease in demand for the products of the organization and excessive accumulation of assets (Shumakova et al., 2016). The decrease in the non-working capital efficiency indicator for the analyzed period shows insufficient utilization of existing fixed assets if the company has not purchased new expensive equipment. If the indicator is too high, it means that the equipment is fully loaded, there are no reserves, and there is a very high probability of physical depreciation and obsolescence of outdated equipment. The profitability of equity capital ratio makes it possible to understand how effectively the capital invested by the founders is used and to compare this indicator with the anticipated profit from investing this capital in another type of activity. The working capital profitability indicator describes the efficiency of using the working capital of an enterprise, the speed of sales, and the effectiveness of relationships with consumers. The decrease in this indicator indicates a decrease in the efficiency of working capital use, an increase in the probability of doubtful and bad accounts receivable, as well as an increase in the degree of commercial risk. The profitability coefficient of the main activity characterizes the amount of profit received from each ruble of products sold. The growth of this indicator positively characterizes the activities of the company. The profitability coefficient of the main activity is defined as the ratio of profit from sales to production costs and largely duplicates the profitability coefficient of the sales. A decrease in the coefficient indicates an increase in the cost of producing products or a decrease in prices. Also, an efficiency indicator of the main activity of the enterprise is the profitability of operating capital, which is involved in the operating activities of the organization. The profitability of permanent capital reflects whether the use of equity and debt capital is effective over the long term.

The need for continuous monitoring of profitability indicators is justified by the performed functions:

1) accounting function involves recording the results of the organization activities for a certain period;

2) the valuation function involves comparing profit with costs, income, assets, capital;

3) the incentive function helps to prevent the deterioration of financial stability.

Regardless of the indicator type, profitability depends on the amount of profit (per unit of production, net profit, profit from sales). Some indicators include production cost and sales revenue, but these values also determine the amount of profit. In other indicators of profitability, the calculation includes the value of assets and capital that should increase with increasing profits, namely retained earnings. Thus, we will consider how the introduction of digital technologies in agricultural organizations affects the volume of profits.

The profit of the agricultural organization is affected by:

- production volume (yield, gross harvest, milk production, meat production, etc.);

- quality of manufactured products;

- price;

- production costs;

- organization of production distribution, etc.

Each of these factors is influenced by the digitalization of agriculture. Within the framework of the state strategy for agricultural modernization in the context of the digital economy, several areas are highlighted (Digitalization of agricultural production in Russia for the period 2018-2025). We will consider two of them: a "smart" field and a "smart" farm. The "smart" field is designed to ensure stable growth of crop production. The project involves the introduction of digital technologies for collecting, processing and using an array of data on the state of fields, namely soil, plants (root and vegetative systems) and the environment (Parkhomenko et al., 2019). A "smart" farm should stimulate the competitiveness of the livestock complex through the creation and implementation of technologies that ensure an increase in the milk productivity of animals up to 13.000 liters per year; herd health, reduced unplanned animal disposals and therefore lower antibiotic costs; creation and implementation of technologies for autonomous production (without an operator). Based on the data transmitted by digital agents, a decision is made on the timing and volume of production operations, i.e. not "by eye", not on the basis of standard deadlines, but based on the peculiarities of the development of living organisms, the peculiarities of natural conditions in this period and at this enterprise. Timely production operations (fertilization, harrowing in crop production; insemination, balanced feeding rations, early detection of mastitis in animal husbandry) ensure an increase in production volumes without the use of extensive factors and an improvement in the quality of products (Bikbulatova et al., 2019). The effect increases with the use of agricultural production management programs, while there is software of both domestic and foreign development on the market, and the cost of the basic package is 300-450 thousand rubles (Zaitseva et al., 2020).

Concerning such a factor as price, it should be noted that it depends on the market conditions, which cannot be influenced by each individual enterprise, however, by achieving a higher quality of products (varietal purity, the value of gluten, weediness in crop production, fat content in animal husbandry), an enterprise can expect a higher selling price.

The acquisition and implementation of digital technologies in production should certainly contribute to the growth of production costs by amortizing the cost of equipment. However, reducing losses (fuel, fertilizers, seeds, feed, livestock deaths) while improving the accuracy of operations will help reduce costs.

In terms of sales organization and financial relations with contractors, many programs for agricultural production management contain logistics units and control of debtors account, which is designed to improve the quality of financial management of the enterprise. The analytical unit of the software provides an opportunity to compare the plan-fact and identify the reasons for the deviation of the planned indicators from the actual ones without significant labor costs.

Standardization and the creation of a data network facilitate the two-way exchange of information and facilitate interaction between representatives of the same and different levels of production, market participants (including investors and consumers), and government agencies (Manzhosova, 2019). The use of digital technologies in agricultural production and the accumulation of an array of data in a single software shell that can quickly generate various reports using filters makes it possible to ensure the necessary transparency of this industry and translate into a digital field the format of relations between agricultural organizations with government agencies (in the context of state support programs) and potential investors (banks and other financial structures). The latter will allow agriculture to count on a reduction in interest rates on loans and acceleration of lending processes, which will help reduce costs, losses in the quality and quantity of products produced (respectively, if other factors remain unchanged, we will see an increase in profitability), as well as the development of investment processes.

Conclusion

The digital transformation of the economy and agriculture, in particular, should not be seen as an end in itself, but as means used to innovatively optimize the existing potential. In addition to the above, digitalization is currently an imperative for the development of society. The introduction of new methods of work based on digital technologies into agricultural production has various effects: reducing the burden on physical labor, improving working conditions for employees, increasing the accuracy and timeliness of production operations, generating checklists with an accurate and understandable task for employees and issuing them remotely. The effect of using digital technologies in agriculture will be an increase in the profitability of agriculture, and, consequently, its investment attractiveness. Increasing various indicators of profitability in digital agriculture will be provided by intensive growth in production volumes and improving the quality of products due to the timeliness and adequacy of decisions made by operational information from digital agents of this agricultural organization, the accuracy of production operations. The impact of processes digitalization on the cost of production is ambiguous: on the one hand, there is a reduction in losses (hence costs), on the other hand, the cost of equipment using digital technologies and software will increase the cost of production. Thus, digitalization of agriculture will have a positive impact on all indicators of profitability, but to varying degrees.

References

Agriculture in Russia. 2019: Statistical Abstract/ Federal State Statistics Service Moscow

Baetova, D. R. (2019). Improving the financial stability of agricultural enterprises in the Omsk region Topical issues of the modern economy, 6(1), 579-584.

Bikbulatova, G., Kupreyeva, E., Pronina, L., & Shayakhmetov, M. (2019). Using Remote Sensing Methods in Precision Agriculture Proceedings of the International Scientific Conference The Fifth Technological Order: Prospects for the Development and Modernization of the Russian Agro-Industrial Sector (TFTS 2019) (pp. 55-59). Atlantis Press SARL.

Chernikova, S. A. (2019). Directions of digital economy development in the agro-industrial complex Moscow Economic Journal, 7280(287).

Digitalization of agricultural production in Russia for the period 2018-2025. https://agrardialog.ru/files/prints/apd_studie_2018_russisch_fertig_formatiert.pdf

Manzhosova, I. B. (2019). Formation of a strategy for modernization of agriculture in terms of digital economy. Orel, Publishing house of Federal State Budgetary Educational Institution of Higher Education Orel State Agrarian University

Parkhomenko, N., Garagul, A., & Shayakhmetov, M. (2019). The Use of Remote Sensing Methods to Study the Ecological State of Agricultural Soils Proceedings of the International Scientific Conference The Fifth Technological Order: Prospects for the Development and Modernization of the Russian Agro-Industrial Sector (TFTS 2019) (pp. 269-273). Atlantis Press SARL

Russian Agricultural Bank (2020). Russian Agricultural Bank spoke about the profitability of the domestic agro-industrial complex. https://www.om1.ru/bank/news/releases/185830-rosselkhozbank_rasskazal_o_rentabelnosti_otechestvennogo_apk/

Shumakova, O. V., Blinov, O. A., Khrabrykh, S. L., Mozzherina, T. G., & Kryukova, O. N. (2016). Disclosure of assets of the agricultural enterprises in the financial reporting under international financial reporting standards. International Journal of Economics and Financial Issues, 2, 172-178.

Timofeeva, K. A., & Pavlova, Yu. A. (2014). Ways to increase profitability Azimuth of scientific research: Economics and Management 2014 No. 4. 98-102.

Zaitseva, O. P., Baetova, D. R., & Goncharenko, L. N. (2020). Application of Digital Management Technologies in the Agricultural Insurance Sector Proceedings of the International Conference on Policies and Economics Measures for Agricultural Development (AgroDevEco 2020) (pp. 107-113). Atlantis Press SARL.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 July 2021

Article Doi

eBook ISBN

978-1-80296-112-6

Publisher

European Publisher

Volume

113

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-944

Subjects

Land economy, land planning, rural development, resource management, real estates, agricultural policies

Cite this article as:

Zaytseva, O. P., Baetova, D. R., Goncharenko, L. N., & Kuznetsova, V. V. (2021). Digitalization As A Factor In Increasing The Profitability Of Agricultural Production. In D. S. Nardin, O. V. Stepanova, & V. V. Kuznetsova (Eds.), Land Economy and Rural Studies Essentials, vol 113. European Proceedings of Social and Behavioural Sciences (pp. 285-294). European Publisher. https://doi.org/10.15405/epsbs.2021.07.35