Improvement Of Cost Accounting And Product Costing In Dairy Farming

Abstract

The development and improvement of methods for cost accounting and product costing in dairy farming is one of the main factors in increasing economic efficiency of agricultural enterprises. It is high-quality and careful accounting of costs that improves the profitability of enterprises. The most advantageous methodology employed for calculating costs of milk, offspring, live weight of livestock will promote the efficiency of dairy production. The paper deals with organizational and methodological issues of cost accounting and product costing. It focuses on agricultural enterprises of the Omsk region. The paper describes various methods for accounting costs in dairy farming and calculating the prime cost of milk and offspring. Based on the methods available, the paper proposes a methodology for calculating the cost of dairy products in the context of responsibility centers (farms). It is assumed that total costs will be apportioned among farms subject to a design ratio. The ratio is calculated for each center of financial responsibility (farm) based on a scoring system against milk production and herd reproduction. The authors propose a revised cost sheet for calculating the prime cost of dairy products. The cost sheet must be drawn up in the context of each center of financial responsibility, since the method proposed calculates prime costs for each CFR. The cost sheet should involve all costs incurred by CFRs, given the specific features of the dairy industry. Additional economic and production indicators are introduced into the revised cost sheet.

Keywords: Costs, center responsibility, dairy farmin

Introduction

The dairy farming industry in the Omsk region is one of the priorities in ensuring food security of the region. Therefore, high economic efficiency of the industry will testify to the whole dairy subcomplex within the agro-industrial complex of the Omsk region. In 2019, milk production decreased by 1.1% in the Omsk region, compared to the level of 2018, and amounted to 609.3 thousand tons. Of these, 336.6 thousand tons accounted for agricultural organizations, the rest for peasant farms (including entrepreneurs) and private subsidiary farming. Statistics for January-June 2020 shows that milk production increased by 1.5% from 303.2 thousand tons in 2019 to 307.6 thousand tons in 2020 across all categories of farms. In 2019, the average milk yield per cow was 5,156 kg. The highest milk yield per cow is recorded in the following districts of the Omsk region: Bolsherechensky (7,393 kg), Omsk (6,954 kg), Cherlaksky (6,928 kg), Krutinsky (6,751 kg). The lowest milk yield per cow (less than 4,000 kg) is in Nazyvaevsky, Lyubinsky, Okoneshnekovsky, Kalachinsky, and Gorkovsky districts (Shumakova et al., 2019; Territorial body of the Federal State Statistics Service for the Omsk Region, 2019, 2020).

One of the main tasks of agricultural enterprises in the dairy farming industry is to reduce costs in order to boost economic efficiency. Therefore, cost managerial accounting in dairy farming is one of the most important components in the management system of the entire industry. Cost accounting in dairy farming is necessary to provide immediate data both for individual centers of responsibility (structural divisions) and for the entire agricultural enterprise (Kosenchuk et al., 2019).

Problem Statement

The current methodology for calculating the cost of production in dairy cattle breeding is reduced to a ratio of 90:10, that is, 90% of the costs go with milk, and 10% with offspring, which is justified in terms of accounting for feed costs (in accordance with metabolic energy). As for other costs (some direct, indirect), this methodology (90:10) is not entirely effective. The current methodology for the costs of dairy cattle breeding does not involve physiological characteristics of cows at different age periods, the conditions of milking and keeping cows, and other specific costs related to dairy farming alone. Therefore, it is crucial to come up with a truly effective, advantageous methodology for cost accounting and product costing, which could go in line with specific features of the dairy cattle breeding industry, thereby calculating the real prime cost of milk, offspring, and live weight gain. The issues of cost accounting and product costing in agricultural organizations were addressed by such scientists as M.Z. Pizengolts, G.M. Lisovich, G.V. Savitskaya, N.G. Belov, L.I. Horuzhy and others. A.P. Kalashnikova, V.A. Sirotki, I.N. Nikitina were engaged in the issues of fostering the economic efficiency of milk production and processing.

Research Questions

The subject of research is organizational and methodological issues of cost managerial accounting in agricultural enterprises engaged in dairy cattle breeding.

Enterprises engaged in dairy production (milk, offspring), calculate the prime cost as follows: when total costs are estimated, the cost of by-products is taken away (the cost of by-products is calculated based on the actual production costs). As a result, the total cost is distributed between milk and offspring in a 90:10 ratio, that is, 90% of the costs account for milk, and 10% for offspring. To define one hundredweight of milk, the total cost of milk must be divided by the total milk yield. To calculate the cost of one animal of offspring, it is necessary to divide the total costs of offspring by the total number of offspring (Ministry of Agriculture of the Russian Federation, 2003a). Based on the current methodology, Tables 01-02 present the calculation of the prime cost of milk, offspring for 2019 at Kirov agricultural enterprise (AE) of Kalachinsky district of Omsk region.

Having calculated the actual cost of livestock products, it is seen that one hundredweight of milk costs 277.21 rubles, which is below the estimated indicator for the enterprise. The actual cost of one unit of offspring is lower than the estimated for the enterprise. Therefore, it is necessary to draw up corrective transactions, where the surplus of the estimated cost over the actual will be reflected by the “red-ink entry” method (Table 02).

Many authors distinguish costs depending on the technological conversion. In dairy farming, there is a dry period and a lactation period. For example, Goncharenko (2013) proposes a methodology for the estimation of costs by cost centers including a calving workshop, a post-calving workshop, a milk production workshop, and an interlactation workshop. The costs are distributed by product type using design energy-product ratios, which is represented by the sum of milk yield energy, live weight gain and energy spent on fetal development (Goncharenko, 2013).

Kudryashova (2017) compares the current methodology for calculating the cost of milk, offspring with methods that rely on conversion factors of live weight into milk, sales prices, quality characteristics of milk. The team of authors (Gonova, et al, 2019), for calculating product costs in dairy cattle breeding, considers such qualitative characteristics as the average percentage and the base percentage of milk fat, resulting in the cost of milk lower than with the current method. Some authors (Govdya & Degaltseva, 2014) calculate the cost based on cost distribution coefficients in a planned economy (milk – 1; offspring – 1.5). This method fails to reflect the actual costs of the enterprise. Bystrova (2020) provides several methods for calculating the cost of joint production (milk, offspring). Particular attention should be paid to the separation of dairy and pedigree cattle breeding, including the cost of maintenance, accounting entities and cost calculation (Bystrova, 2020).

Purpose of the Study

The paper aims to postulate and develop practical recommendations for improving the methodology for recording costs and calculating the prime cost of dairy products in order to effectively manage and control the industry.

Research Methods

The study was based on the following methods: analysis of statistical data, analysis of accounting registers for cost accounting and calculation, comparison of cost accounting and cost calculation, calculation of dairy products, double entry (entries to reflect costs and yield of livestock products) , cost estimate (determination of actual and planned costs).

Findings

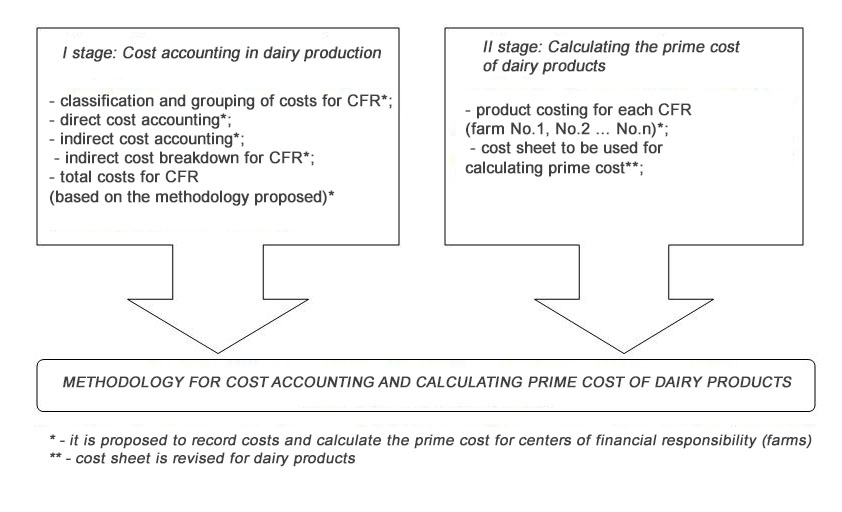

Figure 01 presents a refined methodology for cost accounting and calculating the prime cost of dairy products, in the context of each center of financial responsibility (farm). According to the methodology, the pivotal is the center of responsibility that embraces all production and economic processes: accumulation, classification and grouping of costs, breakdown of costs, calculation of prime cost, use of reporting forms and accounting documents (cost sheet for calculating prime cost) and other processes (Gapon & Golova, 2019; Shumakova et al., 2014).

Table 03 presents a point-based estimate of cost breakdown in terms of productivity and herd reproduction in dairy farming. These indicators should be calculated by the centers of financial responsibility, that is, for each farm (Ruchkina & Kryukova, 2017; Shumakova et al., 2016).

Depending on the number of points scored by CFRs, the distribution coefficient of the total costs for each CFR (farm) is defined (Table 04). As a result, the total cost is subject to distribution among the CFRs, based on the design coefficient. Product costing in the context of CFRs will allow the heads of enterprises to make more effective managerial decisions improving economic profitability of dairy products.

A revised cost sheet (Table 05) is proposed to calculate the prime cost of dairy products for CFRs. The Order of the Ministry of Agriculture of the Russian Federation of 06.06.2003 No. 792 provides a template of cost sheet for crop production, which contains the minimum set of indicators for calculating the prime cost (Ministry of Agriculture of the Russian Federation, 2003b). Therefore, the authors have refined and supplemented the template of cost sheet for calculating the actual cost of dairy products, namely: for the products of the core dairy herd and products for growing and feeding dairy cattle (milk, offspring, live weight, and live weight gain). This template is designed to account costs and calculate the actual prime cost for CFRs (farms, corrals), which reflects the cost attributed to the production of a product in a more realistic and high-quality manner. The proposed template is also suitable in a way it addresses specific features of the dairy farming industry, since it is necessary to reflect the costs for all available items for each CFR.

The cost sheet also includes such additional economic indicators as: the average milk yield per 1 forage cow, the average live weight of a calf at birth, the number of offspring animals per 100 cows and heifers, costs per cwt of milk, costs per 1 offspring animal, costs of 1 cwt of live weight gain. It also includes some additional indices (coefficients), which make it possible to distribute total costs among CFRs. The indicators calculate the cost of milk production and herd reproduction.

Conclusion

The study resulted in some practical recommendations in the field of cost accounting and calculating the prime cost of dairy cattle products. The methodology for cost accounting and calculating the prime cost of dairy cattle products has been updated, which calculates the prime cost based on the indicators of milk productivity and herd reproduction in the context of each center of financial responsibility. The template of cost sheet is recommended for use in dairy cattle breeding for calculating the cost of milk production, offspring, live weight gain, given the specific costs of the industry and including additional production and economic indicators. Thus, the proposed method of cost accounting and calculating the cost of dairy products, with cost breakdown for CFRs depending on the productivity and reproduction of each farm, will allow more accurate calculation of the cost of production, which ultimately will ensure the efficiency of the entire agricultural enterprise.

References

Bystrova, N. Y. (2020). Development of methods for the distribution of joint costs in breeding production. https://elibrary.ru/item.asp?id=42535277

Gapon, M. N., & Golova, E. E. (2019). Organization of cost accounting in animal husbandry (through the example of agricultural enterprise). Siberian Financial School, 5, 187.

Goncharenko, G. V. (2013). Improving managerial accounting in dairy farming. Retrieved from: http://economy-lib.com/

Gonova, O. V., Lukina, V. A., & Malygin, A. A. (2019). Methodological approaches to the search for reserves for reducing the cost in the branches of agricultural production. Socio-economic and human sciences, 3, 118.

Govdya, V. V., & Degaltseva, Z. V. (2014). Cost management and product costing in dairy farming. Agricultural Bulletin of Stavropol Region, 2(14), 216

Kosenchuk, O., Shumakova, O., Zinich, A., Shelkovnikov, S., & Poltarykhin, A. (2019). The development of agriculture in agricultural areas of Siberia: multifunctional character, environmental aspects. Journal of Environmental Management and Tourism, 5(37), 991-1001.

Kudryashova, Y. N. (2017). Accounting and analytical support for cost accounting and calculating the cost of dairy products. https://elibrary.ru/item.asp?id=29986577

Ministry of Agriculture of the Russian Federation. (2003a). Methodical recommendations on accounting of production costs and product costing (activities, services) in agricultural enterprises No. 792. http://www.consultant.ru/document/cons_doc_LAW_59524/

Ministry of Agriculture of the Russian Federation. (2003b). Methodological Recommendations for Cost and Yield Accounting in Dairy and Beef Cattle Breeding. http://www.consultant.ru/document/cons_doc_LAW_93052/

Ruchkina, V. A., & Kryukova, O. N. (2017). Improvement of accounting and calculation of the cost of dairy products. Bulletin of Altai State Agrarian University, 6, 176.

Shumakova, O. V., Blinov, O. A., Khrabrykh, S. L., Mozzherina, T. G., & Kryukova, O. N. (2016) Disclosure of assets of the agricultural enterprises in the financial reporting under international financial reporting standards. International Journal of Economics and Financial Issues, 2, 172-178.

Shumakova, O. V., Karamnova, N. V., Emelianenko, K. V., & Melnikova, S. S. (2019). Priorities for improving the organizational and economic mechanism of innovative development of dairy cattle breeding (through the example of the Omsk region). Bulletin of the Altai Academy of Economics and Law, 12, 196.

Shumakova, О. V., Kovalenko, E. V., & Gapon, М. N. (2014). Developing a methodological approach to cost managerial accounting. Aktualʹni problemy ekonomiky, 9(159), 455.

Territorial body of the Federal State Statistics Service for the Omsk Region. (2019). On livestock production in January – December 2019. https://omsk.gks.ru/news_stat/document/74036?print=1

Territorial body of the Federal State Statistics Service for the Omsk Region. (2020). Livestock production in January – June 2020. https://omsk.gks.ru/storage/mediabank/o6vZh3zH/shg_06-2020.htm

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 July 2021

Article Doi

eBook ISBN

978-1-80296-112-6

Publisher

European Publisher

Volume

113

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-944

Subjects

Land economy, land planning, rural development, resource management, real estates, agricultural policies

Cite this article as:

Gapon, M. N., Golova, E. E., & Baranova, I. V. (2021). Improvement Of Cost Accounting And Product Costing In Dairy Farming. In D. S. Nardin, O. V. Stepanova, & V. V. Kuznetsova (Eds.), Land Economy and Rural Studies Essentials, vol 113. European Proceedings of Social and Behavioural Sciences (pp. 79-87). European Publisher. https://doi.org/10.15405/epsbs.2021.07.11