Organizational And Economic Cost Management Mechanism And Cost Effectiveness Indicators

Abstract

The approaches to the definitions of an organizational and economic cost management mechanism are formulated. The article presents specific internal and external characteristics of machine-building enterprises, the main threat and opportunity for their development. Special attention is focused on the time factor that helps to form an organizational and economic mechanism taking into account operational, tactical and strategic approaches for implementing at the machine-building enterprises. As a result of assumptions the organizational and economic cost management mechanism is clearly presented in the form of a scheme. Based on the time factor and the selected approaches, the importance of separating of capital expenditures and current costs is emphasized. It is also revealed the necessity for separate study of costs that are formed on the basis of the cost structure according to bookkeeping rules, as well as on the basis of their construction within the framework of cash flows. This paper defines a system of indicators for evaluating economic efficiency within the framework of the selected tactical and strategic approaches of the organizational and economic cost management mechanism. At the same time, the cost indicators specified in this system were presented in the form of coefficients for clarity and grouped into a table. The annual cost formula is given in the framework of the specified cash flow calculation algorithm.

Keywords: Capital expenditurescost management mechanismcurrent expendituresoperational componentstrategic component

Introduction

The development of the economy and modern conditions of market changes promote the difficulties in the industry development especially for high-tech and science-intensive enterprise. The issues of optimal use of resources and production costs in enterprises become more relevant. For many centuries economists and researchers have developed the cost management methods to minimize production costs. However, not enough attention is paid to the building a separate organizational and economic mechanism of cost management within machine-building enterprises with their characteristics and their already formed specific structures. Not enough attention is payed to the specific development conditions of market in the country, where these machine-building enterprises are located. The existing methods of cost analyzing and cost management need to be adapted to the modern market conditions and industry development and new methods, principles of cost management need to be developed.

The organizational and economic cost management mechanism is based on objective laws of public development and in the same time it is an active and self-organizational system with flexible internal and external connections. According to different researchers of the economists, cost management practices have positive impact on the competitiveness in strategic priorities (Amir et al., 2016). The organizational and economic cost management mechanism always develops according to public changes and economic relationships. Organizational and economic mechanism of cost management is a complex of two different and interrelated organizational and economic components.

In the organizational and economic cost management mechanism, as a rule, the following control and controlled systems are distinguished. In the control system the following blocks are highlighted: functions (planning and forecasting, cost management organization, regulation and coordination, accounting and analysis, control); cost reduction tools and cost management principles (Naugolnova, 2015). It can be admitted that there is a potential for improving resource efficiency and energy efficiency in manufacturing enterprises due to the use of innovative methods. However, there are many negative aspects that prevent the broad implementation of promising measures. To reduce costs, it is necessary to study the methodology for optimizing the energy efficiency of complex technical systems (Thiele et al., 2019).

Problem Statement

It was revealed that most of existing approaches of the cost management mechanism is elaborated for all functioning enterprises in generally. But researches don’t take into account specific characteristics of each enterprise that can influence on the formed cost management mechanism. It is hard to predict the consequences of implementing such mechanism at the machine-building enterprises with its difficult production conditions. We should take into account the specific of the production of machine-building enterprises. To complete these circumstances we should remember that the development of the economy, the introduction of sanctions, different sectoral restrictions and currency changes also can cause unpredictable results. Moreover, all considered approaches don’t pay attention to the condition that the formed cost management mechanism should also include the possibility of its further efficiency evaluation. So finally, the problem statement is to form the mechanism of cost management is to form the mechanism of cost management enterprises based on the considered approaches of cost analyzing and cost management with special emphasis on tools, processes and time factor for implementing at the machine-building.

Research Questions

Include the study of the organizational and economic cost management mechanism based on time factor. It will emphasis attention of the economists on the components of cost management mechanism. Among most economists identify strategic and operational components (Esina et al., 2015). But operational approach involves the analysis of actual indicators and the development of standards and planned indicators for short periods of time (shift, day, decade, etc.) in relation to its research object (parts, assembly units, etc.). The amount of costs at this level is influenced by the system of operational and production planning. The determination of the actual production costs, directions of their reduction proposed by some authors within the framework of the operational approach, it should be attributed to the tactical stage of cost analysis. The organizational and economic cost management mechanism with the operational, tactical and strategic components allows us to identify current expenditures and capital expenditures for their further analysis. Based on above approaches of cost management mechanism in this article the system of cost effectiveness indicators is considered.

Purpose of the Study

Purpose of the study is to develop a cost management methodology using existing approaches of economists. This mythology is presented in the form of an organizational and economic cost management mechanism in relation to the high-tech machine-building enterprises. It seems that this mechanism will allow identify ways for cost optimization and cost effectiveness evaluation with the possibility of its further improvement. Organizational and economic cost management mechanism can be adapted to certain high-tech machine-building enterprises and business processes at these enterprises. Organizational and economic cost management mechanism, which formed as a result of our research, emphasizes attention on time factor. Based on time factor management of enterprises is realized cost analyzing and cost management with highlighting the operational, tactical and strategic components. As the result cost management will be implemented separately depending on short-term, mid-term and long-term periods and generally in all these periods as the whole.

Research Methods

The research is based on the на applied economic and empirical research methods. The study is based on the methodological aspects of the study based on the economic literature. Domestic and foreign economists dealt with the problems of cost management, the analysis of whose work made it possible to determine the provisions of the existing methods of cost management. By comparing statistical data of economic sourcebooks and abstract journals the modern ways of economic development and problems and opportunities of functioning of machine-building enterprises are revealed. The analyzed facts and statistical data on the development of machine-building enterprises, taking into account the trends of economic processes, made it possible to determine the basis of the positive and negative provisions of their further development. Methods of scientific abstraction and modeling were used to build an organizational and economic mechanism for cost management based on existing approaches. When grouping cost indicators, methods of analysis and synthesis were used.

Findings

While setting the organizational and economic cost management mechanism one should take into account the orientation of the mechanism on the characteristics and production conditions of machine-building enterprises. Such enterprises have specific features, as: the multi-product character of production, an imperfect regulatory framework, a large amount of unfinished production, the long duration of the production cycle and the high level of overhead expenses. And we must mention the fact that there are no global standards and unified methods for managing project costs at production enterprises (Smith, 2016). It is typical for machine-building enterprises the usage of foreign economic cooperation as a resource of high-quality components that can improve the quality of final product. The imposition of sanctions and sectoral restrictions, the fall of the ruble exchange rate in Russia either completely closed the possibility of using high-quality components, or dramatically increased the cost of such components. As a result all it makes the final products of most machine-building enterprises uncompetitive. Also it should be noticed that machine-building enterprises are needed in state support and involvement of borrowed financial funds. Among positive factors one should admitted that the existing structure in the machine-building industry in Russia, according to which all leading enterprises are part of large holding groups, gives more possibility for implementing development projects. It should be noted that for effectiveness cost management, the management of enterprises should adhere to the following principles:

systematic of cost management;

limited combination of cost reduction with high product quality;

methodological unity at all stages of the product life cycle;

avoiding unnecessary costs;

improving of information providing about the amount and classification of expenditures (costs).

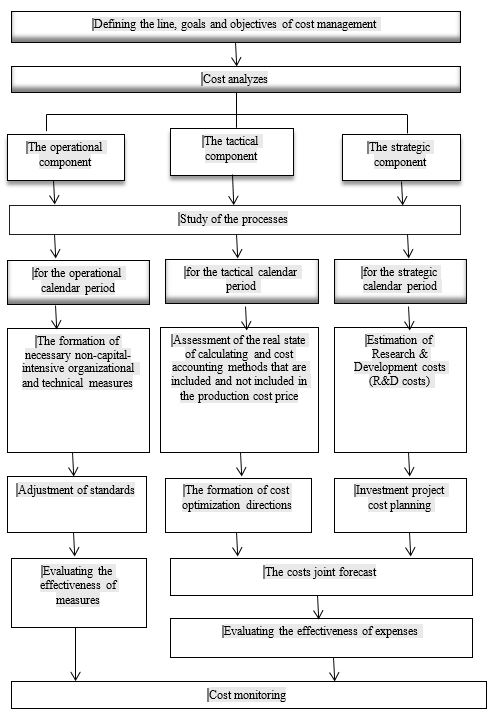

The organizational and economic cost management mechanism of machine-building enterprises should be formed by using three interrelated components: the operational component, the tactical component, the strategic component.

The operational component. The operational component should be focused on reducing current production costs. Cost improvement should be based on a complex of organizational and technical measures that are usually not capital-intensive and do not require considerable time on their development. The operational cost management takes into account internal environment of enterprises and is targeted at maximizing profits in the short-term period.

The tactical component. This component should also be focused on minimizing current costs. However, it is necessary to partially take into account capital expenditures, for example, in such cases as: during updating individual units of equipment when resolving issues whether to repair or buy units of equipment. Special attention should be paid to costs per unit of output, minimizing costs for individual technological processes.

The strategic component. The strategic component focused on changing the technologies used, the material and technical base of the production, the development and launch of a new product, entering new markets. All this is not possible without the formation and implementation of investment projects, which, accordingly, requires the study of both current and capital expenditures.

Current expenditures are carried out due to the production cost price and also include in bookkeeping calculation material costs, labor costs, costs for controlling production processes and product quality and other expenses. Capital expenditures are the annual expenses of creating non-current non-expendable assets. A joint study of current and investment costs in relation to emphasizing attention on time factor also requires separate study of costs formed on the basis of the cost price structure according to the accounting rules and also on the basis of their construction within the framework of cash flow generations. The research of current and investment costs on the basis of their construction within the framework of cash flow generations involves separating nominally monetary expenditures from cost structure, which, on the one hand, are expenses, and on the other hand do not lead to any transfers of funds. A joint study of current and investment costs also requires the research of a number of indicators in the effectiveness assessment of investment costs: capital expenditures; the liquidation value of equipment; interest rates and others. Risk analysis should also be included in the organizational and economic cost management mechanism. Based on the above, one can form an organizational and economic cost management mechanism, which is schematically presented in the Figure

Cost effectiveness evaluation should be carried out separately within the operational approach and within the tactical and strategic approaches. It is particularly difficult to jointly estimate cost effectiveness within the tactical and strategic approaches. To evaluate cost effectiveness within the tactical and strategic approaches we have to select and group a system of indicators. Selecting and grouping a system of indicators is a rather time-consuming and complex process, that requires compliance some criteria: the ability of quantifying the indicator; the economic feasibility of using the indicator that should show the comparability of benefits from its joint use together with costs; accessibility for understanding the operational and strategic meaning; the interconnectedness and the balance of indicators (Boyko, 2016). According to the machine-building enterprises it is advisable to highlight the following groups of indicators:

production processes costs;

organizational and management processes costs;

financial and commercial processes costs;

summary cost effectiveness indicators.

While accounting and costs calculating during implementing the organizational and economic cost management mechanism all grouped costs can be converted into expenses, thus reflecting the cost of certain elements in the value chain of machine-building enterprises (Papazov & Mihaylova, 2015). Based on the grouping of indicators shown above the system of cost effectiveness evaluation indicators in tactical and strategic approaches can be formed (Table

For the joint study of current and capital expenditures it is advisable to use an algorithm for calculating cash flows. It characterizes the money supply that circulates in an organization over a certain period in order to generate profit, ensure its viability and improve the welfare of owners (Rybalko, 2015). The annual cost will be is expressed as:

,

– amount of costs in a year;

- production cost price;

– depreciation;

– current costs that financed from profit;

– investment costs.

If the development investment project is implemented at the machine-building enterprises, change all key indicators of this enterprise including fixed assets. In the evaluating of the investment project accrued depreciation is not included in costs. But when describing the dynamics of costs for current activities, it significantly affects the level of costs. Therefore, it is necessary to study the dynamics of the depreciation without taking into account changes in nominal cash costs (the depreciation of fixed assets).

Conclusion

The paper presents the concept of an organizational and economic cost management mechanism. This concept is focused on the allocation of its components: operational, tactical, and strategic. The selection of operational, tactical, strategic in the organizational and economic mechanism of cost management revealed the necessity of study current expenditures and capital expenditures separately and also in aggregate at the same time. To crown it all operational, tactical and strategic approaches form the research on the basis of the cost structure according to bookkeeping rules, and on the basis of their construction within the framework of cash flows. So time factor plays an important role in cost management. It can give us more opportunities to foresee the major factors of cost reduction in the production of enterprises. The organizational and economic cost management mechanism also should be flexible for the conditions of high-tech machine-building enterprises and different economy situations. There must be opportunities for its analyzing and further development. In this case according the tactical and strategic approaches the indicators for evaluating cost effectiveness has been formed. At last the formula for the annual value of costs in the study of indicators for the joint study of current and capital expenditures is considered.

References

- Azriyah, A., Auzair, S., & Amiruddin, R. (2016). Cost management, entrepreneurship and competitiveness of strategic priorities for small and medium enterprises. Procedia – Social and Behavioral Sciences, 219, 84-90.

- Bebeşelea, M. (2015). Costs, productivity, profit, and efficiency: An empirical study conducted through the management accounting. Procedia - Social and Behavioral Sciences, 191, 574-579.

- Boyko, N. V. (2016). Complex approaches to evaluating the effectiveness of strategic management. Bulletin of the Bryansk State Technical University, 5(53), 75-82.

- Esina, O. N., Tereshenko, N. N., & Trusova, S. V. (2015). Methods of enterprise cost analysis based on the synthesis of strategic and operational approaches. Research Institute of Economic Strategies.

- Naugolnova, I. A. (2015). Organizational and economic mechanism for reducing costs at industrial enterprises (on the example of engine building). Abstract of dissertation. Samara State University of Economics.

- Papazov, E., & Mihaylova, L. (2015). Organization of management accounting information in the context of corporate strategy. Procedia – Social and Behavioral Sciences, 213, 309-313.

- Rybalko, O.A. (2015). The concept of cash flows and their role in the management system. In G. D. Akhmetova (Ed.), Proceedings of the IV International Scientific Conference Economics, Management, Finance (pp. 192-194). Zebra.

- Smith, P. (2016). Global professional standards for project cost management. Procedia – Social and Behavioral Sciences, 226, 124-131.

- Thiele, G., Heimann, O., Grabowski, K., & Krüger, J. (2019). Framework for energy efficiency optimization of industrial systems based on the control layer model. Procedia Manufacturing, 33, 414-421.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

30 April 2021

Article Doi

eBook ISBN

978-1-80296-105-8

Publisher

European Publisher

Volume

106

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1875

Subjects

Socio-economic development, digital economy, management, public administration

Cite this article as:

Streltsova, D. A. (2021). Organizational And Economic Cost Management Mechanism And Cost Effectiveness Indicators. In S. I. Ashmarina, V. V. Mantulenko, M. I. Inozemtsev, & E. L. Sidorenko (Eds.), Global Challenges and Prospects of The Modern Economic Development, vol 106. European Proceedings of Social and Behavioural Sciences (pp. 691-698). European Publisher. https://doi.org/10.15405/epsbs.2021.04.02.83