Transformation Of The Banking System

Abstract

The transformation of the banking system is a continuous and dynamic process that accompanies the banking system throughout the entire period of its existence. Every year banking systems of the world face new external challenges and internal crises that motivate them to retaliate. Successful overcoming of these challenges depends on flexibility of banking systems. The main instruments of this overcoming are forecasting the position of the banking system in various conditions, understanding real threats and challenges, identifying prerequisites of transformation, and creating scenarios according to which the transformation will take place. So, the issue of banking system transformation prerequisites identifying and detecting necessary instruments of its realization is one of the most important fields of research in the modern economic science. Existing internal and external political and social-economic conditions in Russia are prerequisites of the banking system transformation in the country. Studying processes that take place in the banking system we can estimate its actual transformation. To do it we should divide the processes into evolutionary (i.e. natural, which occur under the influence of the technological process and the implementation of modern cloud and Internet technologies) and revolutionary or forced (i.e., forced reforms within the system). Within this article the transformation is a factor that might contribute financial sustainability of the system. Using this approach as a basis we can not only estimate the ongoing reformation and processes in the banking system, but also propose a number of measures to improve the functioning of the banking system.

Keywords: Banking systemimprovement of financial sustainabilityprerequisites of the transformationtransformation

Introduction

Within the banking transformation issue it is necessary to take in account extensive and intensive processes that cause changes of the banking system structure, changes in a field of economic relations linked to banking system and changes of the environment where this system exists (Hamdaoui & Maktouf, 2020). Reasons of this transformations are different historical, political, social, and economic factors. Analyzation of the impact on foundation and development of banking system activities let detect prevail influence of economic factors that determine a natural transformation in the banking system in the face of a changing economic situation. These economic factors are growth of commodity and money relations and development of trading relations (especially international trade), growth of small handicraft and factory production, the need to ex and commercial and productions capital, and the lack of loans and their high cost. They caused the need of new credit relations, expanding of lending sizes, expanding of variety among banks and other credit organizations, interactions between banks and other credit organizations appear. So, the processes that were caused by the earliest factors of changes has become the factors of changes in the banking system themselves. There are also such factors as the interest of the governing classes in getting loans, the need for the development of cashless payments, the ongoing process of concentration and centralization of capital. In later periods the other factors are detected. They are emergence of emission functions, foreign capital influence and expanding of bills circulation etc.

Problem Statement

Every year the world's banking systems are facing new external challenges and internal crises that trigger them to respond. Successful overcoming of these challenges depends on the flexibility of banking systems. The main tools for overcoming these challenges are: anticipating the situation of the banking system in various conditions, calculating real threats and challenges, determining the prerequisites for transformation, as well as developing scenarios for the transformation.

It should be noted that there are a lot of studies and points of view in the issue of transformation and functioning of the banking system. The banking system has a long history of the formation and ongoing transformation processes. But, despite the diversity of the number and profundity of scientific studies there are still controversial points among scientists since most of the works are aimed at studying a specific type of banking activity, certain areas of interaction within the banking system, and the interaction of the banking system with the environment. Therefore, there is a conclusion that the insufficient level of development of the issue leaves a space for further scientific research.

Research Questions

The issue of banking sector development in the current conditions of the Russian economy is quite relevant. At present, there is a need to consider and study a number of issues related to the banking sector development trend in Russia. The issue that is described in the article need to have a complex theoretical study and basis with clearly defined and structured stages and tasks. First of all it is necessary to analyze factors that have an impact on transformation of the banking systems. Then their typology is needed in terms of natural (evolutionary) transformation and forced transformation caused by crisis processes in the economy. What is more, it is necessary to detect factors that threaten financial stability of the Russian banking system. Practical part of study is aimed, firstly, at identifying the most obvious prerequisites for the transformation of the banking system of Russian, and secondly, at proposing a number of measures to improve the functioning of the Russian banking system with a purpose to enhance its financial sustainability. The results and conclusions obtained in the course of the research may serve as a basis for designing further development of the Russian banking system.

Purpose of the Study

The purpose of the study is to solve a scientific problem which consists in studying theoretical and methodological issues of the essence, features of the functioning of banking systems, identifying the most obvious prerequisites for the transformation of the banking system of Russia and proposing a number of improvement measures aimed at increasing financial stability of the banking system. The efficiency of the banking system in modern conditions largely depends on the quality of the analysis of market segments. Object of the study is the transformation process of the banking system in Russia. The subject of the study is economic and institutional relations that are developing in the process of functioning and development of modern banking systems. The issues of the research are economic and institutional relations that develop during the functioning of modern banking systems. The information basement of the research is a data of statistical and rating studies of the Central Bank of Russia, domestic and foreign agencies, scientific publications, periodicals, Internet resources on the topic of the study.

Research Methods

There is no doubt that the banking system is a dynamic system, constantly evolving and evolving. However, not all these processes lead to significant changes in the system, namely, they are the distinctive characteristics of the transformation. The reliability of the conclusions and recommendations obtained in the study is ensured through the use of general scientific methods and technologies of scientific knowledge including experimental and theoretical methods (comparison, analysis, generalization, systematization), technologies of tabular and graphical interpretation, methods of econometric analysis. Also, when assessing the financial condition of the banking system, various financial indicators were analyzed. Based on the retrospective analysis used in the study, we were able to demonstrate the transition from one state to another and how this transition process can be successfully used to improve the financial stability of the system. The results of the conducted fundamental research are arranged in accordance with the algorithm. The transformation scenario consists of three main stages: prerequisites, tools and transformation results.

Findings

The problem of insolvency of the banking market, i.e. the fiasco of the market is quite acute for the current banking system of Russia. An actual and priority solutions for this problem which threatens the financial sustainability of the banking system is the targeted use of its transformation process. The first group of problems, which is the source of the failure of the banking market that can be solved with the correct use of transformation tools is associated with the need to own and use objective and complete information. The asymmetry of information in the banking sales market while making transactions of a different type (credit, investment, trust, etc.) is two-sided. Incomplete information can be provided by both a bank's representative and a client (Kuzmina et al., 2020). Asymmetry is shown in its uneven distribution between the parties of the transaction. Banks use various methods and ways of customer verification (scoring tests, analyzing credit histories, checking by security service, underwriting, etc.) to protect themselves.

But, risks of a client often are caused by not having sufficient knowledge in the field of bank operations, bankruptcy of a commercial bank, hidden fees, poor-quality and unfair contract. Within the clients’ safety issue there are some problems of information asymmetry from a side of banking organization. To maintain the safety and stability of the banking market the state adopts laws, regulations etc. Examples of such actions on the part of a government are creation of a deposit insurance system (Qian et al., 2019), licensing of banks, supervisory measures, etc. There are measures to prevent such a failure through the transformation of the banking system. It is worth focusing on the innovations of digital development (Tekic & Koroteev, 2019). Thus, the toolkit of banking organizations in obtaining "fast" and high-quality information about the client expands, as well as to include as many banking organizations as possible in the implementation of solutions for the availability of information to clients about banking activities, so that potential clients can rely on objective and general information about the banking market. Also, it is important to make as many banks as possible to find solutions of providing sufficient information about banking activities to their clients. This action will provide objective and general information about banking market as a basis for potential clients.

In the process of these measure realization it is important to take in account a back side of a pure market that might have a negative effect on competition and development of the banking market (Agoraki et al., 2019). During supervising actions in the banking system of Russia problem of a partial insolvency in estimating of local and jurisdictional commercial banks’ activities of regional departments of the Bank of Russia was detected. These incidents indicate the desire of the departments to prove their effectiveness and the need for the presence of a sufficient number of commercial banks in control. Therefore, they ignored their unstable financial situation, and these facts show illegal and dishonest realization of their duties. As you can see, this failure of the banking market was mitigated out by the transformation of the Russian banking system, i.e. by implementing the reform of the centralization of banking supervision.

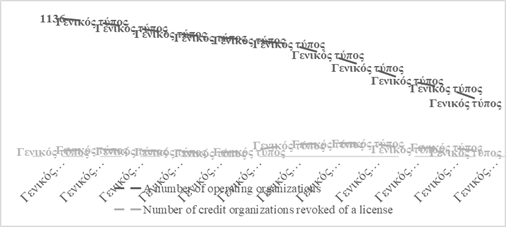

The second reason of market failure is caused by imperfect competition. From our point of view reasons of it are clear. We will explain them. Firstly, lager banks can easily take over smaller regional banks that cannot withstand the competition. In these situations, a merger, voluntary takeover is possible, another option is that the smaller banks go bankrupt (Baltas et al., 2017). Further, private reorganization by a large regional bank takes place. This situation decreases a number of alternative banks for clients. Regional banking market closes with the monopoly of the leading bank in the region. Secondly, the reason that have a negative impact on competition in the banking market are collusion of bank managers that also reduce the number of players in the market. Examples of collusion include a pre-divided market and its segments, audience, and various types of banking services. In the first and second situations, it is possible to see another reason of the market failure that is the external monetary effect. Undoubtedly, lager and more influential banks put pressure on small commercial banks with their pricing policy as their money turnover and a wide range of banking services and accumulated client base allow to reduce the cost of the services (Chen & Zhu, 2019). Thirdly, it is «objective» bankruptcy of commercial banks. This problem might be explained as one that occurs due to the influence of external factors since the first two reasons are “intent” and internal influence. The banking market is characterized by the presence of insolvent organizations. Also, these insolvent banks’ market share and the sensitivity of their bankruptcy are also important. In fact, this problem also implies the following. A large-scale audit of the activities of commercial banks in Russia led to the understanding that large banks are also exposed to risk and it is necessary to take measures to keep the country's banking market from failure. Figure

Data from the Figure

Now we describe a new rehabilitation process for commercial banks in Russia created by the Bank of Russia. A new Fund of banking sector consolidation is a tool to avoid bankruptcy of important banking organizations. Now the banking system of Russia with the Bank of Russia as a leading organization and with support of the government can realize rehabilitation and reorganization of commercial banks. It was necessary and possible because of several reasons that threatened the banking system of Russia with market failure. Crisis financial situation and insolvency of commercial banks became transparent (information from top-managers or auditing organizations) as well as a ban on commercial banks from resorting to international lending from foreign organizations (a consequence of the sanctions measures). The inconsistency of this situation lies in the fact that large private banks fell under the reorganization. Their assets are now largely owned by the Central Bank of the Russian Federation. These banks are PJSC Bank FC Otkritie, PJSC Binbank, PJSC Promsvzbank, etc. Thus, the banking system of the country while offering this effective way to improve and to rehabilitate the banking market has also created a risk of ineffective return of the measures. An example is the concentration of a significant number of assents in hands of the Bank of Russia and the state which according to experts’ forecasts will be difficult to transfer to private management. Further, we note the influence of the technological external effect and the network effect on the banking market. A feature of these effects is their duality. They cause market failure and also they are a tool for minimizing the risk of failure caused by other reasons. The negative impact of the technological external effect is based on the risk of reducing the participation of bank representatives in financial transactions. Thus, smart contracts, digital platforms and applications allow excluding the bank as an intermediary from a number of financial transactions. Consequently, the income of banks decreases (especially those based on commission transactions, currency transfers, cross-border payments, etc.), competition with representatives of the non-banking sector for a number of services increases, the costs of banks increase, and, consequently, the cost of their services, etc.

A reasonable way out is the development and implementation of digital technologies by the banks themselves in the work within the banking infrastructure and in the work with clients (Chmielarz & Zborowski, 2020). It might be noted that the risk of failure in this case is relatively small since the use of digital technologies largely contribute the development of the banking system in general. For example, blockchain technology has aroused great interest in the Russian banking market. Various banks are currently offering pilot versions of blockchain solutions on the Masterchain platform: messaging system (Central Bank of the Russian Federation), power of attorney exchange and factoring (PJSC Sberbank of Russia), exchange of digital letters of credit (JSC Alfa-Bank), distributed register digital bank guarantees (PJSC VTB), fraud accounting service (PJSC Bank FC Otkritie), fast exchange of payments (Payment system QiWi). Thus, we note that the transformation of the banking system in the field of transition to a digital platform is an effective measure to prevent failures of the banking market. One of the features of the banking market is that it is closely connected with other economic markets, and this connection is two-way, i.e. the spillover effect for the banking market is a widespread phenomenon and the regulation of its influence is an important task in preventing failures (Djalilov & Piesse, 2019). There are some examples of the negative consequences of the spillover effect on the banking market and ways to address them. Changes in the currency exchange market inevitably lead to changes in indicators in the banking market, this situation is aggravated by economic and political events which resulted in the need to create a national payment system. NPS MIR is designed to stabilize the national banking market and the stability of the national currency within the country. The active development of digital letters of credit in the money market also affects the banking market and the system in general. In this case the market failure can be caused by lagging behind current trends and customer requirements. It is solved by analysis of the market and the implementation of popular trends.

Conclusion

As can be seen from the examples given in the study prevention of the emergence and elimination of failures in the Russian banking market is possible in three different ways that are used in modern realities. The first one is a government regulation in the banking services market. The second is an independent transformation of the banking system (Panova, 2020; Sidorenko & Lykov, 2020). The third is the self-regulation of the market by consumers. All three processes are taking place in the context of a real transformation of the Russian banking system. The reasons for these failures are often the prerequisites for transformation as a result of which there is a conscious or intuitive use of certain transformation tools.

In the study there are presented different stages of the banking system transformation in Russia that might prevent and eliminate failures of the banking market. We analyzed and estimated changes in different directions of banking system activities. They are centralization of banking audit, implementation of digital technologies, two-tier licensing, reorganization with the help of FKBS, creation of NPS MIR, etc. Using this research, we can make a conclusion that process of transformation contradictory in its results. There are pros and cons in each of these cases. And sometimes the presence of negative tendencies is a necessity for achieving an overall positive result. Therefore, when realizing any measures it is necessary to maintain the "golden mean" which will help to establish an effective market mechanism, without infringing on the interests of some market participants and not exalting the interests of others.

References

- Agoraki, M. K., Kouretas, G. P., & Triantopoulos, C. (2019). Democracy, regulation and competition in emerging banking systems. Economic Modelling, 84, 190-202.

- Baltas, K. N., Kapetanios, G., Tsionas, E., & Izzeldin, M. (2017). Liquidity creation through efficient M&As: A viable solution for vulnerable banking systems? Evidence from a stress test under a panel VAR methodology. Journal of Banking & Finance, 83, 36-56.

- Chen, J., & Zhu, L. (2019). Foreign penetration, competition, and financial freedom: Evidence from the banking industries in emerging markets. Journal of Economics and Business, 102, 26-38.

- Chmielarz, W., & Zborowski, M. (2020). The selection and comparison of the methods used to evaluate the quality of e-banking websites: The perspective of individual clients. Procedia Computer Science, 176, 1903-1922.

- Djalilov, K., & Piesse, J. (2019). Bank regulation and efficiency: Evidence from transition countries. International Review of Economics & Finance, 64, 308-322.

- Hamdaoui, M., & Maktouf, S. (2020). Financial reforms and banking system vulnerability: The role of regulatory frameworks. Structural Change and Economic Dynamics, 52, 184-205.

- Kuzmina, O. Y., Konovalova, M. E., & Chulova, E. S. (2020). Transformation of the banking system as a way to minimize information asymmetry. In S. Ashmarina, M. Vochozka, & V. Mantulenko (Eds.), Digital Age: Chances, Challenges and Future. Lecture Notes in Networks and Systems, 84 (pp. 12-18). Springer.

- Panova, G. S. (2020). Cryptocurrency – Money of the digital economy. In S. Ashmarina, M. Vochozka, & V. Mantulenko (Eds.), Digital Age: Chances, Challenges and Future. Lecture Notes in Networks and Systems, 84 (pp. 604-612). Springer.

- Qian, N., Zhang, K., Zheng, C., & Ashraf, B. N. (2019). How do regulatory ability and bank competition affect the adoption of explicit deposit insurance scheme and banks’ risk-taking behavior? International Review of Economics & Finance, 61, 69-90.

- Sidorenko, E. L., & Lykov, A. A. (2020). Prospects for the legal regulation of central bank digital currency. In S. Ashmarina, M. Vochozka, & V. Mantulenko (Eds.), Digital Age: Chances, Challenges and Future. Lecture Notes in Networks and Systems, 84 (pp. 613-621). Springer.

- Tekic, Z., & Koroteev, D. (2019). From disruptively digital to proudly analog: A holistic typology of digital transformation strategies. Business Horizons, 62(6), 683-693.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

30 April 2021

Article Doi

eBook ISBN

978-1-80296-105-8

Publisher

European Publisher

Volume

106

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1875

Subjects

Socio-economic development, digital economy, management, public administration

Cite this article as:

Ovsyannikova, E. E., & Chulova, E. S. (2021). Transformation Of The Banking System. In S. I. Ashmarina, V. V. Mantulenko, M. I. Inozemtsev, & E. L. Sidorenko (Eds.), Global Challenges and Prospects of The Modern Economic Development, vol 106. European Proceedings of Social and Behavioural Sciences (pp. 1082-1089). European Publisher. https://doi.org/10.15405/epsbs.2021.04.02.129