Standards For Forming Non-Financial Reporting: Practice Of Application In Russia

Abstract

The study describes methodological features of non-financial information by economic entities. The authors conducted a comparative analysis of non-financial reporting standards used in world and Russian practice, noted the characteristic features of information disclosure in the application of each of them. The content of the basic reporting indicators developed by the Russian Union of Industrialists and Entrepreneurs for the possibility of their use by companies in corporate non-financial reports to reflect key performance results is also analyzed. A comparative analysis of the studied standards for non-financial information disclosure allows us to conclude that there are differences in approaches to non-financial reporting described in the standards. Each of the standards has a number of key advantages, the use of which together will allow business entities to improve the quality and transparency of non-financial information. The formation of non-financial reporting should be carried out using separate methods of previously considered standards (elements of GRI G4 should be used to characterize the relationship of economic, social and environmental activities). ISO 14001-2016 Environmental Management Systems will improve the quality of information on environmental activities and performance characteristics of ongoing activities. In Russia, an integrated approach to the formation and presentation of non-financial reporting may be a new stage in promoting ideas in the field of corporate responsibility and sustainable development.

Keywords: Non-financial reportingenvironmental reportingintegrated reportingstrategic reportingtransparencysustainable development

Introduction

A non-financial report is a set of reliable and related descriptions of the company’s activities and the results of its achievements related to sustainable development policies of interest to stakeholders, among which are investors, shareholders, employees, government agencies, various civil society institutions, and the media. A non-financial report plays an important role in forecasting risks, assessing competitiveness, as well as in a significant range of issues related to the quality of management, ethics of business personnel, the effectiveness of social investments, etc. These factors have a significant impact on the business reputation of the company, which largely affects economic consequences in future.

The increasing role of business and increasing requirements for transparency and openness of reporting is becoming an increasingly relevant topic for modern companies. Along with this, the topic of social responsibility comes to the fore, which covers economic, environmental and social activities of companies. Therefore it requires close attention and consideration of the needs of stakeholders. To achieve these goals, more and more companies are beginning to apply universal principles of corporate responsibility as a factor in effective management.

One of the tasks of economic entities is to develop a comprehensive system recording the results of activities that can be presented to stakeholders. It is assumed that companies should be held accountable to society. The legal liability of the company extends by providing information on environmental and social consequences of the company.

Currently, much attention is paid to environmental activities, especially in multinational large companies, which have found that maintaining the environment is necessary to achieve competitive success in the long term. In this regard, it is advisable for economic entities to generate reports with non-financial indicators.

Problem Statement

Over the past two decades, a significant number of studies have been carried out involving theories of environmental disclosure in the reporting of companies in developed countries. These theories include the theory of political economy, the theory of legitimacy, the theory of beneficiaries, and organizational theory (Noodezh & Moghimi, 2015). The practice of environmental reporting is being actively studied in the works of scientists such as Benlemlih, Shaukat, Qiu, and Trojanowski (2018), Chelli, Durocher, and Fortin, (2018), Crowther, (2017), Haque and Ntim, (2018), Higgins, Stubbs, and Milne, (2018), Lau, Lu, and Liang, (2016), Pucheta Martinez and Gallego, (2018), Schreck and Raithel, (2018).

In Russian practice, the development of non-financial business reporting is supported by the Russian Union of Industrialists and Entrepreneurs (RSPP), which considers reporting as a tool to improve operations and increase transparency. One of the directions of its activity is the development of tools that will allow Russian companies to adapt to international standards of corporate responsibility and social reporting.

In order to manage, assess the current situation and set strategic goals in the field of environmental activity, business entities need to measure and present results of this activity to users. At the same time, Russian companies can choose their own methods for measuring and presenting them on their own, which ultimately makes it difficult for the user to compare the presented non-financial information with the data of other organizations. Moreover, the lack of comparability leads to information asymmetry, which:

Does not allow correctly measuring and evaluating activities;

Makes it impossible to make a homogeneous comparison over time, not only within one company, but also in comparison with others;

It does not make it possible to achieve the amount of information necessary for interested parties.

Research Questions

In accordance with the identified problems in the field of non-financial reporting methodology, the following questions were formulated in the framework of this study:

- What disclosure standards in non-financial reporting are applied by Russian companies today?

- What proposals regarding the regulation of information in non-financial reporting can increase its transparency?

Purpose of the Study

The purpose of the study is to develop recommendations regarding the regulation of non-financial reporting based on the analysis of progressive world experience. Based on the purpose, the following tasks were formulated:

- Analyze information disclosure standards in non-financial reporting used in Russian and foreign practice;

- Develop proposals for regulating information in non-financial reporting to increase its usefulness to the user.

Research Methods

Research hypothesis formation

The presentation of non-financial reporting of activities with high information value for stakeholders by Russian companies presents significant requirements for the tools used by compilers.

Н1 The use of basic indicators developed by the Russian Union of Industrialists and Entrepreneurs enables companies to present non-financial information on the results of environmental and social activities of a business in accordance with the concept of sustainable development based on systematic characteristics of results.

H2 The development of an integrated standard by types of non-financial information and its use as a regulatory tool will help increase transparency of reporting.

Research methodology

Methods were used to analyze on-financial reporting of Russian business entities and synthesize the prevailing approaches to information disclosure on the results in order to form a reasonable opinion about the established practice of preparing and presenting this type of information in reporting.

Data collection procedure

In the course of the study, the Basic indicators developed by the Russian Union of Industrialists and Entrepreneurs as a tool for systematic information disclosure on indicators related to economic, environmental and social activities by business entities were analyzed.

Information on each indicator is formed in the form of a passport (Table

Findings

To disclose information and meet the needs of interested users of the company, several reporting standards are used to properly disclose the interaction of economic, environmental and social information in the world and Russian practice of forming non-financial reporting, including:

- GRI 419: Socioeconomic Compliance Sustainability Reporting Guide, Global Reporting Initiative (GRI 419: Socioeconomic Compliance, Sustainability Reporting Guide, Sustainability Reporting Guide, Global Reporting Initiative, 2016);

- AA1000 Assurance Standard (AA1000 Assurance Standard, Accountability, 2008);

- GOST R ISO 14001-2016 Environmental Management Systems (GOST R ISO 14001-2016 Environmental Management Systems, Requirements and application guidelines, national standard of the Russian Federation, 2016).

Sustainability Reporting Guidelines of the Global Reporting Initiative GRI G4 is an international standard that companies use on a voluntary basis to report on sustainable development activities. A feature of the standard under consideration is the ability of the reporting entity to apply recommendations in stages, starting from general principles (for example, in the first applications of GRI G4) and ending with the whole set of indicators.

Sustainability Reporting Guidelines of the GRI G4 Global Reporting Initiative contain general aspects of reporting by economic entities, regardless of size, industry, or location. This standard assumes information disclosure in the Sustainability Report according to the following criteria: organization’s activity strategy, significant aspects of work, management and interaction with stakeholders. It should be noted that the GRI G4 standard enables the company to disclose information not only about economic activity, but also its relationship with the implementation of social and environmental activities. Thus, this standard is the most general and allows you to reveal the existing interdependencies of managing different areas of the economic entity.

GRI G4 in Russia is used most actively in comparison with other reporting systems. However, the use of the standard is not widespread.

AA1000 AS Social Reporting Standard for companies contains a set of criteria for disclosing information in terms of ethical positions for conducting social and ethical audits, and also directly describes the procedure and the set of criteria used for this. A distinctive feature of the standard is direct interaction with interested users of reporting in its preparation. The application of the standard implies the compilation of a set of conclusions and recommendations, including a guarantee statement and a report to management. In Russia, it is practically not used, only in combination with other reporting systems.

ISO 14001-2016 Environmental Management Systems. Requirements and guidance sets the criteria for the environmental management system and can be voluntarily used by companies to improve resource efficiency, reduce losses and costs. As part of this standard, it is advisable to disclose information about the organization’s environment, the operation of the environmental management system, environmental policy and management’s attitude, as well as the implementation of the “Plan - Do - Check - Act” concept. According to the data of the International Organization for Certification in Russia, 799 certificates of conformity ISO 14001-2016 were issued.

To solve the problems of information asymmetry in non-financial reporting by the Russian Union of Industrialists and Entrepreneurs (RSPP), the basic performance indicators were developed. They represent a tool for quantitative, qualitative values of performance results, which are an element of corporate governance that helps to improve risk management and contributes to sustainability and competitiveness of the company in the long term. The development of the basic indicators was carried out taking into account international standards, legislative acts of the Russian Federation, as well as the practice of Russian and international companies and the specifics of business development in the country as a whole.

The functional purpose of the basic indicators of the RSPP in non-financial reporting:

Principles of responsible business;

Tool for interaction with stakeholders;

System of sustainability indicators;

Systematic view of performance;

Improved management system;

Ability to compare non-financial reports of companies.

The basic indicators of the Russian Union of Industrialists and Entrepreneurs represent a set of 48 indicators Their quantitative ratio according to the lines of activity is as follows: economic - 8 indicators, environmental – 18 indicators, social – 22 indicators. These 48 indicators are also divided by the degree of importance for the user into the main (29 indicators) and additional ones (19 indicators). In non-financial reports, information on indicators should be consistently compiled by companies and presented in dynamics for at least three years (for the reporting year and two years preceding it).

Conclusion

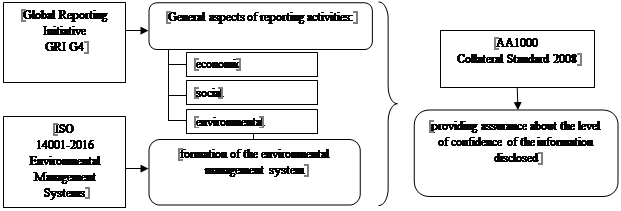

A comparative analysis of the studied standards for non-financial information disclosure allows us to conclude that there are differences in approaches to non-financial reporting described in the standards. Each of the standards has a number of key advantages, the use of which in combination will allow Russian business entities to improve the quality of non-financial information. The formation of non-financial reporting should be carried out using separate methods previously considered standards. So, the elements of GRI G4 should be used to characterize the relationship of economic, social and environmental activities. ISO 14001-2016 Environmental Management Systems will improve the quality of information on environmental activities and the performance characteristics of ongoing activities. AA1000 Collateral Standard 2008 is well applicable to reporting in order to present a guarantee of disclosed information and its compliance with confidence levels to form a definite judgment by users regarding the reporting of an economic entity.

The developed set of methods for disclosing non-financial information (Fig. 01) can be used as the basis for a standard that will increase the level of transparency of reporting information.

According to the authors, when using such a set of methods, the structure of a non-financial report can be as follows:

Management structure of the organization - describes the organizational and managerial structure of the organization for users to understand information;

Characteristic features of the activity – reveals the features of the activity that will allow users to most accurately evaluate the activity;

A system for ensuring the interaction of economic, environmental, and social activities — describes practical relationships;

Essential aspects of the activity – discloses the key indicators of the organization;

Business model of the organization - discloses positive and negative relationships with the environment;

Information disclosure principles – describes the principles on information formation.

Statement of compliance with confidence levels – discloses the aspects the allow concluding the fact that one of the two levels of confidence is consistent. An important aspect of the application of the standard is the disclosure of compliance with one of two levels of confidence: high and moderate.

The report is based on the following basic principles for the preparation of information: relationships with stakeholders, accountability; transparency; context of sustainable development; materiality. In this case, it is necessary to adhere to qualitative characteristics, which include comparability; timeliness; understandability; fullness; reliability.

Thus, the proposed report will be a separate document, which is an annex to financial statements, and may also be an annex to the report on sustainable development (if any). As additions, if necessary, the report may contain a set of conclusions in which certain aspects of its content are disclosed. The organization should also disclose information on the practical application of the Standard: on actions aimed at ensuring its use at all levels of the organization. The application of the Standard is possible by organizations of private and public sectors, large and small, both in developed and developing countries.

References

- AA1000 Assurance Standard, Accountability. (2008). Retrieved from: http://www.corporateregister.com/content/DefinitionAA1000AS08.pdf Accessed: 31.08.2019.

- Benlemlih, M., Shaukat, A., Qiu, Y., & Trojanowski, Y. G. (2018). Environmental and social disclosures and firm risk. Journal of Business Ethics, 152(3), 613-626.

- Chelli, M., Durocher, S., & Fortin, A. (2018). Normativity in environmental reporting: A comparison of three regimes. Journal of Business Ethics, 149(2), 285-311.

- Crowther, D. (2017). A social critique of corporate reporting: A semiotic analysis of corporate financial and environmental reporting. London: Routledge.

- Feoktistova, E., Alenicheva, L., Kopylova, G., Ozeryanskaya, M., Purtova, D., & Honyakova, N. (2019). Analytical review of corporate non-financial reports: 2017-2018 release. Moscow, D.C.: RSPP. [in Rus.].

- GOST R ISO 14001-2016 Environmental Management Systems. Requirements and application guidelines, national standard of the Russian Federation. (2016). Retrieved from: http://docs.cntd.ru/document/1200134681 Accessed: 01.09.2019.

- GRI 419: Socioeconomic Compliance, Sustainability Reporting Guide, Sustainability Reporting Guide, Global Reporting Initiative. (2016). Retrieved from: https://www.globalreporting.org/standards/gri-standards-download-center/ Accessed: 02.09.2019.

- Haque, F., & Ntim, C. G. (2018). Environmental policy, sustainable development, governance mechanisms and environmental performance. Business Strategy and Environment, 27(3), 415-435.

- Higgins, C., Stubbs, W., & Milne, M. (2018). Is sustainability reporting becoming institutionalized? The role of an issues-based field. Journal of Business Ethics, 147(2), 309-326.

- Lau, C. M., Lu, Y., & Liang, Q. (2016). Corporate social responsibility in China: A corporate governance approach. Journal of Business Ethics, 136(1), 73-87.

- Noodezh, H. R., & Moghimi, S. (2015). Environmental costs and environmental information disclosure in the accounting systems. International Journal of Academic Research in Accounting, Finance and Management Sciences, 5(1), 13-18.

- Pucheta Martinez, M. C., & Gallego, A. I. (2018). Environmental reporting policy and corporate structures: an international analysis. Corporate Social Responsibility and Environmental Management, 25(5), 788-798.

- Schreck, P., & Raithel, S. (2018). Corporate social performance, firm size, and organizational visibility: Distinct and joint effects on voluntary sustainability reporting. Business and Society, 57(4), 742-778.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

09 March 2020

Article Doi

eBook ISBN

978-1-80296-078-5

Publisher

European Publisher

Volume

79

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1576

Subjects

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Arkhipova*, N., Gafurova, D., & Potasheva, O. (2020). Standards For Forming Non-Financial Reporting: Practice Of Application In Russia. In S. I. Ashmarina, & V. V. Mantulenko (Eds.), Global Challenges and Prospects of the Modern Economic Development, vol 79. European Proceedings of Social and Behavioural Sciences (pp. 246-252). European Publisher. https://doi.org/10.15405/epsbs.2020.03.35