Development Of Methods For Monitoring Economic Security Of An Economic Entity

Abstract

In the modern conditions, economic security of the country is possible only with the operation of high-tech production, which provides leading economic sectors with high-quality resources that allow them to produce competitive products of the world level. The Economic Security Strategy of the Russian Federation until 2030, published in May 2017, identified the main directions and objectives of state policy in this area. At the moment, the stage of improving the mechanism of monitoring economic security is being implemented. Economic security of the country is directly dependent on the state of economic security of resident economic entities. It is economic security of enterprises, its scope, structure and efficiency that are one of significant competitive components of domestic economic entities and the development of the national economy as a whole. The study analyzes conceptual foundations of economic security and approaches to it. The authors propose a methodology for monitoring economic security of an economic entity, which includes nine key stages. The content of each of the stages, internal and external factors affecting the level of economic security, as well as some tools to improve it (implementation of a compliance system) were determined. The methods for assessing the target values of economic security indicators of an economic entity are defined.

Keywords: Economic securitymonitoring the level of economic securityindicators of economic securityeconomic entity

Introduction

In accordance with the Economic Security Strategy of the Russian Federation until 2030 (Presidential Decree No. 208), the key focus of this area is to counter challenges and threats to economic security, to prevent crises in resource, raw materials, industrial, scientific, technological and financial spheres, as well as to prevent a decline in the quality of life of the population.

The first stage of this strategy implementation, the duration of which is indicated until 2019, is the development of organizational, legal and methodological measures to ensure economic security. However, the development of both methods and tools for managing economic security should be based on a fundamental understanding of processes and factors forming it, without which the entire system of principles, paradigmatic models and concepts will have a low effect and can create a risk zone for the domestic economy.

Currently there is no single point of view on the definition of economic security of an organization. Theoretical, instrumental and methodological aspects of this scientific field are in the start-up phase.

From the standpoint of the study, the state is one of the parties that form the economic security system and are members of the world community, the functioning of which is impossible without the adoption of theoretical foundations by other participants: economic entities and representatives of human community.

Economic entities, their business activity and a balanced development are one of the main incentives for the country’s economic growth. In connection with the urgency of this problem, it is necessary to develop a methodology for identifying and analysing the factors destabilizing economic security of an economic entity, based on balancing the interests of key stakeholders at various levels in accordance with strategic principles of the socio-economic development of the Russian Federation.

Russian companies have to adapt to the conditions of socio-economic and political instability, to be in constant search for solutions to emerging problems and ways to reduce threats to their functioning in the market. The lack of financial resources, including working capital, the aging of production technologies and apparatus and the rupture of cooperative ties forced many companies to fight for their existence. As a result, for the overwhelming majority of Russian enterprises, the task of creating an economic security system that will reduce the level of threats to the enterprise’s economic activities in its main areas of activity (financial, economic, social, etc.) is urgent. Maintaining economic security of an enterprise is ensuring the most efficient use of its resources in order to prevent risks, significant deviations from the benchmarks of the overall security strategy, as well as creating conditions of stable functioning of its main elements.

Problem Statement

At the moment, issues related to ensuring sustainable economic growth of Russian companies are becoming increasingly relevant. It can be affected by the general economic situation in the Russian Federation in particular and in the world as a whole. The situation in the country, in addition to a number of other aspects, depends on the ability of the relevant state bodies to ensure not only economic security of the country itself, but also the companies. At the same time, companies in various industries should make their own efforts to ensure their economic security. In modern economic conditions, which are characterized by instability and multidimensionality of economic relations, the development and implementation of the economic security strategy is urgent.

Even though issues related to economic security have recently become of particular relevance, the overwhelming majority of research in this area relates to security at the state level. Despite the fact that an enterprise is a key element of the economy, the issues of ensuring economic security at the level of an economic entity are not fully studied (Arbuzov, 2016).

In the modern conditions, characterized by an open competitive environment, economic and political instability, business entities have complete autonomy in terms of decision-making in the field of the strategy development, choice of counterparties, organization of production and marketing of the product, sources of financial resources and other management decisions (Jerry & Ramesh, 1989). Virtually all the risks associated with doing business are now borne by entrepreneurs. In this regard, the problems of the survival of companies and ensuring their economic security are of paramount importance (Janioglo, 2017).

The overwhelming majority of Western scientific papers relate to security at the level of the individual and the country. Busan et al. (1998) explain this circumstance by the fact that an enterprise does not claim to be a security object due to contradictions between its ephemeral nature and the logic of existing security threats. In their opinion, an enterprise acts mainly as a functional security actor, influencing the safety dynamics in the relevant industry.

Messier (2014) also noted that economic security of society is more than just economic security of its constituent entities or the market, which is associated with the state’s role in the economy. Despite this, in transitional conditions to market relations by post-Soviet countries, issues related to ensuring economic security of an enterprise are becoming increasingly important, however, they are still not sufficiently studied.

According to Glumov and Kiselitsa (2013), economic security of an enterprise is the effective use of resources in order to level the threats and ensure the stable and effective functioning of this enterprise in this and future periods. They emphasize that economic security of an enterprise is characterized by a set of quantitative and qualitative indicators, the main one is the level of economic security, which is the result of evaluating the performance of enterprise resources in terms of economic security criteria.

As was shown above, in the scientific literature there is no unambiguous approach to the definition of the term “economic security of an enterprise”. In the studies of Russian scientists, economic security of an enterprise is understood as the most efficient use of resources in order to eliminate threats, minimize risks and significant deviations from the benchmarks of the overall security strategy. The position on ensuring economic security in a number of Russian companies is far from satisfactory. In foreign countries, more attention has traditionally been paid to the above aspect of financial and economic activities, since the experience of operating in market conditions for enterprises abroad is much richer than for Russian ones. At the same time, Russian economy differs from the progressively and steadily growing economies of developed countries. The normal activity of domestic companies and enterprises in today’s competitive environment requires more and more management skills. At present, a variety of monographs, works, guidelines, textbooks and dissertations consider such aspects as the organizational structure of an enterprise, an enterprise management system, management accounting, controlling, accounting, auditing, document flow, personnel policy, internal control, risk management, etc. (Cook, 2016). However, in the overwhelming majority of cases, the above issues are considered without taking into account the need to ensure economic security of a complex, which is a modern enterprise (Gaponenko, Bespalko, & Vlaskov, 2007).

As a result, for the overwhelming majority of Russian enterprises, the challenge is to create a management system that allows them to ensure economic security by reducing the level of threats to this business in its main areas of activity (financial, quality, resource management, etc.).

Thus, for the purposes of economic security in organizations, it is advisable to create a system of indicators for monitoring. The completeness and adequacy of a system of indicators affects the accuracy of the assessment of economic security of an enterprise.

Such a system should include a set of measures to prevent and repel hazards, corresponding to the scope and nature of threats.

Research Questions

As part of this study, the following research questions were highlighted:

What are the key characteristics of economic security of an economic entity in modern scientific research?

What is the role of economic security of an economic entity in the economic security system of the state?

How is economic security of an economic entity monitored?

Purpose of the Study

As part of the study, the following purposes were set:

Determine the mandatory stages of monitoring economic security of an economic entity;

Disclose the content and key features of each stage;

Define a set of indicators for monitoring economic security.

Research Methods

The issues of monitoring and analysing economic activity of an enterprise are partially solved within the framework of building a management accounting or controlling system. The directions for using information from these systems at enterprises to ensure economic security are as follows:

Substantiate and adopt strategic and tactical management decisions;

Develop and implement industry-specific methods for analysing and assessing the potential of an enterprise, taking into account its industry-specific nature;

Develop and justify the changes in the organizational structure of an economic entity during reorganization processes (merging of individual organizations into groups, creation of holdings, vertically integrated structures),

Coordinate the relationship between the newly created and existing subsystems of the management structure;

Develop and implement a flexible management accounting system that contributes to the more efficient use and management of resources; Control over the compliance of price and quality of products, as well as the volume of its release;

Develop individual management accounting systems at an enterprise.

Survey, analysis, and expert assessments were used in determining the key stages of monitoring. In assessing the probability of threats that do not have quantitative assessment methods of simulation, methods of observation, comparisons, classical and statistical methods of probabilities of an event were used.

Findings

When monitoring threatening factors, the basic principle is the continuity of monitoring the state of the monitoring object.

Figure

Economic security of an enterprise, its independence and the prevention of transition to a critical risk zone can be ensured if the key strategic directions for ensuring business security are determined with a well-designed system of timely detection and elimination of threats, reducing the consequences of economic risks, as a result of effective use of information and analytical apparatus.

At the first stage, “identification of an economic entity”, the scope, goals and industry of an enterprise and key features of the external and internal environment are identified. As part of identification, a strategic analysis of the enterprise position in the market can be carried out using classical methods (SWOT analysis, PEST analysis, BCG matrix and others).

After identification of the monitoring object, a system of indicators is determined to assess the level of economic security and factors of its destabilization.

It is advisable to use a system of indicators that allow comprehensively monitoring the efficiency of an enterprise and indicators used in accounting, planning and analysis of an enterprise, which is a prerequisite for the practical application of such an assessment. It should be noted that the number of these indicators is required to be reduced to the necessary and sufficient value, making them grouped by the main activities of this enterprise.

Based on surveys of heads of financial services of 18 Russian enterprises, research by Russian scientists (Karzayeva & Babanskaya, 2016) and professional judgment, the use of a truncated set of indicators is recommended for express monitoring. These indicators are universal for the activities of most economic entities (Table

The selection of indicators is carried out in accordance with the results of identification of an economic entity, the main objectives and industry characteristics. Therefore, the presented list of indicators is open.

At the third stage of collecting, processing and preparing information about the monitoring object, an accounting and analytical base is formed for calculating indicators selected at the second stage. The following information is required:

Relevance of accounting and reporting information means its timeliness, value, usefulness for forecasting and assessing results.

Reliability of information is characterized by truthfulness, compliance with regulatory acts and intra-entity regulations; neutrality, i.e. the absence of “pressure” in it, pushing to make a decision, in which the user is not interested at all; possibility of verification and transparency; discretion - a reflection of costs and losses before income and profits (Steinbart, Raschke, Gal & Dilla, 2012a), (Steinbart, Raschke, Gal & Dilla, 2012b).

Comparability - the data should be accompanied by such comments and explanations concerning the meaning of the analysed indicators and the methodology for assessing them, which would preserve the possibility of their comparison (in time and space) and “reduction to a common denominator” in situations characterized by changes in the assessment methodology and adjustment of the analysed variables - is achieved in the process of conducting dynamic and structural analysis.

Rationality of economic information implies its sufficiency, efficiency, high utilization of primary information, the lack of unnecessary data, overcoming the contradiction between the systematic growth of the volume of information and its constant lack for rational management due to a high cost of obtaining (acquiring) the necessary information. An important criterion of rationality is not only reflecting, but also organizing the role of information, if it is adapted to the requirements of a particular user and can be recorded as know-how.

The next stage of monitoring is to identify the factors destabilizing economic security of an economic entity. The main factors of destabilization are presented in Table

Among the factors highlighted are features of the internal and external environment that do not have a quantitative assessment, in contrast to economic security indicators selected in the second stage of monitoring.

At the fifth stage - the formation of target indicators to protect the interests of an economic entity and permissible risk levels - the value of the indicator and the level of risk inherent in this value are determined. Table

The results of matching a risk category and probability of threats are presented in Table

After determining target values and acceptable risk levels, it is necessary to calculate monitoring indicators for a period of at least 5 years to effectively formulate conclusions and recommendations. This recommendation is mandatory during the initial monitoring to form a trend of indicators.

According to the results of calculations, a comprehensive assessment of economic security of an economic entity is carried out. The analysis is carried out in four main areas (groups) of indicators. The trend of change is determined. Negative trends and indicators, when it is impossible to formulate the stability of negative or positive changes, are identified. If necessary, a deep factor analysis of deviations of the indicator from the target value is carried out.

In addition to financial, economic, marketing and labour indicators of economic security, its level at an enterprise is characterized by violations of the law. Violations in the economic and financial sphere lead to the loss of economic security of an economic entity. Therefore, at the eighth stage of monitoring, an assessment of factors indicating a violation of the law at an enterprise takes place.

To reduce the risk of violations, economic entities are implementing a compliance control system.

A compliance system is a complex of internal control types embedded in the corporation’s business processes in the context of people, technical means and documents established to comply with external and internal standards and requirements.

This means that compliance control, as part of internal control, is one of the functions of corporate management. The “compliance” function has been introduced into Russian business by large foreign companies, which has not been legally defined, in contrast to the legally necessary and therefore well formed in economically developed countries where it is an integral part of activity.

Many domestic enterprises consider internal control and compliance to be not very important for successful business, so they don’t want to spend either time or finances on compliance control. At the same time, Western firms demonstrate in practice that competent compliance control can generate added value. The built-in control in the field of compliance is in turn - customer loyalty, interest and trust of shareholders, public trust in general. So, for the owners of a credit company, compliance control is a guarantee of reputation protection, since monitoring and control of risks to business reputation are usually assigned to compliance and are perceived in the international financial compliance sphere as a long-established compliance institution. When entering global capital markets, available compliance functions at an enterprise are viewed in a positive way by international regulators, investment financial organizations and institutional investors.

The compliance control structure consisting of highly qualified specialists creates an attractive perception of enterprise activities and its top management. The correct attitude of the management to compliance control creates conditions for the effective control of loss of profits, reduces the potential probability of deliberate or unintentional loss. Compliance control prevents loss of business reputation. Compliance control in structural divisions can be used as a consulting centre for internal compliance policy and the implementation of corporate compliance procedures. Such interaction with structural divisions ensures compliance control of potential risks at early stages, which simplifies their neutralization.

The final stage of monitoring is the development of recommendations based on its results. In the form of recommendations, measures can be formulated to strengthen economic security or to ensure the safety of the level already achieved.

Developed recommendations should guide managers not only to work on improving the values of short-term financial indicators in the current reporting period, but also to achieve long-term strategic goals and objectives. It is possible to trace the strategic goals and objectives that lie behind them at the stage of selecting indicators at stage 2 of monitoring.

In the process of functioning of the economic security mechanism, enterprises should determine not only the changes occurring in its state from the position of economic security in terms of “worse”, “better” and whether an enterprise left the dangerous economic state, where threats to its economic activity become systemic or, conversely, it has entered this state and how deep it is. For these purposes, it is necessary to know the boundaries between these states, i.e. know the threshold and target values of an indicator in the system of safety indicators. In the course of diagnostics of crisis situations at enterprises, it is necessary to identify future threats to economic security of an enterprise, the direction and nature of their actions in the process of strategic planning at the stage of analysing the current state and development forecast.

Conclusion

Monitoring of the level of economic security should be based on a system of indicators coordinating the relationship between analysis, building an information base, internal control and planning, ensuring the concentration of control actions on key factors of economic security of an enterprise, prompt identification of actual deviations of indicators from target and threshold ones and making appropriate management decisions aimed at normalizing indicators included in the system.

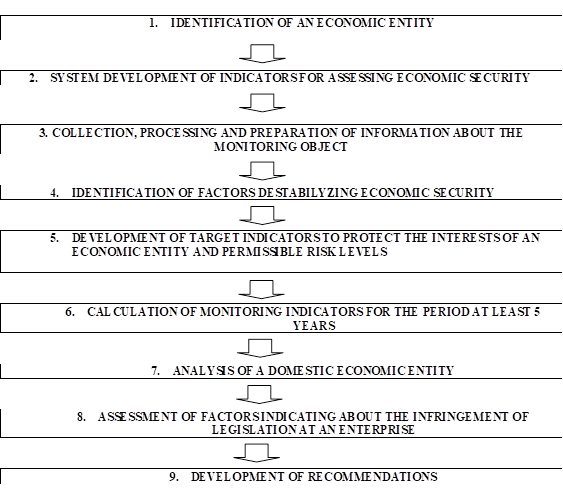

The methodology developed in the study to monitor, identify and analyse factors destabilizing economic security of an economic entity includes 9 steps:

1. Identification of an economic entity;

2. Development of a system of indicators for assessing the level of economic security;

3. Collection, processing and preparation of information about the object of monitoring;

4. Identification of factors destabilizing economic security;

5. Formation of target indicators to protect interests of an economic entity and permissible risk levels;

6. Calculation of monitoring indicators for a period of at least 5 years;

7. Analysis of economic security of an economic entity;

8. Assessment of factors indicating violation of the law at an enterprise;

9. Development of recommendations.

This methodology is recommended for implementation at industrial enterprises of the Russian Federation in order to create an economic security system that will reduce the level of threats to the business.

References

- Arbuzov, S. (2016). Features of the methodological and methodological support of economic security of the county at the present stage: dissertationю St. Petersburg, Russian Federation. Saint Petersburg state university of economics.

- Busan, B., Wæver, O., & Wilde, J. (1998). A New Framework for Analysis. London. GB. Lynne Rienner.

- Cook, W. (2016). Inside environmental auditing: Current. Environmental, Environmental & Environmental, 18, 33-39.

- Gaponenko, V., Bespalko, L., & Vlaskov, A. (2007). Economic security of enterprises. Approaches and principles. Novy Urengoy. Russian Federation, 89. 107-108.

- Glumov, A., & Kiselitsa P. (2013). Formation of economic security of an enterprise. Academic Bulletin, 4 (26), 85-90.

- Janioglo, A. (2017). Complex system of ensuring economic security of enterprises (using the example of the ATU Gagauzia) (Doctoral dissertation). Chisinau, Republica Moldova: Moldova State University.

- Jerry, C., & Ramesh, J. (1989). Managers’ earnings and intra-industry information transfers. Journal of Accounting and Economics. Elsevier, 11(1). 3-33.

- Karzayeva, N., & Babanskaya, A. (2016). Economic security: a textbook. Moscow, Russian Federation: RGAU-ICHA.

- Messier W. (2014). An approach to learning risk-based auditing. Journal of Accounting Education, 32, 276 – 287.

- Presidential Decree on the Economic Security Strategy of the Russian Federation for the Period until 2030 (2017). No. 208. Collected legislation of the Russian Federation. 20. 1976-1984.

- Steinbart, P., Raschke, R., Gal, G., & Dilla, W. (2012a). There is a relationship between the decisions and accounting organizations. International Journal of Accounting Information Systems, Elsevier, 25, 10-11.

- Steinbart, P., Raschke, R., Gal, G., & Dilla, W. (2012b). Factors influencing the relationship between internal audit and information security: An exploratory investigation, International Journal of Accounting Information Systems, Elsevier, 26, 228-243.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

20 March 2019

Article Doi

eBook ISBN

978-1-80296-056-3

Publisher

Future Academy

Volume

57

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1887

Subjects

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Manyaeva, V., Naumova, O., & Sotskova, S. (2019). Development Of Methods For Monitoring Economic Security Of An Economic Entity. In V. Mantulenko (Ed.), Global Challenges and Prospects of the Modern Economic Development, vol 57. European Proceedings of Social and Behavioural Sciences (pp. 1158-1168). Future Academy. https://doi.org/10.15405/epsbs.2019.03.117