Factors Influencing Whistleblowing Intention Among Accountants In Malaysia

Abstract

The accounting field and profession have emphasis the demand for professional accountant to build and develop ethical attitudes early in their career, even before they enter the profession which the accounting profession is closely related with whistleblowing element. To understand the factors that influences an accountant for decision to whistle blow is very crucial for both management and organisations. This study is to investigate the factors that influence an accountants’ intention to whistleblowing in Malaysia. This study narrowed the factors into several categories which are organisational factors (organisation size and job level), individual factors (locus of control) and situational factors (seriousness of wrongdoings). A total of 157 accountants had participate in an experimental design adopting four vignettes constituting four different types of wrongdoing. The result indicate that, different kind of unethical behavior reflect different level of intention to whistleblowing. The job level, locus of control and seriousness of wrongdoing were found to be significant factors that were be able to influence accountants’ intention to whistleblowing.

Keywords: Whistleblowingprosocial behaviour theory

Introduction

Whistleblower plays a significant role to expose any fraud, mismanagement, corruption, or any other wrongdoings made by the company or management. It is very important especially in the cases that threaten public health and safety, environment, financial integrity and human rights. However, not everyone are having the courage to become a whistleblower as it is like putting themselves to risk. This is because, to become a whistleblower, it may cause that whistleblower to be fired, blacklisted, arrested, sued, or when worse become to worst it can lead to assault or homicide. Therefore, the act or policy regarding whistleblowing on the corporate wrongdoings is needed (Eaton & Akers, 2007).

The researchers had come out with many theories and opinions that can be related to whistleblowing. One of the opinions from the previous study states that, “hot” cognitions play important role in decision making on whistleblowing and it is vital for managers to understand that emotions were most influential on whistleblowing decisions only after internal attempts to halt the activities that had failed (Henik, 2008). In a psychology view, the decision to blow the whistle is not an easy one and it is quite difficult (Miceli & Near, 1984). In May 2010, the Malaysian Parliament had passed the Whistleblower Protection Act 2010 effective on December 2010. According to National Key Result Area (NKRA), the act is a law of Malaysia to beat and combat the corruption and other wrongdoings by encouraging and facilitating disclosures of improper conduct in the public and private sector, to protect persons making those disclosures from detrimental action, to provide for the matter disclosed to be investigated and dealt with and to provide for the remedies connected therewith.

Even though there are several studies have been conducted regarding the factor encouraging and influence to be a whistle blower, but it needs to be continuously conducted the research extensively to get understanding on certain particular questions about whistleblowing especially in Malaysia. Therefore, to understand the factors that influences an accountant for decision to whistle blow is very crucial for both management and organisations.

Prosocial behaviour theory.

The theory of procosial behaviour approach of whistleblowing is based on the bystander intervention theory. This study is based on the study by Latane and Darley (1968). Many previous literature on whistleblowing are using this theory (see Ahmad, 2011; Brennan & Kelly, 2007; Dozier & Miceli, 1995). The bystander intervention theory can be used in determine the decision process. Latane and Darley (1968) had illustrated five steps of the decision process for whistleblowing behavior. Firstly, the observer has to be aware of the event. Next, the observer also needs to decide that the event is an emergency event. Third, the observer must decide whether he or she is responsible for helping. After that, choose the appropriate method to help and finally is the observer implements the intervention which is the action is undertaken (Brennan & Kelly, 2007). The other theories related to whistleblowing intention are the organizational theory (Kaplan & Shultz, 2007) and a study on the reciprocal influence of whistleblower and co-workers (Greenberger, Miceli, & Cohen, 1987).

Factors influencing whistleblowing intention.

Size of organisation:

Prosocial behaviour theory suggests that intention to whistleblowing in smaller organisations would be higher than larger organisations due to the diffusion of responsibility. The employee in the large firm would less likely to whistleblowing. Two previous studies (Dennis & Blaire, 2008; Nadzri, Jeremy, & Robert, 2011) shared the same perception that in line with bystander theory which stated that the employee in small firm would feel more responsible and concerned with the wellbeing of the company (Miceli & Near, 1984; Keenan, 2000). Hence, the following hypothesis is proposed:

H1: There is a significant relationship between size of organizations and intention to whistleblow;

Job levels:

Individuals who held higher position are tend to do more whistleblowing compared with employees at lower levels due to the role prescriptions of supervisors (Rothwell & Baldwin, 2007 and Miceli, Near & Dozier,1991). On the study conducted by Keenan (2002) also stated that different level of position will have different tendency in whistleblowing which is the upper-levels managers are more likely to whistleblow compared to the middle-level and lower-level. In term of the research on power, which is the minority influence literature, Greenberger et al. (1987) mentioned that, the individual who in higher position will have a greater influence and able to prevent organizational wrongdoing. Therefore, the study expects that high job level will increase the intention to blow the whistle which lead to the following hypothesis:

H2: Accountants holding higher managerial positions have high whistleblowing intention than those in lower managerial positions.

Locus of control:

According to Curtis & Taylor (2009) and Chiu (2003), the personal characteristics of locus of control are a vital antecedent of the possibility to blow the whistle. To be a whistle-blower is consider as a good manner, which is influenced by internal locus of control. Curtis and Taylor (2009) also support that the person who possess internal locus of control is more likely to involve in whistleblowing behavior. Therefore, this study proposes the following hypothesis:

H3: Accountants with internal locus of control will be more likely to whistleblow.

Seriousness of wrongdoing:

The study conducted by Miceli et al. (1991) indicates that each members in organization will act differently based on different types of wrongdoing. In Ayers and Kaplan's (2005) study, the seriousness of wrongdoings are closely related to the individual intention to report the wrongdoing and be a whistleblower (Ayers & Kaplan, 2005). The finding also consistence with Ahmad (2011) research that using internal auditors as the sample. Both of this previous studies using a similar experimental approach "vignettes". This study will use similar experimental approach and expects that accountants will demonstrate similar behavior.

H4: Accountants tend to have high intention of whistleblowing when seriousness level is higher.

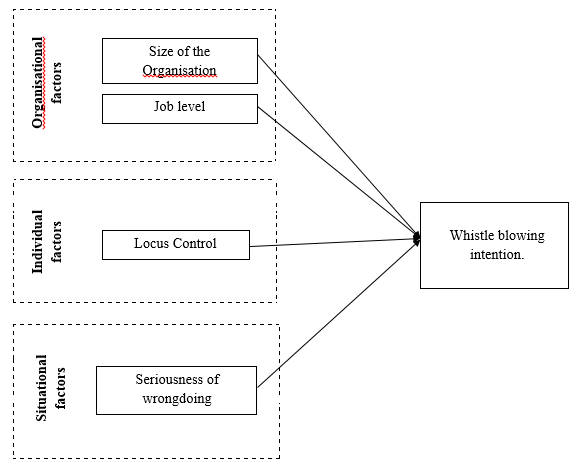

Research framework.

Figure

Problem Statement

The whistleblower intention not only depends on specific factor, the decisions are dependent on complex psychological and sociological factors which indicate that no two individual whistleblowers are alike (Gobert & Punch, 2000). The accountants themselves might have no intention or vice versa to be a whistleblower due to factor that might influence them such as organizational, individual, situation, and demographic factors. Therefore, studies of these four factors on the accountant’s whistleblowing intention need to be conducted. Malaysia is still having a limited literature and discussion on the issue arise regarding the whistleblowing activities in organization. Previous studies of whistleblowing in Malaysia (Patel, 2003; Ahmad, 2011) only examined auditors as subjects. To achieve the objective of whistleblowing policies in the organization, it is important for the management to understand the factors that might be a catalyst to increase the intention of accountant to be a whistleblower in Malaysia. Without any intention to blow the whistle, the organization might face difficulties especially when the case is material to the organization.

Research Questions

The following are the research questions for this study:

What are the factors that influence the accountants to whistleblowing?

Purpose of the Study

The purpose of this research study is to examine the factors that influence whistle blowing intention among accountants in Malaysia. There are four main research objectives to be addressed in this study:

To study the factors those influence the accountants to blow the whistle. The factors that will be included in our research study are:

Organisational factors: size of organisation and job level influence intention among accountants in Malaysia to whistleblowing in their own organization.

Individual factors: locus control and intention of accountant’s to whistleblowing.

Situational factors: seriousness of wrongdoing and intention among accountants in Malaysia to whistleblowing in their organisation.

Research Methods

Sample selection.

The convenience sampling process is run by selecting a sufficient number of element from the population then the result obtain will be concluded to present a whole population actual result. The final sample of this study is 157 samples which were distributed to accountants in Malaysia and also from various type of organization to reflect our investigation which is the factor lead to the intention of whistleblower.

Measurement of dependent variable.

The measurement for whistleblowing intention is by using vignettes (Ahmad, 2011) and it will use two character. First character will be the first person which is the individual who engage with whistleblowing, while the other character is the individual who would take the action. The respondent will be given four vignettes which is different situation to determine the likelihood of their engagement in whistleblowing. The scale will be used is five-point likert scale, which will be defined as 1 = “Less likely” to 5 = “Very likely”. These are similar to ones used by Ahmad (2011) and Kaplan et al. (2007).

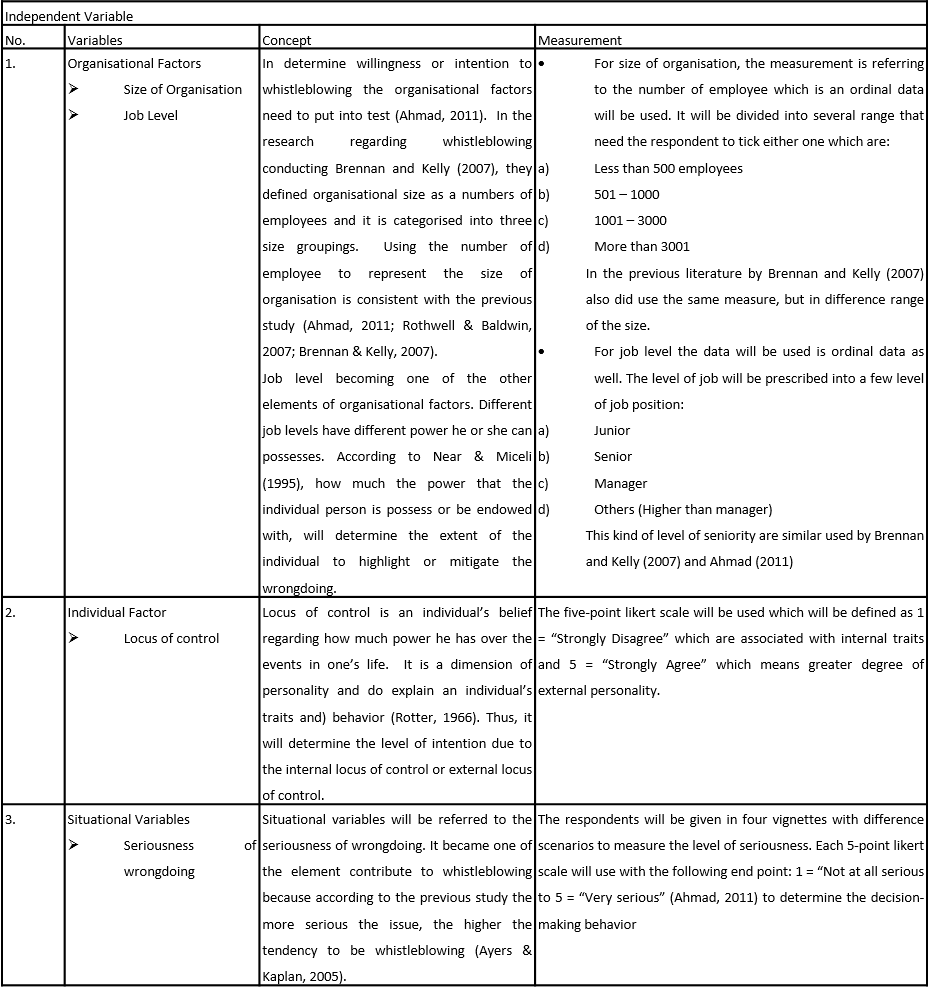

Measurement of independent variable.

Findings

Descriptive result.

Majority of the respondents are working with the current organization less than 2 years (29.9%). As the tenure increased, the percentage of the respondent decreased. For tenure of 2 to 5 years, the percentage was 26.8% and followed by 6 to 10 years 26.1% and lastly 17.2% for 11 years or more. The job level of the respondents was categorized to junior executive, senior executive, manager and other. Most of the respondents are holding junior executive position in their organization. The percentage was 54.1%, which is more than half of the respondents. Many of the respondents worked in small organizations that consist of 1 to 500 employees which is 41.4%. As the size increased, the percentage was decreased. Only 30.6% from 501 to 1000 employees, 16.6% from 1001 to 3000 employees and 11.5% of respondents from more than 3000 employees organizations (Table

Reliability analysis.

The range value of reliability is from 0 to 1. Based on the table, we can see that all variables obtain reliability coefficients of more than 0.80 by using the Cronbach's Alpha method. The value of above 0.8 for all this variable is considered good for the all item in the variables. In other words, this shows that the items in the scale are suitable to be used in this study.

Test of difference/significance.

The Kruskal-Wallis test found out that, only in vignettes 3 was a significant difference within the firm size in whistleblowing intention with p=0.04. The firm size of ‘1-500 employees’ recorded a highest mean rank score than the other group of firm size which indicates that the smaller firms are more influence the accountants’ intention to whistleblow. However, as only 1 out of 4 is came out with a significant difference, it will be consider that the firm size are not becoming a vital factor in influencing the accountant to whistleblow. Thus, the hypothesis is not accepted. This finding was contradict with study by Brennan and Kelly (2007) which found that firm size able to influence the intention of whistleblowing.

The Kruskal-wallis test also showed that there are significant difference in vignettes 1 and 3. Vignettes 3 strongest significance difference as the p value is below 0.05. Whereas the other vignettes showed that, the p values were higher than 0.1. In vignettes 1 and 3, the ‘others’ position which exclude junior executives, senior executives and manager give higher mean rank score. Therefore, even though it is significant our suggested hypothesis is not accepted. This findings is different with previous literature by Ahmad, 2011; Keenan, 2002) where in their research found that those in higher than manager is more tendency in whistleblowing. It may be due to the higher management alert and acknowledge the responsibility given to them that encourage them to whistleblowing than lower management.

Correlation analysis.

Based on the correlation result by Spearman rho test, the hypothesis 3 is partially accepted. By possessing external traits, only for vignettes 1 & 2 show significant relationship between locus of control and whistleblowing intention. Whereas, vignettes 4 and vignettes 5 are not significant. Therefore, it can be conclude that the hypothesis of locus of control in determining the accountant’s intention is partially accepted. The result is similar with the previous literature by Chiu (2003) and Miceli et al. (1991) found that there is a relationship between locus of control with the intention to whistleblow, due to the condition of threat of retaliation. It shows that when the individuals are having a control over their life and able to make their own decision, the tendency to whistleblowing will increase.

Spearman rho correlation coefficient test shows that vignettes 2, 3 & 4 are having significant influence on the accountants’ intention to whistleblowing as the result shows positive significant correlation at level 0.05. However, for vignettes 1 are having no significant relationship. Thus, our hypothesis proposed that seriousness of wrongdoing having significant influence over the attention to whistleblowing is accepted. When an accountant are facing or found the wrongdoings that have a high impact to the user, they tend whistleblowing. This shows that this finding is consistent with the several studies. The study by Ahmad (2011), he found that the seriousness of wrongdoing is giving a significant influence on the intention to whistleblowing. Contradict with the study by Brennan and Kelly (2007), they found that the situational factors are not significantly influence the intention to whistleblowing.

Conclusion

Based on the findings, only locus of control and seriousness of wrongdoing is accepted. Whereas, the others are contradicted with the hypothesis. This study shows that when the individuals are having a control over their life and able to make their own decision, the tendency to whistleblowing will increase and when an accountant are facing or found the wrongdoings that have a high impact to the user, they tend whistleblowing. In term of size of organization, this study found that size of organization is not significantly influence the intention to whistleblowing. Only vignettes 1 gave significant differences. Therefore, hypothesis 1 is not accepted. The size of organization is not the factors to trigger the accountants’ intention to blow the whistle.

Hypothesis 2 on job level is also not accepted. This study previously proposed that the higher managerial position will be more likely to whistleblowing. However, this study found that the ‘others’ position are more potential in whistleblowing. The ‘others’ here refer to the others position exclude junior executives, senior executives and manager. It does not specifically refer to higher than manager only as it can be the position which is lower than junior executives. However, in term of triggering the intention, job level is partially able to influence the intention in whistleblowing due to significant result in vignettes 1 and 3.

References

- Ahmad, S. A. (2011). Internal auditors and internal whistleblowing intentions: A study of organisational, individual, situational and demographic factors. Doctor of Philosophy Thesis, Edith Cowan University Western Australia.

- Ayers, S., & Kaplan, S. E. (2005). Wrongdoing by consultants: An examination of employees' reporting intentions. Journal of Business Ethics, 57(2), 121-137.

- Brennan, N., & Kelly, J. (2007). A study of whistleblowing among trainee auditors. The British Accounting Review, 39(1), 61-87.

- Chiu, R. K. (2003). Ethical judgment and whistleblowing intention: Examining the moderating role of locus of control. Journal of Business Ethics, 43(1/2), 65-74.

- Curtis, M. B., & Taylor, E. Z. (2009). Whistleblowing in public accounting: Influence of identity disclosure, situational context, and personal characteristics. Accounting and the Public Interest, 9, 191-220.

- Dennis, H., & Blair, S. (2008). Confusion culture and whistle-blowing by professional accountants: An exploratory study. Managerial Auditing Journal, 23, 504 – 526.

- Dozier, J. B., & Miceli, M. P. (1985). Potential predictors of whistle-blowing: A prosocial behavior perspective. Academy of Management Review, 10(4), 823-836.

- Eaton, T. V., & Akers, M. D. (2007). Whistleblowing and good governance. The CPA Journal, 77(6), 66-71.

- Gobert, J., & Punch, M. (2000). Whistleblowers, the public interest, and the Public Interest Disclosure Act 1998. The Modern Law Review, 63(1), 25-54.

- Greenberger, D. B., Miceli, M. P., & Cohen, D. J. (1987). Oppositionists and group norms: The reciprocal influence of whistle-blowers and co-workers. Journal of Business Ethics, 6(7), 527-542.

- Henik, E., G. (2008). Mad as hell or scared stiff? The effects of value conflict and emotions on potential whistle-blowers. Doctor of Philosophy Thesis, University of California, Berkeley.

- Kaplan, S. E., & Schultz, J. J. (2007). Intentions to report questionable acts: an examination of the influence of anonymous reporting channel, internal audit quality, and setting. Journal of Business Ethics, 71(2), 109-124.

- Keenan, J. P. (2000). Blowing the whistle on less serious forms of fraud: A study of executives and managers. Employee Responsibilities and Rights Journal, 12(4), 85-94.

- Keenan, J. P. (2002). Whistleblowing: A study of managerial differences. Employee Responsibilities and Rights Journal, 14(1), 17-32.

- Latane, B., & Darley, J. M. (1968). Group inhibition of bystander intervention in emergencies. Journal of Personality and Social Psychology, 10(3), 215-221.

- Miceli, M. P., & Near, J. P. (1984). The relationships among beliefs, organizational position, and whistle-blowing status: A discriminant analysis. Academy of Management Journal, 27(4), 687-705.

- Miceli, M. P., Near, J. P., & Dozier, J. B. (1991). Blowing the whistle on data fudging: A controlled field experiment. Journal of Applied Social Psychology, 21(4), 271-295.

- Nadzri, A.G., Jeremy, G. & Robert, E. (2011). Predicting whistleblowing intention among supervisor in Malaysia. Journal of Global Management, 3(1), 44-45.

- Patel, C. (2003). Some cross-cultural evidence on whistle-blowing as an internal control mechanism. Journal of International Accounting Research, 2, 69-96.

- Rothwell, G. R., & Baldwin, J. N. (2007). Whistle-blowing and the Code of Silence in police agencies. Crime and Delinquency, 53(4), 605-632.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

31 July 2018

Article Doi

eBook ISBN

978-1-80296-043-3

Publisher

Future Academy

Volume

44

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-989

Subjects

Business, innovation, sustainability, environment, green business, environmental issues, industry, industrial studies

Cite this article as:

Zainol, Z., Zollkefli, A. Q., Nasir, A. N., Zakaria, F. M., & Kamaruzaman, N. Z. (2018). Factors Influencing Whistleblowing Intention Among Accountants In Malaysia. In N. Nadiah Ahmad, N. Raida Abd Rahman, E. Esa, F. Hanim Abdul Rauf, & W. Farhah (Eds.), Interdisciplinary Sustainability Perspectives: Engaging Enviromental, Cultural, Economic and Social Concerns, vol 44. European Proceedings of Social and Behavioural Sciences (pp. 79-88). Future Academy. https://doi.org/10.15405/epsbs.2018.07.02.9