Balanced Scorecard For Future Sustainability Of Malaysian Higher Education Institutions

Abstract

The purpose of this study is to examine the relationship between Balanced Scorecard Initiatives and Organizational Climate with regard to the Sustainability of Malaysian Higher Education Institutions. A sample of 272 top administrators from eight selected public universities in Peninsular Malaysia was determined based on purposive sampling technique. A full-fledged Structural Equation Modeling computer software, Analysis of Moment Structures version 20.0 was used as statistical analysis technique in examining the psychometric properties, testing the hypotheses of the study. Using a comprehensive Balanced Scorecard theory this paper argues that Balanced Scorecard Initiatives provide a systemic strategy for the achievement of future sustainability of Malaysian higher education institutions. The findings revealed that Organizational Climate has no relationship with Sustainability of Malaysian Higher Education Institutions and therefore consistent with previous literature due to communication challenges and decision-making in higher education institutions that needs further attention among the selected eight higher education institutions in Malaysia. This study provides a basis for the future study but unfortunately the result cannot be generalized for the whole of Malaysia due to the study is limited to peninsular Malaysia only. The framework presented in this study can be used as a basis for the development of general framework of the Balanced Scorecard, Organizational Climate and the Sustainability of Higher Education Institutions perspectives. This paper indicates the important findings on the Balanced Scorecard Initiatives and considered as first kind of research on the future sustainability of Malaysian higher education institutions.

Keywords: Balanced ScorecardSustainabilityHigher Education Institution

Introduction

The background of the study and the balanced scorecard initiative together with the future sustainability of higher education institutions are discussed below.

Background

Prominent strategies such as strategic planning (SP), quality assurance (QA), total quality management (TQM), Balanced Scorecard (BSC) and others might be executed ideally and timely in uplifting the institutions of higher learning. Lee et al. (2000) described BSC in particular as an organizational holistic performance management tool which is geared towards defining performance measures, communicating objectives and vision to the organization. Besides that, Hladchenko (2015), Allen et al., (2010) claim that BSC initiative is a key driving performance in organizations. As the co-founders of BSC, Kaplan and Norton (1996b) emphasized that BSC provides the management with the instrumentation they need to navigate for future competitive success in both corporate sectors and educational institutions. In supporting this, BSC is able to address effectively the serious deficiencies in old-fashioned management system such as managed to create a meaningful linkage between long term strategic planning with short term strategic action plans that merit urgent attention for sustainability of higher education institution sectors (Perkins, Grey & Remmers, 2014; Anisha, 2012).

The vibrant vision of becoming Asia higher education hub, the Malaysian public universities need to be more dynamic and highly responsive to quality performance needs to be applicable in order to fulfil the agenda of becoming a developed country. In general, public universities in Malaysia were provided with adequate financial resources by the Ministry of Higher Education (MOHE) to upgrade their quality performance and strategies to the extent of meeting the global quality education demand worldwide. The issue is the lump sum of funding as budget allocation meant for developmental capital expenditures was available to contribute certain impact towards the sustainability of higher education without prejudice. Although, it is noted that MOHE preserves the respective universities in their decision-making processes and strategic direction endeavors, however the sustainability performance and improvement are indeed required to be evaluated (Kahirolmohdsalleh & Nor Lisa, 2012).

Nevertheless, BSC initiative perceived as a performance measurement system that focuses on four related perspectives of

Balanced Scorecard Initiative and Sustainability of Higher Education Institutions

The future sustainability of higher education institutions (HEI) is the most crucial responsibility to the top administrators. The aim of the future institutions is to achieve quality and quality performance with respect to organizational climate effort through a developed strategic vision on how to appear in the presence of the customers and stakeholders (

Furthermore, evidence have revealed successful operation and implementation of BSC at the Royal Canadian Mounted Police (RCMP) in Canada, also at the Economic Development Administration (EDA) in USA (Chan, 2004) while, further extended at the United Kingdom Ministry of Defence (MoD) thus, tested successful in Finland higher education institutions and Othman, (2006) stress that implementations of BSC in Malaysia have experienced lower level of implementation than many countries consistence implemented. According to Nur Anisah (2012) the introduction of BSC indicators aims to facilitate leadership performance in HEIs to move strategically and to develop the ability to relate major decisions to the bigger picture of how future can be achieved.

It was noted that management were too busy and lacking high developmental information about how to implement the BSC paradigm for the achievement of initiative goal (Chan, 2004). However, the significant of implementing balanced scorecard for quality performance was recognized by Gonçalves (2009) who proposed that strategic model of planning aligned with balanced scorecard through the strategic ability of organizational climate. Similarly, BSC has been tested based on critical four perspectives aligned with the Malcolm Baldrige National Quality Award (MBNQA) in education criteria for performance and excellence in USA for promoting quality management in educational sector (Lee et al., 2000).

Fundamentally, Balanced Scorecard Initiative (BSCI) was mounted on specific objectives which are crucial that permitted establishing performance indicators in becoming an evaluating tool that are employing worldwide in corporate and educational institutions (Othman, 2006; Kaplan & Norton, 2004; Hronec, 1994). As a matter of fact in education the intangible aspects are converted to tangible initiative. The main problems of using the balanced scorecard is a way to measure the performance and its initiatives towards achievement of quality performance that developed by the top administrators in HEI. Improving effectively as being the importance of using BSCI, meanwhile effectiveness and efficiency of management in HEIs is to clarify and gain consensus about strategy: (1) on how to communicate quality as major part of future performances throughout the organization, (2) align departmental and personal goals to the strategy, (3) by linking the strategic objectives to long-term targets and annual budgets, (4) identify and align strategic initiatives, (5) perform periodic and systematic strategic reviews, and (6) Obtain feedback to learn about and to improve strategy (Lasisi, 2016; Allen, et al., 2010; Chen et al., 2006; Kaplan & Norton 2004).

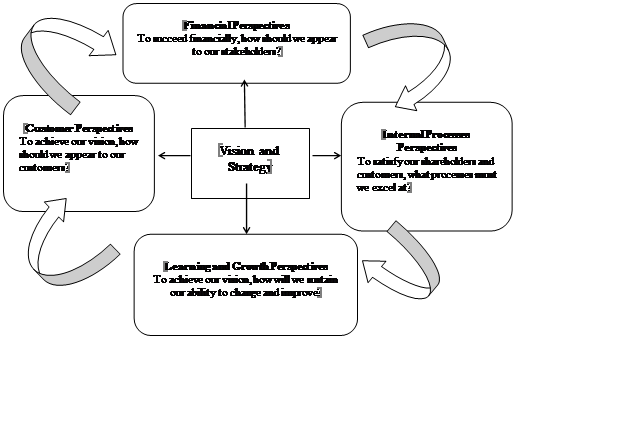

To evaluate the performance in HEI, it required Kaplan and Norton’s initiative theory that being used widely in various higher educational institutions in developing and developed countries. This theory leads the present study by applying strategies from corporate and business organizations in achieving better futures in HEI. This is because achieving quality is persisting in educational sector as seen in corporate organizations. Kaplan and Norton (2004) built on strategy of how we can achieve the future for long term rather than short term planning achievement. Nevertheless, BSCI has had tremendous impact on management at various levels to develop balanced indicators of performance in HEI. Meanwhile, original Balanced Scorecard identified four perspectives which are the financial perspective (F); the customer perspective (CU); the internal-process perspective (IP); and the learning and growth perspective (LG) (Figure

Problem Statement

Waheed et al., (2011:359) established that “when quality improves sustainability increases”. Meanwhile, Moore (2005) realized that there is a gap about universities obligation on sustainability and to become, continues as a leader in accommodating global quality education demand. It is important to envision what a sustainable university might look like through organizational climate activities such as orientation, communication, supervision, decision-making, and reward-management (Jeswani & Dave, 2012; Wright 2010). This is because engagement of the administrators, staff, faculty and students shall ensure long-time achievement in HEI (Kurland, 2011; Filho, 2005). Sustainability is a collective effort of the people concerned in HEI, thus required strategy of moving towards a sustainable future.

The university has a task and responsibility in creating a sustainable future and should have common understanding about sustainability concept. Emanuel and Adams (2010) conceptualized the word sustainability as continuous development and for development activities now and indefinite future in HEI. It also defined as meeting the needs of the present generation without compromising the ability of the future generations to meet their needs (Brundtland, 1987). Universities’ customers as one of the future generation might meet their needs by implementing certain tools. It can be observed that initiating balanced scorecard has its relationship with sustainability that enhancing in measures the four perspectives performance in HEI.

Literaures have provided that universities should make sustainability issues a top priority, encouraging critical thinking about sustainability issues, creating partnership with government and non-governmental agent for sustainability issues and consults students on their opinions on sustainability issues in HEIs. Lasisi and Hairuddin (2015) create SHEI model based on:

Sustaining the future of HEI requires the effort of the management because change is the responsibility of administrators for SHEI (Wright, 2010; Moore 2005; Waheed et al., 2011:359). The related issues and problem building a gap within this study is attention failure towards quality performance among the administrators even though autonomy was given to HEI leaders by the MOHE (Morshidi, 2010). Organizational climate requires to be assessed based on five factors in this study as already employed by previous researchers (Peña-Suárez, 2013; Jeswani & Dave, 2012; Pace & Stern, 1958; Halpin & Croft, 1963). Conceptualizing organizational climate is a set of characteristics that distinguish one organization from another which are relatively enduring over time, and influence the behavior of the people in the organization. In short, organizational climate is a concept that deals with organizational members’ perceptions of their working environment.

The existing literature on organizational climate was determined by James and Jones (1974). The researchers reviewed all related researches, the definitions, conceptual frameworks, and measurement approaches and divided them into three principal categories. According to the researchers, their findings show that the majority of the studies were based on theoretical aspect of organizational climate. Similarly, Halpin and Croft (1963) measured organizational climate of public school employees’ perceptions through dimensions comprising of intimacy on how members enjoy social relationships in an organization. Aloofness as another dimension measured the perception of how formal and impersonal management behavior is in an organizational climate. In addition, hindrance was measured in terms of perception of how employees feel that they are burdened by routine duties. Finally, organizational climate’s closeness and constant supervision among supervisors on the subordinate staff in organization was also measured.

Jeswani and Dave (2012) tried to study the impacts of organizational climate on turnover intention. The study was measured by a 23-item instrument distributed among faculty members of a technical institution in India. This organizational climate instrument was dimensionally categorized into 5 factors of

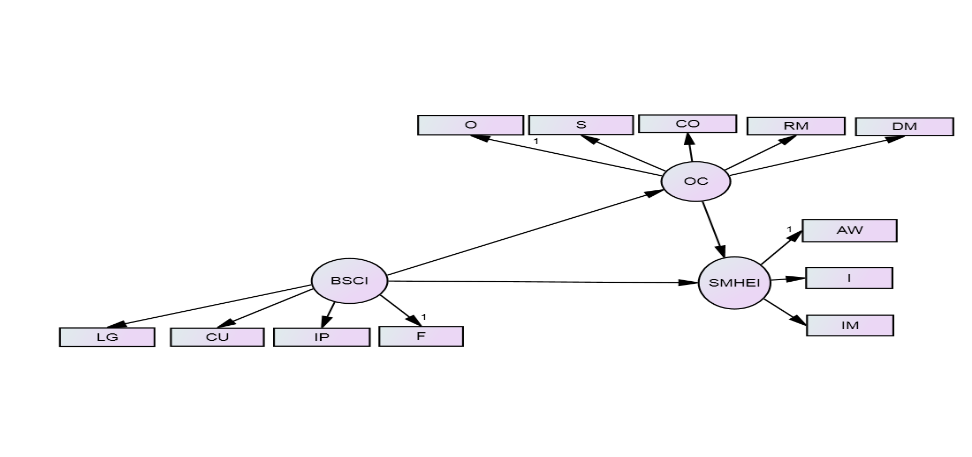

Due to the statement of the problem as discussed above, this study assumed that BSCI and OC has a significant direct and indirect relationship with SMHEI. Therefore, the proposed general conceptual framework of the study has three constructs particularly BSCI, OC, and SMHEI in order to establish the relationship for the improvement of Malaysian HEIs. The proposed general conceptual framework of the study is exhibited by Figure

Research Questions

Based on the general conceptual framework of the study (Figure

Does BSCI has direct and significant relationship with SMHEI?

Does BSCI has direct and significant relationship with OC in the context of MHEI?

Does BSCI has indirect significant relationship with SMHEI through OC?

Does the hypothesized model of the study is valid and fit the data well?

Purpose of the Study

As depicted and illustrated by Figure

Research Methods

The methods are briefly discussed below.

Research design, sampling and data collection

This quantitative study had conducted a survey for collection data. The selection of top administrators at eight selected universities was made through a purposive sampling of procedure which is based on position and experience: Deans, Deputy Deans, Directors, Deputy Directors, Assistant Directors, and HODs within Malaysian such as Universiti Malaya (UM), Universiti Sains Malaysia (USM), Universiti Putra Malaysia (UPM), Universiti Kebangsaan Malaysia (UKM), Universiti Teknologi Malaysia (UTM), Universiti Utara Malaysia (UUM), International Islamic University Malaysia (IIUM), and Universiti Teknologi MARA (UiTM). Questionnaires were distributed based on permission from each faculty and human resource offices by showing the introduction letter of the researcher’s university.

Respondents and Instrumentation

The research instrument using seven (7) summative or Likert scales was pilot tested before it was distributed to the actual respondents. The results of the pilot test showed that all instruments are valid and achieved acceptable reliability index (α=0.75 to 0.98). Then, the survey instrument was distributed to actual respondents comprised 277 top administrators for the main research on initiating balanced scorecard for sustainability of HEI. After testing the assumptions of outliers and missing data, the total usable returned questionnaires in the study were 263 which are adequate for Structural Equation Modeling (SEM) statistical techniques for further analysis (Hair, et al., 2010).

Demographic information revealed that the sample comprised 131 males (49.8 per cent) and 132 females (50.2 per cent). Based on position, 32 Deans (12.2 per cent), Deputy Deans were 66 (25.1 per cent), Directors were 15 (5.7 per cent), Deputy Directors also were 12 (4.6 per cent), and Assistant Directors 54 (20.5 per cent) and Head of Departments were 84 (31.9 per cent). The breakdown in term of experience, majority (166 or 63.1 per cent) was 1-5 year experience in HEI administration. Meanwhile, some (31, or 11.8 per cent) was less than one year, another (35, or 13.3 per cent) was 6-10 year of experience, and others (31, or 11.8 per cent) were eleven (11) years above. Nevertheless, the respondents have shown long term experience in administration of HEI in Malaysia.

Findings

We tested the proposed research hypothesized model using the SEM. In this study, a confirmatory factor analysis (CFA) was applied to validate the measurement model according to dimensional variable of each construct, and the structural model was estimated based on full-fledge model (Hair et al., 2010). We used AMOS 20.0 computer program with the maximum likelihood method of estimation in measuring the strength of relationships and model suitability.

Testing the measurement models

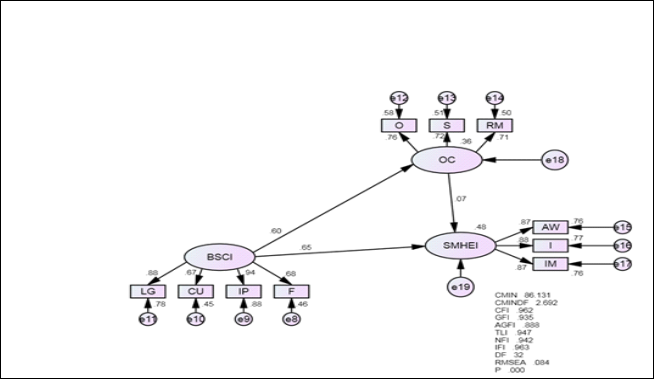

For the purpose of addressing the objectives of the study, the measurement model was tested through the application of CFA on each construct of BSCI, OC, and SMHEI. The results illustrated in Table

In this study, the fit indices were utilized to assess the overall fit of the measurement model. However, all the factors of BSCI and SMHEI were sufficiently followed the trend of variable dimensionality (4 factors for BSCI and 3 factors for SMHEI) while, OC was not fit if based on five (5) factors according to the theory. Modification indices (MI) suggested that by removing the communication and decision making factors were not strong enough for modification.

Based on recommended criteria: χ2, p > 0.05; the ratio of χ2 to its degree of freedom (χ2/df) < 3.0; goodness of fit index (GFI) > 0.9; root mean square error of approximation (RMSEA) < 0.08; and incremental fit index (IFI) > 0.9 (Hair et al., 2010), the result revealed that only

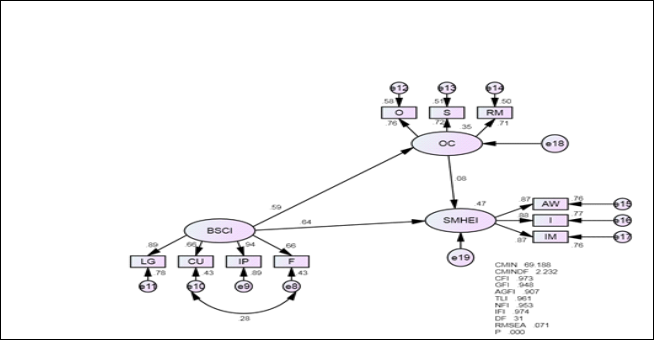

The study employed SEM technique for estimating the relationships between BSCI, OC and SMHEI. Prior to testing of the hypotheses, the recommended criteria of fit statistics were checked (Figure

The better fit indices were achieved while the MI suggested moderate correlation between customer and financial perspectives of BSCI (Figure

Testing of the hypotheses.

The study also attempted to seek more information about direct and indirect relationships among the variables employed in the study by testing the following hypotheses:

H1: BSCI has direct relationship with SMHEI

Hypothesis (H1) trying to prove that BSCI in Malaysian HEI has direct relationship on the SMHEI. It is trying to expatiate that if there is improve in BSCI perspectives there will be increases in SMHEI. According to Figure

H2: BSCI has direct relationship with OC in MHEI

Hypothesis (H2) is trying to prove that BSCI in Malaysian HEI has direct relationship with OC. This indicated that administrators fully understand the complexity of BSCI and its indicators but adopting in MHEI not exists on the SMHEI. According to Figure

H3: BSCI has significant indirect effect through OC of MHEI on the SMHEI

Hypothesis (H3) is trying to prove that BSCI in Malaysian HEI has significant indirect effect on SMHEI through OC of Malaysian HEI. According to Figure

H4: Hypothesized model fits the data well

Hypothesis (H4) is demonstrating that all constructs (BSCI, OC, and SMHEI) in full-fledge SEM are valid and fit the data well. As usual, based on Figure

Conclusion

BSCI has direct relationship on the SMHEI. It is trying to expatiate that if there is more attention given to effectiveness and efficient uses of BSCI there will be a tendency in SMHEI improvement (Waheed, 2011). Previous researches have been stressed on Malaysian HEI customers and its efficiency. The findings revealed the student were enticed due to improvement in places of learning and strategic vision on quality in Malaysian HEI (Fernandez, 2010). However, it is important to further establishing quality performance indicators which seen readily available in MHEI through specific Key Performance Indicator (KPI). Evaluation tool in management that specifically caters for customer, financial, internal process, and learning and growth perspectives is also important. These aspects are believed included in BSCI as it has direct relationship on the SMHEI. Gonçalves (2009) opines that relationship of BSCI with SHEI enhanced the institution performance expectation based on the vision and strategy of the administrative leaders cordial with the autonomy given by the Ministry of Higher Education, Malaysia (Nur Anisha, 2012; Morshidi, 2010). Nevertheless, initiating BSC directly with SMHEI has input towards satisfying the needs of internal process, satisfy the expectations of the external and internal stakeholders such as government, administrators, and customers and thus shall improve financial perspective of MHEI.

On the other hand, the result has established that insignificant relationship exists between the BSCI and SMHEI through OC (Kline, 2011). The result revealed that there is no indication that balanced scorecard was adopted or embraced through OC. This is consistent with preliminary finding on balanced scorecard adopted in Malaysian corporate establishments. Hence, the findings emphasized that little or few corporate sectors constantly developed causal model for their implementation (Othman, 2006). This study has contributed to the balanced scorecard literature and explore the necessary organizational climate towards the sustainability concept in HEI. The study serves theoretical implication as it enriched further studies in administration through the implementation of quantitative and multivariate analysis. On the other hand, managerial implication mounted on the level of performance and improvement among the administrators in HEIs. However, due to the limitation in terms of sample size, financial constraint and distance the study was conducted only in Peninsular Malaysia and thus the result could not be generalized. The study only used public HEIs and this, for the purpose of widening the scope of generalizability and authenticate the theory, future studies also need to consider to include the private HEIs.

This study indicates the new and preliminary findings on the BSCI, OC and SMHEI. This study found the evidence to suggest that initiating BSC in Malaysian HEI can improve the strategic vision of HEIs and improve their performance towards the SMHEIs. It shows that those who are concerned in organizational climate encountered considerable problem through insufficient communication and freedom of decision-making. Among other things, the absence of KPI emphasis as one of management tool in measuring performance will create difficulties in developing future sustainability (Perkins, Grey & Remmers, 2014). Action plan for financial measures and customer indicated the evidence of improvement for sustaining the future of MHEIs.

References

- Allen, D. (1995), Observable stances, Management Accounting, Vol.73, No.1, p.20-22

- Allen. F, Kirsten F., & Judith B. (2010), Unifying information behaviour and process: a balanced palette and the balanced scorecard, Performance Measurement and Metrics, Vol. 11 Iss 3, p. 280 – 288

- Barth, M. (2015), Implementing Sustainability in Higher Education: Learning in an age of transformation, NY: Earthscan Routledge.

- Bittlestone, R. (1994), Just how well are we doing, Director, Vol.47, No.12, p.44-51

- Brundtland, G. H. (1987), Our Common Future: Report of World Commission on Environment and Development, NY: United Nations General Assembly

- Chan, L. (2004), Performance measurement and adoption of balanced scorecard: A survey of municipal governments in the USA and Canada, The International Journal of Public Sector Management, Vol. 17, Iss2/No.3, p.204

- Chen, S., Yang, C. & Shiau, J. (2006), The application of balanced scorecard in performance evaluation of higher education, The TQM Magazine, Vol. 18, No.2, p.190-205

- Emanuel, R. & Adams, J. N. (2011), College students‟ perceptions of campus sustainability, International Journal of Sustainability in Higher Education, Vol.12, No.1, pg. 79-92

- Fernandez, J. L. (2010), An exploratory study of factors influencing the decision of students to study at Universiti Sains Malaysia, Kajian Malaysia,Vol. 28, No2: 107-136

- Filho, W. L. (2005), Handbook of Sustainability Research, Peter Lang, Frankfurt am Main In Wright, T. (2010), University presidents‟ conceptualizations of sustainability in higher education, International Journal of Sustainability in higher education, Vol. 11, No. 1, p.61-73

- Gonçalves, H. S. (2009), Proposal of a strategy model planning aligned to the balanced scorecard and the quality environments, The TQM Journal,Vol. 21, No.5, p.462-472

- Hair, J. F., Black, W. C., Babin, J. B. & Anderson, R. E. (2010), Multivariate Data Analysis, (7th edn.), New Jersey: Prentice-Hall, Inc

- Halpin, A. W. & Croft, D. B. (1963), The Organizational Climate of Schools: Midwest Administration Center, (p. 89-110) University of Chicago, Chicago, USA

- Hladchenko, M. (2015), Balanced Scorecard – a strategic management system of the higher education institution, International Journal of Educational Management, Vol. 29 Iss 2, p. 167–176

- Hronec, S. (1994), Sinais vitais:usando medidas de desempenho da qualidade, tempo e custo para traçar a rota para o future de sua empresa, Makron Books, São Paulo

- Hu, L. & Bentler, P. M. (1999), Cuttoff Criteria for fit indexes in conventional structure analysis: Conventional criteria versus new criteria alternatives, Structural Equation Modelling: A multidisciplinary Journal, 6 (1), 1-55

- James, L. R. & Jones, A. P. (1974), Psychological climate: dimensions and relationship of individual and aggregated work environment perceptions, Organizational Behaviour and Human Performance, Vol.23, p. 201-250

- Jeswani, S. & Dave, S. (2012), Impact of organizational climate on turnover intention: An empirical analysis on faculty members of technical education of India, International Journal of Business Management &Research, Vol. 2, No.3, p.26-44

- Kaplan, R.R & Norton, D.P. (1992), The balanced scorecard measures-measures that drive performance, Harvard Business Review, (Jan-Feb), 1992.

- Kaplan, R. S. & Norton, D. P. (2004), Strategy Mapping; Converting intangible assets into tangible outcomes, Boston: Harvard Business School Press

- Kaplan, R.S. & Norton, D.P. (1996b) Linking the balanced scorecard to strategy. California Management Review, 39(1)

- Kurland, N. B. (2011), Evaluation of a campus sustainability network: a case study in organizational change, International Journal of Sustainability in Higher Education, Vol. 12 No. 4, pp. 395-429

- Kline, R. B. (2011), Principles and Practice of Structural Equation Modeling, London: The Guilford Press.

- Kahirolmohdsalleh & Nor Lisa Sulaiman (2012), Business Process Reengineering in Malaysia Higher Education institutions, International Journal of Business Management & Research (IJBMR), Vol.2 Iss3, p.1-7

- Lasisi, A. A. & Hairuddin, M. A. (2015), Achieving Sustainability in Nigerian Higher Education Institutions: Responsive Role of the Leaders, Advances In Multidisciplinary & Scientific Research, AIMS Research Journal, Vol. 1, No.2, p.9-16

- Lasisi, A. A. (2016), The effects of organizational quality management initiatives and mediating factor on the sustainability of Malaysian higher education institutions, IIUM: Unpublished: Dissertation

- Lozano, R. (2011), The state of sustainability reporting in universities, International Journal of Sustainability in Higher Education, Vol.12, No.1, pg. 67-78,

- Lee, S. F., Lo, K. K., Leung, R. F. & Sai On Ko, A. (2000), Strategy Formulation Framework for vocational education: Integrating SWOT analysis, balanced scorecard, QFD methodology and MBNQA education criteria, Managerial Auditing Journal, Vol.15, No.8, p.407-423

- McAdam, R. & O’Neill, E. (1999), Taking a critical perspective to the European business excellence model using a balanced scorecard approach: a case study in the service sector, Managing Service Quality, Vol.9, No.3

- Mike Perkins, Anna Grey & Helge Remmers, (2014),"What do we really mean by “Balanced Scorecard”?", International Journal of Productivity and Performance Management, Vol. 63 Iss 2 pp. 148 – 169

- Moore, J. (2005), Seven recommendations for creating sustainability education at the university level: a guide for change agents, International Journal of sustainability in higher education, Vol. 6 (4), p. 326

- Morshidi, bin Sirat, (2010), Strategic planning directions of Malaysia‟s higher education: university autonomy in the midst of political uncertainties, High Educ 59, p.461-473

- Nur Anisha, A. (2012), Performance Measurement in Malaysia’s Higher Education, PMA 2012 Conference, Cambridge UK, 11(13) p.1-10, sources: www.PERFORMANCEPORTAL.ORG retrieved on 15/2/2013

- Olson, L., Arvai, J. & Thorp, L. (2011), Mental models research to inform community outreach for a campus recycling program, International Journal of Sustainability in Higher Education, Vol.12, No.4, pg. 322-33

- Olve, N., Petri, C., Roy, J & Roy, S., (2004) In Yeung, A. K. and Connell, J. (2006), The Application of Niven’s Balanced Scorecard in a Not-For-Profit Organization in Hong Kong: What Are the factors for Success?, Journal of Asia Business Studies, Fall 2006, p.26-33

- Othman, R. (2006), Balanced Scorecard and causal model development: Preliminary findings, Management Decision, Vol.44, No.5, p.690-702

- Pace, C. R. & Stern, G. C. (1958), An approach to the measure of psychological characteristics of college environments, Journal of Educational Psychology, vol.49, no.2, p.269-277

- Peña-Suárez, E., Muñiz, J., Campillo-Álvarez, Á., Fonseca-Pedrero, E. & García-Cueto, E. (2013), Assessing organizational climate: Psychometric properties of the CLIOR Scale, Psicothema, Vol. 25, No. 1, 137-144

- Schalkwyk, F. C. (1998), Total Quality Management and Performance measurement barrier, The TQM Magazine, Vol. 10, No.2

- Thomas, I. (2004), Sustainability in tertiary Curricula: what is stopping it happening? International Journal of Sustainability in Higher Education, Vol.5, No.1, p. 33-47

- Velazquez, L., Munguia, N., & Sanchez, M. (2005), Deterring Sustainability in Higher Education Institutions: An appraisal of the factors which influence sustainability in higher education institutions, International Journal of Sustainability in Higher Education, Vol. 6, No.4 p. 383-391

- Waheed, B., Khan, F. I. & Veitch, B. (2011), Developing a qualitative tool for sustainability assessment of HEIs, International Journal of Sustainability in Higher Education, Vol.12, No.4, pg. 355-368

- Wright, T. (2010), University presidents‟ conceptualizations of sustainability in higher education, International Journal of Sustainability in higher education, Vol. 11, No. 1, p.61-73

- Yeung, A. K. & Connell, J. (2006), The Application of Niven’s Balanced Scorecard in a Not-For-Profit Organization in Hong Kong: What Are the factors for Success?, Journal of Asia Business Studies, Fall 2006, p.26-33

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 May 2018

Article Doi

eBook ISBN

978-1-80296-039-6

Publisher

Future Academy

Volume

40

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1231

Subjects

Business, innovation, sustainability, environment, green business, environmental issues

Cite this article as:

Ali, H. B. M., & Ayodele, L. A. (2018). Balanced Scorecard For Future Sustainability Of Malaysian Higher Education Institutions. In M. Imran Qureshi (Ed.), Technology & Society: A Multidisciplinary Pathway for Sustainable Development, vol 40. European Proceedings of Social and Behavioural Sciences (pp. 1180-1192). Future Academy. https://doi.org/10.15405/epsbs.2018.05.92