The Effects of GST (Goods and Services Tax) on Construction Capital Costs and Housing Property Prices

Abstract

Following the implementation of GST in Malaysia on 1 April 2015, it was predicted that construction capital costs and housing property prices will increase accordingly. Examining the GST effects associated with construction capital costs and its influences towards the housing developers and housing property prices is this study’s primary objective. This study also aims to highlight the developers’ point of view regarding how GST impacts upon them as well as the housing prices of further future proposal of initiatives. The findings are obtained by surveying the opinion of 36 housing developers and an experienced property consultant under the employment of Henry Butcher (International Asset Consultant) in Penang, Malaysia. It was concluded that building materials and land acquisition are the major construction capital costs affected by the GST implementation while capital flow turnover is the post and significant consequence that developers now face which subsequently led to an increment of housing property prices. Ultimately, the end buyers are the ones who bear the brunt of the price increment where the government plays the central role within this scenario.

Keywords: CapitalConstruction CostsGSTHousing PropertyPrice

1. Introduction

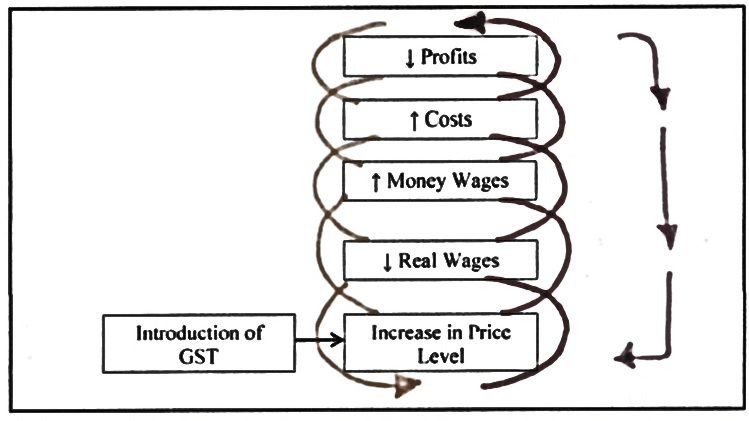

Following the implementation of GST in Malaysia, the primary group affected due to this broad-based consumption tax are the consumers (Warsame, 2006). According to the Malaysian Deputy Finance Minister, living costs will not increase but instead decrease logically as those items being charged 10% of Sales and Service Tax (SST) will then be subjected to a lower 6% of GST only (Aaron, 1981). However, the adoption of GST had increased the price level as illustrated in Figure

2. Impacts of GST on Construction Capital Costs

Building material costs are the major components in construction development costs while GST implementation has been identified to have inflated the construction material prices within a year of implementation (Breen

Findings as shown in Table

Besides, marketing costs has also been raised after GST implementation which may be a result of developers outsourcing marketing agents to help them boost the sales of property while the agents are entitled to as much as 5% of the project’s Gross Development Value, leading to higher marketing costs for the developers. Moreover, labour cost as indicated at Table

3. Impact of GST on Housing Developers & Housing Property Prices

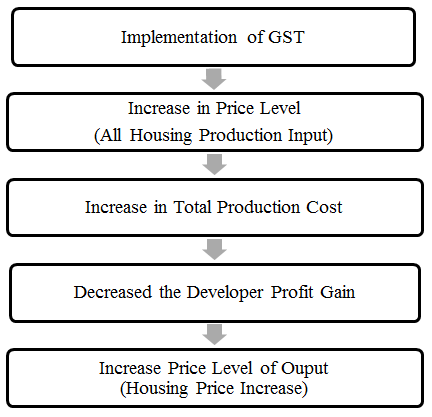

GST implementations in reality will not directly affect the business profitability but instead affects one’s living cost and eventually one’s purchasing power (Grigore and Gurau, 2013). Due to the lack of purchasing power, it will indirectly led to a waning sales of property as the development costs is brought up by 6% where the 6% charged is for the price of the final product which is housing property prices.

For a developer, their projects include residential properties and also commercial properties. Sales of commercial properties being charged an additional 6% of standard rate and developers are able to claim back the 6% from the government within one month. Hence, developer cash flow should not face any issue. However, all of the developers surveyed have not yet received any payback from the government after GST implementation due to the government system being temporarily offline, calculation error and the authorities still in the learning process of the new system.

Although housing properties are exempted from GST, the late tax claim refund from the government for the commercial properties will result in difficulties within an organisation’s overall cash flow which is the critical circumstance that all respondents are facing (Englund

Once the housing property prices increase due to GST implementation eventually the end buyers will bear and suffer the price increment. The main reason is due to developers’ entrepreneur objective which aims for profit maximisation. Although GST is said to be absorbed by housing developers on surface, but in reality, the final housing prices have already increased although only more than 3.41% and not 6%.

In conclusion, GST does affect housing developers in terms of cash flow (financial tightening) and work overload. Cash flow turnover leads to developer’s increasing the output prices while the ones who bear the price increment are the end buyers who act as the last consumer within a supply chain whereas the complexity of the claiming procedure results in one’s work overload and confusion.

4. Initiatives and Suggestions for Malaysian Housing Developers

Transferring all the cost increment to the end buyers is the priority decision among all of the developers. However such a measure will result in an increment of the housing property prices and thus is unadvisable. The initiative of using in-house sources which is recommended by MCT Executive Director is not an effective solution to soften the GST impact either as professional soft costs are just a small portion in a project. However, such small portioned savings can help an organisation to allocate their resources onto other operational fields.

On the other hand, promotions such as giving discounts between 5-10% for those buyers who can pay their instalments within a single payment is necessary in order to push up sales rate although developers will still sustain some losses. Additionally, the late claiming issues can be overcome if an organisation establishes a GST specialist department to handle all GST related issues. Although investment in a new department may be costly initially, however it can provide a positive return in the long run. Yet, all the suggestions above are not the most effective as that particular solution lies within the government’s role because government is the one who can ensure that the GST implementation can be ran efficiently. Once everything is proceeding smoothly, then only anything can be settled easily.

Hence, for this moment, the most urgent issue which the government should tackle first is to list all the claimable guidelines clearly and make the claiming process faster so to ensure an organisation’s cash flow can be proceeded smoothly. However, if the government would not abolish the GST implementation, then they must at least make housing properties less than RM500k into zero-rated tax items. Moreover, subsidies can also be provided for the developers as the Gross Development Value can be reduced while Gross Development Costs can be decreased automatically. For example, Prima and MyHome projects are the projects receiving subsidies from the federal government.

Meanwhile, the local government can alter certain policies or reduce other taxes such as stamp duty to help in lowering the GST impact (Obst et al., 1999). Due to subsidies and increase in population density per hectare of land, housing developers would be able to build more economic houses and thus property prices would become cheaper while the sales rate becomes greater. As a side note from the findings, it was found that Malaysian NGOs within the construction field have no obvious function other than to act as the informer who passes along messages.

In conclusion, the ones who can directly help in lowering the GST impact on the housing developers are the federal and local governments. The federal government needs to improve itself and cooperate with the developers to ensure that all related can benefit from this tax implementation.

5. Conclusion

Overall, building materials and land acquisition costs are the major construction cost components to receive the most significant impact due to GST implementation. On the other hand, cost increment due to GST and exempted taxes have caused various issues in the developers’ business capital flow. In order to maintain profit and cover the risk of losses developers have resorted to raising the housing prices where the end buyers will ultimately bear the price increment. Therefore the government should wisen up and strives to transform the critical scenario for the developers and housing buyers into a win-win situation.

References

- Aaron, J.H. (1981). The Value-added Tax: Lessons from Europe. Washington, D.C.: Brookings Institution.

- Anthony G. (2008). Submission Australian Tax Review 17/10/2008, Australian and New Zealand Property Journal, Sept. 2007, l1(3)

- BERNAMA (2014). Perception That GST Will Increase Cost of Living Not Right - Ahmad Maslan. Pontian, Malaysia. Retrieved from http://web10.bernama.com/gst/news.php?id=1087060

- Breen J., Bergin-Seers S., Roberts I., & Sims R. (2002). The Impact of the Introduction of the GST on Small Business in Australia. Asian Review of Accounting, 10(1), 89–104.

- Burgess J. Kniest P. and Lee J. (1998). Introduction to Macroeconomics Workbook Answers, Australia, Machillan Education AU.

- Daliæ M. (1999). Price Effects of Value Added Tax. (53), 5–28.

- Englund P., Hendershott P. H., & Turner B. (1995). The Tax Reform and the Housing Market. Swedish Economic Policy Review, 2, 319–356.

- Godsell D. (2013). The Bahamas The Economic Consequences of the Value-Added Tax for the Bahamas, Bahamian. Retrieved from http://www.nassauinstitute.org/files/VATEconomicConsequencesBahamas.pdf

- Grigore M. Z. & Gurău M. (2013) Impact of VAT on the Profitability and the Cash Flow of Romanian Small and Medium Enterprises. Global Economic Observer, 2(1), 170–180,

- Obst W., Graham R., Binney W., & Christie G. (1999). Agribusiness Financial Management (pp. 1–5). The Federation Press.

- Warsame, A. (2006). Supplier Structure and Housing Construction Costs.

- Zainal R., Teoh C.T., & Shamsudin Z. (2015). A Review of Goods and Services Tax (GST) on Construction Capital Cost and Housing Property Price. Proceeding of 4th International Conference on Technology Management, Business and Entrepreneurship, Melaka, Malaysia.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

22 August 2016

Article Doi

eBook ISBN

978-1-80296-013-6

Publisher

Future Academy

Volume

14

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-883

Subjects

Sociology, work, labour, organizational theory, organizational behaviour, social impact, environmental issues

Cite this article as:

Zainal, R., Teng, T. C., & Pin, Y. S. (2016). The Effects of GST (Goods and Services Tax) on Construction Capital Costs and Housing Property Prices. In B. Mohamad (Ed.), Challenge of Ensuring Research Rigor in Soft Sciences, vol 14. European Proceedings of Social and Behavioural Sciences (pp. 349-354). Future Academy. https://doi.org/10.15405/epsbs.2016.08.49