Web-Based Sustainability Reporting: Evidence From State Islamic Religious Councils in Malaysia

Abstract

Web-based disclosure on sustainability offers significant benefits of the Internet in promoting transparency and accountability in government entities, including religious bodies. Web disclosure also functions as an important means of discharging accountability in organizations. Despite its advantages, current evidence indicates a lack of empirical evidence on the extent and quality of disclosure of sustainability-related information on the websites of State Islamic Religious Councils in Malaysia. Hence, this study examines the extent and quality of SIRC websites’ disclosure in communicating sustainability-related information to their stakeholders. A new SIRC sustainability-related web disclosure index was developed and used in performing a content analysis of the SIRC's websites. Findings demonstrated variations in the extent and quality of disclosure among all SIRCs across four elements: environmental, social, economic, zakat and waqf. Hence, future effort is required to ensure uniformity in the content and quality of disclosure. The findings provide valuable input for the government to strengthen the role of SIRCs in achieving sustainable development goals.

Keywords: Islam, religious bodies, sustainability reporting, uniformity, web-based disclosuret

Introduction

The Internet has transformed how information is communicated and shared, becoming a vital tool for promoting transparency and accountability (Othman et al., 2020; Utama, 2020). Recent studies have highlighted the significant impact of the Internet in promoting transparency and accountability in government bodies. For instance, a study by the Pew Research Centre found that "the Internet has played a major role in increasing government transparency and accountability, particularly through the provision of access to government information and data" (Rainie et al., 2021, p. 7). Furthermore, the Internet has enabled citizens to access a wealth of information previously inaccessible or difficult to obtain. This has facilitated greater participation in governance and decision-making, as citizens are better informed about government policies and actions. As noted by Michener et al. (2020), "the Internet has enabled citizens to hold their governments accountable for their actions and demand greater transparency in decision-making processes" (p. 2).

Websites are among the digital platforms used to disseminate information to investors and other stakeholders worldwide (Abdi et al., 2021). Web disclosure is widely regarded as an important means of discharging accountability in the corporate and government sectors. Alsartawi and Reyad (2021) noted that organisations can improve their websites by including more content reflective of transparency and due diligence, which is viewed as beneficial since organisations can build and maintain long-term relationships with investors and other stakeholders, thus positively influencing their performance. Nevertheless, there are still unclear guidelines for communicating information, while the choice of website content remains dependent on the discretion of the companies and their managers (Jerry et al., 2015). This situation leads to a lack of uniformity in the contents of information and its form of presentation (Abdi et al., 2021).

With the growth of website disclosure, several studies have focused on studying the practices of web-based disclosure in Malaysia, including that by Nair et al. (2023), Ibrahim et al. (2022) and Ramli and Kamaruddin (2017). However, to date, there is still a lack of studies examining web-based disclosure of religious-based organisations, particularly in the context of supporting sustainability goals. In Malaysia, religious bodies responsible for the administration and management of Islamic affairs are known as the State Islamic Religious Councils (SIRCs) or Majlis Agama Islam Negeri. These councils are state-level institutions led by a chief religious officer or Mufti. The councils are responsible for a wide range of Islamic matters, including managing Islamic institutions like mosques, developing Islamic education, regulating Islamic religious practices and rituals, and enforcing Islamic law or Shariah. The functions and powers of each MAIN are governed by state Islamic laws, which may vary from state to state.

The SIRCs represent a wide range of stakeholders, including government agencies, religious scholars and members of the public. As such, they are accountable to various actors, including the SIRC's board, the government and the wider public (Masruki et al., 2022). From the perspective of website disclosure, the information disclosed by SIRCs on their websites provides access to the public with information they deem important, including those related to sustainability. These website reports represent one of the ways by which Islamic non-profit organisations can improve stakeholders’ perceptions of their accountability (Ramli & Kamaruddin, 2017).

On the other hand, sustainability reporting is increasingly becoming an important practice among religious bodies because it promotes ethical and socially responsible behaviour. Religious organisations are influential institutions that significantly impact the communities they serve. As such, they have a moral responsibility to promote sustainable practices and contribute to attaining the United Nations Sustainable Development Goals (SDGs). Sustainability reporting is also a critical tool for religious bodies to communicate their commitment to sustainability and demonstrate how they integrate sustainability principles into their operations, programs and initiatives. Through sustainability reporting, religious bodies can identify and prioritise sustainability issues, set sustainability goals and targets, and measure and report on their progress towards achieving those goals. Despite the importance of website disclosure on sustainability by religious bodies, there is a current lack of evidence on how the Malaysian SIRCs fulfil this role. Thus, this study examines the extent and quality of disclosure to which the SIRCs use their websites to communicate sustainability-related information to their stakeholders.

The following sections present the literature relevant to web-based sustainability reporting, reporting on Islamic institutions followed by the State Islamic Religious Councils. In addition, a web-based sustainability reporting model underpinning this research is provided. The methodology section sheds light on the main data collection and analysis methods. The subsequent sections discuss the analysis and findings. Finally, the conclusions are presented in the last section.

Literature Review

Reporting in Islamic Institutions

Within the Muslim community, Islamic religious organizations are established to manage the Muslim economy, the reduction of poverty, social welfare, educational opportunities, and healthcare resources (Zain et al., 2014). The State Islamic Religious Council (SIRC) oversees all matters relating to Islam in Malaysia. According to Mahadi et al. (2018) and Zain et al. (2014), the SIRC is responsible for advising the Head of the Islamic Religion on all matters pertaining to Islam and for managing Islamic riches such as zakat, waqf, baitulmal, and other resources. The SIRCs must report and disclose all financial and non-financial information to the relevant stakeholders as part of their performance of these duties, either through the financial statements (Abu Bakar et al., 2020) or through other channels, such as the SIRC's website.

According to Abu Bakar et al. (2020), the main purpose of Islamic Reporting is to provide users, particularly stakeholders, with information about financial operations and the performance of religious institutions during a defined time period. This could also include how well private companies manage risky situations (Hamid et al., 2014). Full disclosure, social accountability, and transparency are three essential standards for Islamic reporting from an Islamic perspective (AAOIFI, 2019; Baydoun & Willett, 2000). The first criterion is full disclosure, which emphasizes that the Muslim community has a right to know how the Islamic religious institutions operate and perform (Abu Bakar et al., 2020). This criterion requires Islamic religious institutions to disclose all relevant information, including environmental, economic, and social fairly (Global Reporting Initiative, 2021; Yusof, 2016).

Social accountability (AAOIFI, 2019) is the second criterion for greater Islamic reporting and disclosure, and it refers to the responsibility and accountability of Islamic religious institutions to equally describe all financial and non-financial facts for the benefit of the ummah (Zain et al., 2014). Since Muslims are accountable for their actions and must consider their responsibility towards society because their deeds will affect the community, they, along with community leaders, must learn the truth in order to understand the impact of a person or a business on the community's well-being (Abdillah et al., 2021; Farook, 2007). The third criterion, transparency, calls on organizations to protect the financial and non-financial information supplied in an understandable and faithful manner (AAOIFI, 2019). Through adequate and appropriate disclosure, transparency may develop (Abu Bakar et al., 2020). Regardless of whether the information is favorable or unfavorable in the eyes of the Islamic religious organizations, the information revealed should include all pertinent information necessary to make it helpful to the stakeholders (Abu Bakar et al., 2020; Farook, 2007).

In order to increase openness and the caliber of the reporting, Abu Bakar et al. (2020) recommended two new criteria to the SIRCs, namely a statement of shariah compliance and a statement of the SIRC's obligations on baitulmal, zakat, and waqf. This study aims to give a general overview of disclosures made on the SIRCs' websites in Malaysia that fall under the categories of social, economic, social, and environmental information. It does so by taking into account the literature on reporting elements of SIRCs through the websites.

State Islamic Religious Councils (SIRCs)

Within the Muslim community, Islamic religious organizations are established to manage the Muslim economy, the reduction of poverty, social welfare, education, and healthcare facilities (Zain et al., 2014). The State Islamic Religious Council (SIRC) oversees all matters relating to Islam in Malaysia. According to Mahadi et al. (2018) and Zain et al. (2014), the SIRC is responsible for advising the Head of the Islamic Religion on all matters pertaining to Islam and for managing Islamic riches such as zakat, waqf, baitulmal, and other resources. The SIRCs must report and disclose all financial and non-financial information to the relevant stakeholders as part of their performance of these duties, either through the financial statements (Abu Bakar et al., 2020) or through other channels, such as the SIRC's website.

According to Abu Bakar et al. (2020), the main purpose of Islamic Reporting is to provide information about the financial operations and performance of religious institutions during a given time period to help users, particularly stakeholders, make decisions. From an Islamic perspective, complete disclosure, social accountability, and transparency are three essential standards for Islamic reporting (AAOIFI, 2019; Baydoun & Willett, 2000). The Muslim community has a right to know how Islamic religious institutions operate and perform (Abu Bakar et al., 2020), so full disclosure is the first criterion, which calls for these institutions to disclose all relevant information, including environmental, economic, and social fairly (Global Reporting Initiative, 2021).

Social accountability (AAOIFI, 2019) refers to the responsibility and duty of Islamic religious institutions to describe all financial and non-financial facts equally for the benefit of the ummah (Zain et al., 2014). It is the second requirement for greater Islamic reporting and disclosure. Knowing how a person or company affects the community's well-being is essential for the Muslim community to learn the truth, as Muslims are accountable for their acts and must consider how they influence the community as a whole (Farook, 2007). AAOIFI, 2019). The third criterion, transparency, calls for organizations to protect the financial and non-financial information presented in a faithful depiction and understandable manner. A adequate and appropriate disclosure may lead to transparency (Abu Bakar et al., 2020). Regardless of whether the information is favorable or unfavorable in the eyes of the Islamic religious organizations, the information given should include all pertinent facts necessary to make them valuable to the stakeholders (Abu Bakar et al., 2020; Farook, 2007).

In order to increase openness and the caliber of the reporting, Abu Bakar et al. (2020) recommended two new criteria to the SIRCs, namely a statement of shariah compliance and a statement of the SIRC's obligations on baitulmal, zakat, and waqf. This study aims to offer an overview of disclosures on the SIRCs' websites in Malaysia within the context of social, economic, social, and environmental information. It does so by taking into account the literature on reporting features of SIRCs through the websites.

Web-based Sustainability Reporting

In particular, it serves as a medium to assess the economic, environmental, and social impacts of an organization's capacity to attain sustainable development goals and oversee its societal impact (Global Reporting Initiative, 2004; Meutia et al., 2021). Sustainability reporting is concerned with issues relating to economic, social, environmental, and governance performance.

In order to convey their responsibilities to society, the communication channels for sustainability reporting have changed from yearly reports to standalone sustainability reports and, more recently, internet-based technologies through web-based reporting (Lodhia, 2018; Mion & Loza Adaui, 2019; Parker & Gould, 1999). Modern information and communication technology have changed how reporting operates. Therefore, web-based disclosure may, through its interactive potential and facilitation of communication with stakeholders, increase the capabilities of conventional media as opposed to one-directional reporting (Joseph, 2010; Joseph et al., 2014; Lodhia, 2018). According to Selahudin et al. (2014), disclosures by organizations must be able to inform readers of any malfunctions and unethical activities that are being used.

Previous research on online sustainability reporting by businesses, non-profit organizations, and governments (Che Ku Kassim et al., 2019; Gaia & John Jones, 2017; Nicolò et al., 2021; Parker & Gould, 1999) was published (Correia et al., 2021). Environmental and social information was disclosed less frequently than economic and customer-related information on the websites of Portuguese companies (Correia et al., 2021). Companies with higher incomes and publicly traded companies were observed to disclose more sustainable development information on their websites (Carvalho et al., 2018). On the other hand, by helping local sporting clubs achieve their goals and thereby improve their values, the disclosure of sustainability information on their websites has increased their earnings and opened up new opportunities for sponsorship (Burgess et al., 2021).

Comparatively, research has shown that the public and private sectors typically provide different information on their websites. For instance, Midin et al. (2017) discovered that, in contrast to the commercial sector, the public sector rarely releases information about stakeholder engagement. Only 30% of stakeholder interaction items were found to be reported on Malaysian local government websites, indicating a lack of transparency. On the other hand, stakeholders began to place a high priority on information connected to the environment. According to Che Ku Kassim et al. (2019), the stakeholders want greater transparency on an organization's impact on the environment and sustainability issues such biodiversity loss, climate change, and global warming. However, in the UK, information provided through web-based reporting on local biodiversity is somewhat patchy, making it difficult for interested parties to administer a comprehensive understanding of the current status of the local biodiversity (Gaia & John Jones, 2017). On the other hand, despite the lack of pertinent laws and regulations, Malaysian local councils took the initiative to provide detailed environmental disclosure on their websites (Che Ku Kassim et al., 2019).

The improvement of fiscal transparency in the public sector and web-based accountability measures have been linked in previous studies. A communication and engagement tool that encourages accountability improvement is the web-based accountability practice, which makes reporting and receiving feedback or input from stakeholders accessible online (Saxton & Guo, 2011). Organizations must publish important organizational data, performance, and political accountability to show they are accountable. In fact, a local study on the website for the public sector's financial, performance, and political accountability established web-based accountability as one of the variables to win over the people's trust, with political accountability being the key variation (Ibrahim et al., 2022).

Indeed, leveraging websites gives the public and commercial sectors a strategic chance to manage their potential advantages, increasing the volume and diversity of sustainability information that is supplied. ICT advancements make it possible to prepare, upload, and disseminate sustainability information in a way that is efficient, affordable, and capable of reaching a larger audience.

Web-based Sustainability Disclosure Index

Due to its interactive character, which may present real-time statistics and up-to-date information on any program, a website is a vehicle for organizations to transmit sustainable information (Bilu et al., 2016; Darus et al., 2013). In order to convey organizational direction, purpose and objectives, human resource organization structure, and the goal of each division, the Malaysian state government websites have produced a set of vision and mission statements (Ibrahim et al., 2022). If maintained through proper exposure and advice reporting processes, these websites can offer useful reporting of their occurrences. In order to increase web-based disclosure practices, measures should be put in place (Nair et al., 2023). The website-based categorization of the disclosure's role may make it easier for stakeholders to quickly find the information and improve the unit's accountability.

According to Masruki et al. (2018), stakeholders have long been curious about information pertaining to governmental and nonprofit organizations. By merging the national and international reporting criteria for SIRC and religious-based organizations, the disclosure index, specifically for the SIRC, must be used to meet the expectations of various stakeholders from the SIRCs' annual reports. The financial statement (FS), strategic information (SI), non-financial performance (NFP), financial performance (FP), and corporate information (CI) are the foundations for these disclosure item types, according to Masruki et al. (2016).

Conceptual Framework

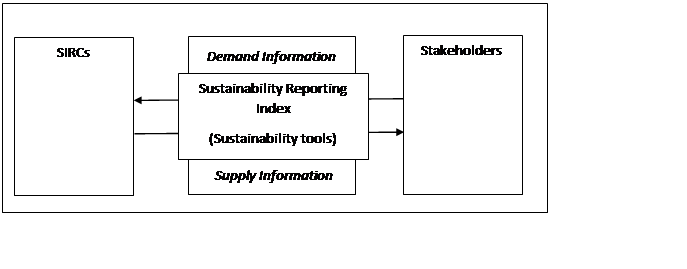

The Ramli and Kamaruddin (2017) study, which focused on web-based accountability disclosure of zakat organizations, served as the inspiration for the conceptual framework used in this investigation. A new Sustainability Reporting Index (SRI) model was created in this study using the study's findings, where SRI serves as a sustainability tool, as shown in Figure 1 above.

Since the model illustrates the relationship between information demand and supply among SIRCs and stakeholders, the Sustainability Reporting Index gains importance as a tool that should be taken into consideration by organizations with several stakeholders.

Methodology

In order to understand more about concerns connected to disclosure on institution websites, a review of the disclosure literature was conducted. Qualitative features were emphasized as this article discussed the quantity and quality of information regarding the SIRCs' sustainability component. The disclosure index utilized in this study was modified from a prior investigation conducted in Malaysia by Joseph (2010), Abu Bakar et al. (2020) and Masruki et al. (2016) focusing on the sustainability elements of environmental, social, economic, zakat and waqf. The closest study using the SIRC as the unit of analysis was done by Masruki et al. (2016) who developed the accountability index for SIRCs, but a specific study on sustainability reporting within SIRCs’ websites in Malaysia is yet to be noted. In this study, analysis in the form of content analysis over elements related to sustainability reporting was performed.

Findings and Discussion

Demography of State Islamic Religious Council (SIRCs)

For this study, 14 websites of 13 SIRCs and the federal territory Islamic religious council in Malaysia were analysed. The disclosure index presented was categorised into 5 regions consisting of the northern, central, southern, east coast of Peninsular Malaysia and East Malaysia. The state councils for each region were denoted as SR1, SR4 and SR5 representing the southern, SR2, SR6, SR7 and SR8 representing the northern, SR3 and SR9 representing the central, SR10, SR11 and SR12 representing the east coast, and SR13 and SR14 representing East Malaysia, respectively.

Analysis of disclosure index of SIRCs by regions in Malaysia

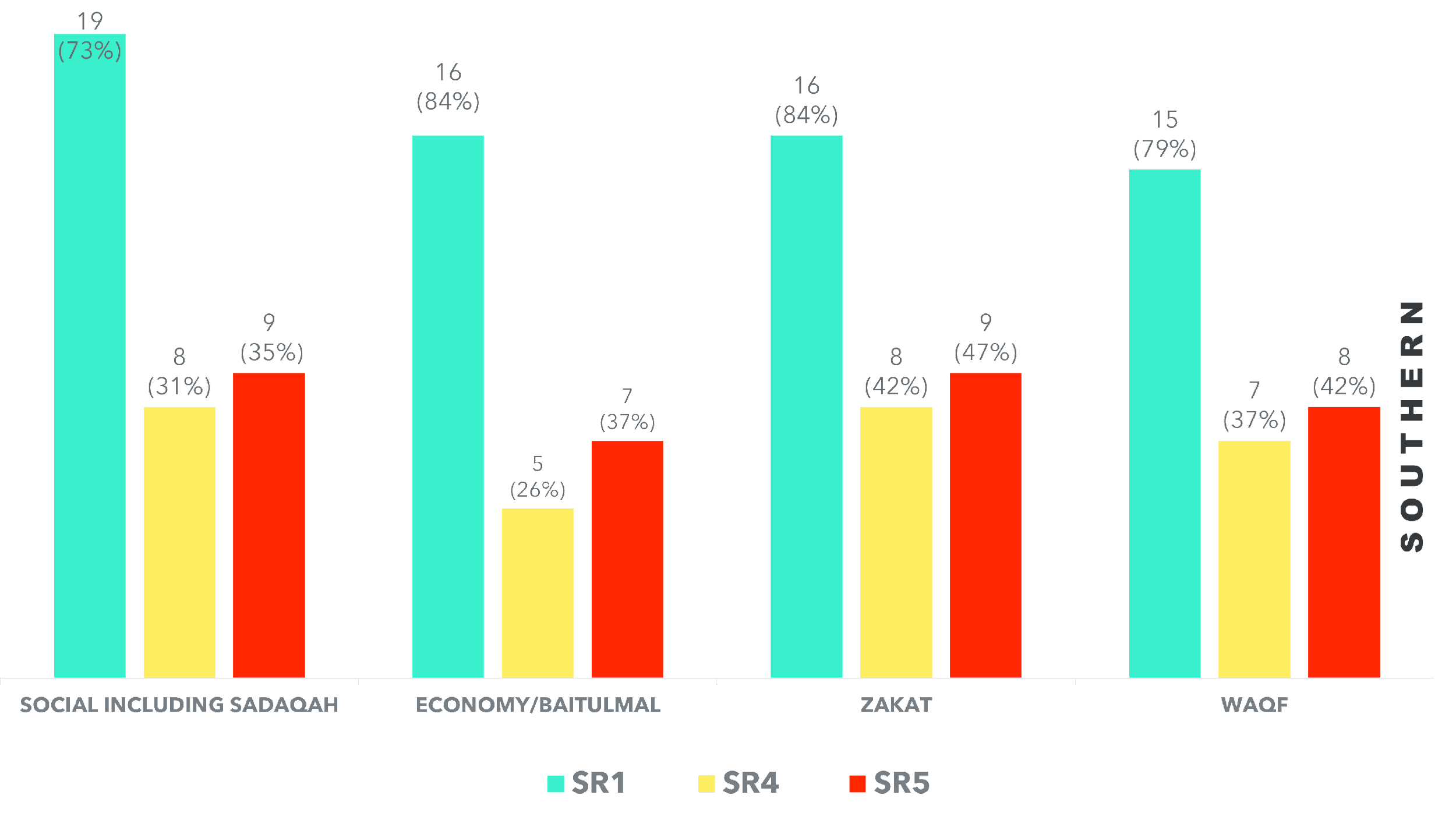

As depicted in Figure 2, the southern region is represented by respondents SR1, SR4 and SR5. SR1 showed the highest disclosure index of all themes including social information with 19 items, economy/Baitulmal information with 16 items, zakat with 16 items and waqf with 15 items. The second rank disclosure was SR5, whereas the least was SR4 among all the themes shown above. None of the SIRCs in the southern region showed the information for shariah compliance and environment.

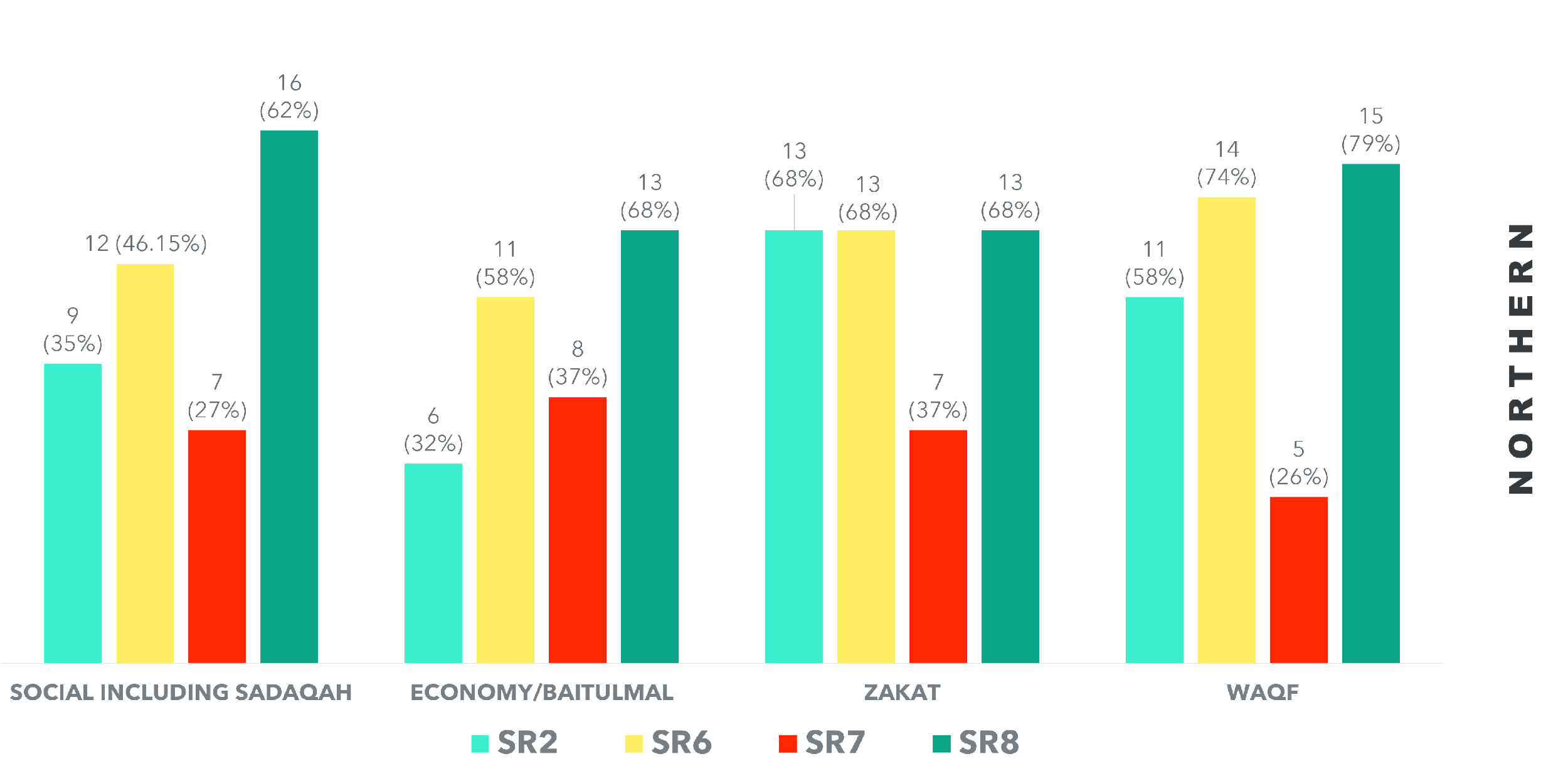

As shown in Figure 3, the northern region is represented by SR2, SR6, SR7 and SR8. For social (including sadaqah) information, SR8 disclosed 16 items followed by SR6 with 12 items, SR2 with nine items and seven items for SR7. For economy/Baitulmal information, SR8 disclosed 13 items followed by 11, 8 and 6 items disclosed by SR6, SR7 and SR8, respectively. For zakat information, SR2, SR6 and SR8 have disclosed equally 13 items, respectively, followed by SR7 with seven items. Meanwhile for waqf information, SR8 disclosed 15 items followed by SR6 with 14 items, SR2 with 11 items and SR7 with five items. Similar to the southern region SIRCs, none of the SIRCs in the northern region displayed information for shariah compliance and environment.

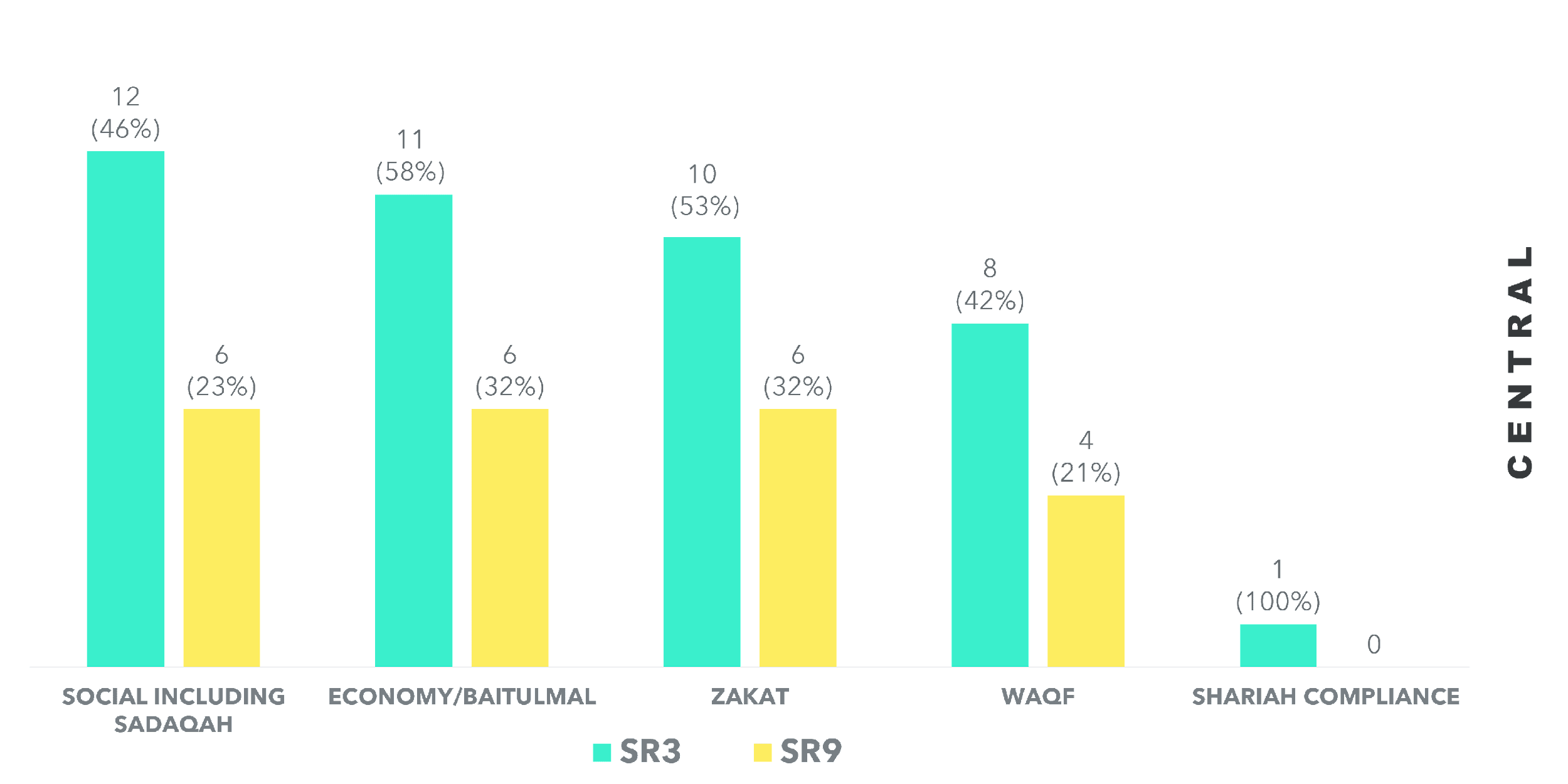

Figure 4 presents the central region comprising SR3 and SR9. For social (including sadaqah) information, SR3 disclosed 12 items and SR9 only had six items. For economy/Baitulmal information, SR3 disclosed 11 items and SR9 only six items. For zakat information, SR3 disclosed 10 items while SR9 disclosed only six items. For waqf information, SR3 disclosed eight items, whereas SR9 only had four items. For shariah information, only SR3 has mentioned shariah information on its website. Further, it was discovered that none of the SIRCs in the central region exposed information on the environment.

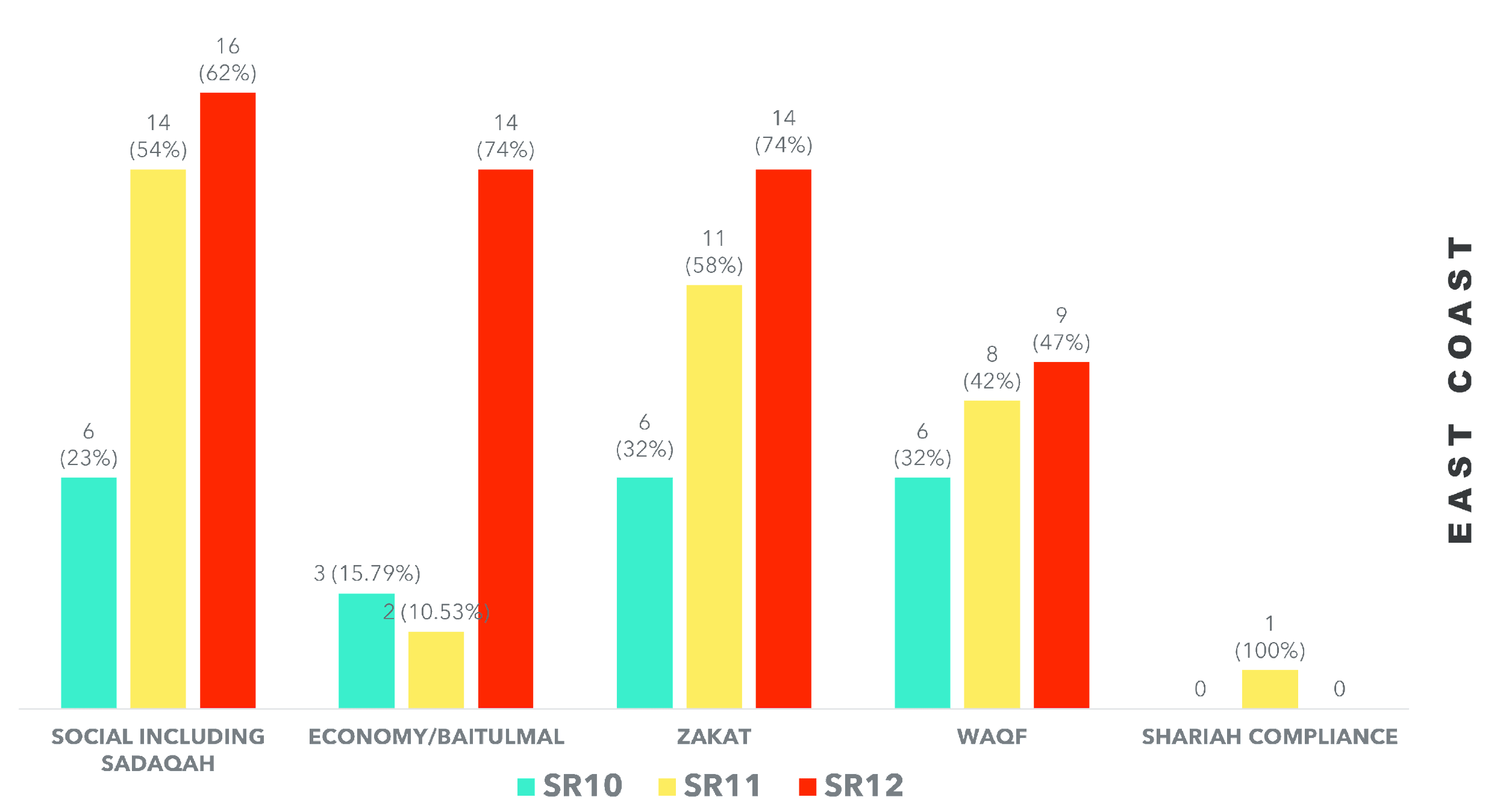

As revealed in Figure 5, the east coast region consists of SR10, SR11 and SR12. For social (including sadaqah) information, SR12 disclosed 16 items followed by SR11 with 14 items and SR10 with six items. For economy/Baitulmal information, SR12 disclosed 14 items followed by SR10 with 3 items and SR11 with only two items. As for zakat information, SR12 disclosed 14 items followed by SR11 with 11 items and SR10 with six items. In terms of waqf information, SR12 disclosed nine items followed by SR11 with 8 items and SR10 with six items. For shariah information, only SR11 have disclosed the shariah information on its website. None of the SIRCs in the east coast region showed information on the environment.

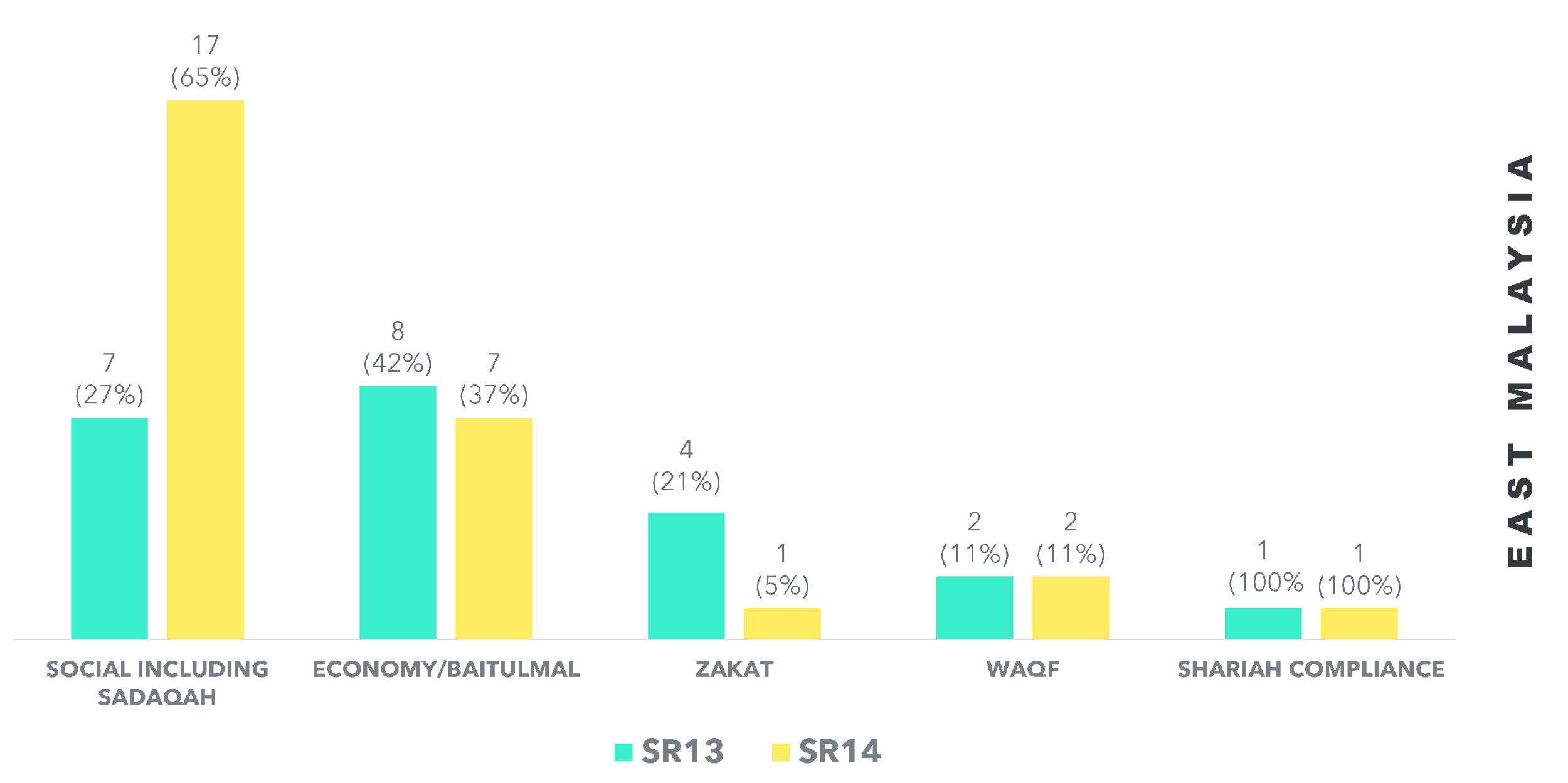

Figure 6 illustrates the disclosure index for East Malaysia’s SIRCs, which represents two SIRCs denoted as SR13 and SR14. For social (including sadaqah) information, SR14 disclosed 17 items while SR13 with only seven items. For economy/baitulmal information, SR13 disclosed 8 items, whereas SR9 disclosed seven items. For zakat information, SR13 disclosed 4 items and SR14 only had one item. For waqf information, SR13 and SR14 equally disclosed two items. For shariah information, SR13 and SR14 stated the shariah information on their websites. None of the SIRCs in East Malaysia disclosed any information on the environment on their websites.

Analysis of disclosure of social information

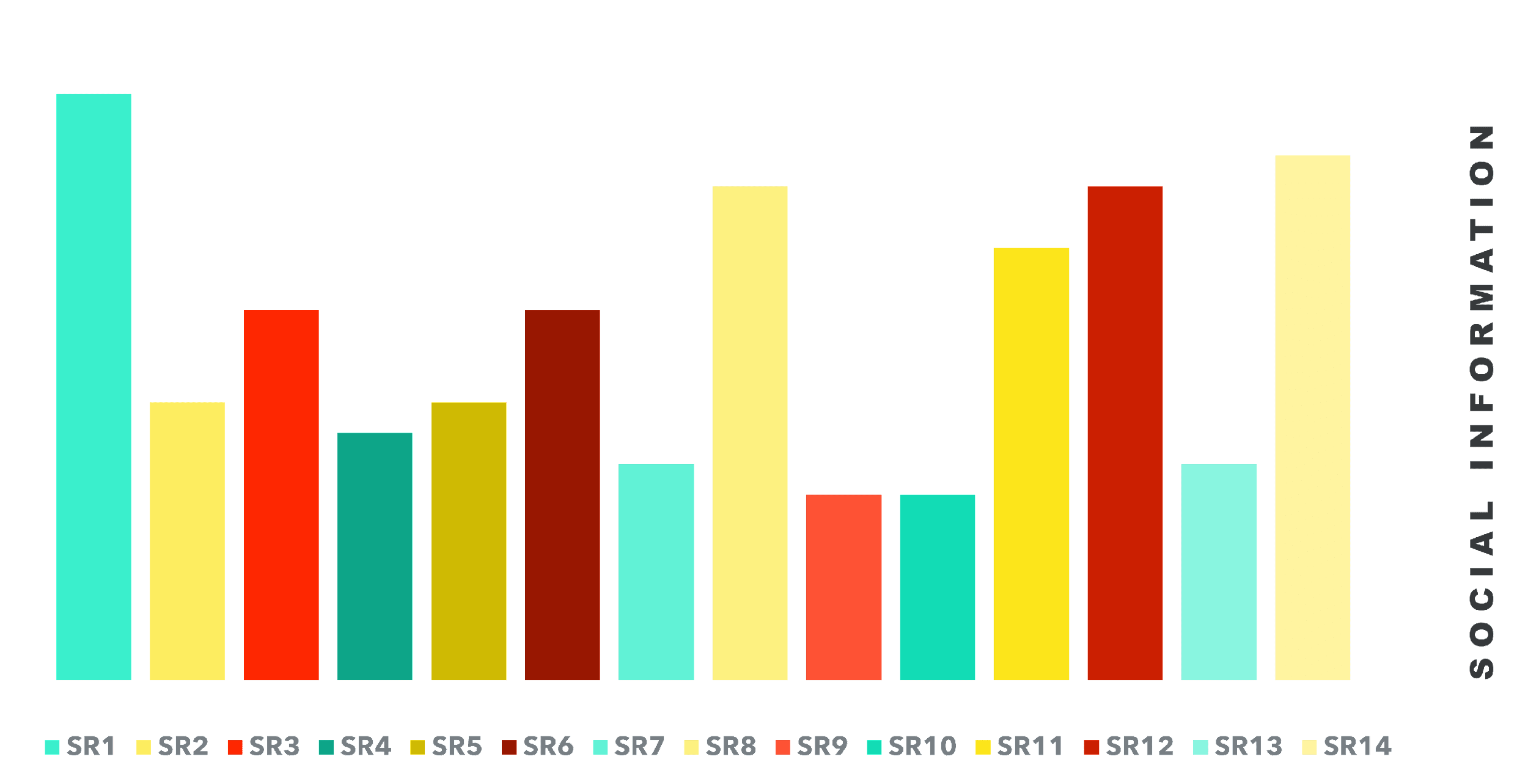

During their social activities, SIRCs made a total of 26 items public, including sadaqah and financial relief for flood victims, Muslim converts, orphans, and single parents. The actions were made public in the client charter, general statement, social issues strategy, social aims, chairman's remarks, and social services. All websites were noted to have disclosed the items as stated in Figure 7, of which SR1 scored the highest at 73% (19) and the lowest score was obtained by SR9 and SR10 with 23% (6).

Analysis of disclosure of economy/baitulmal information

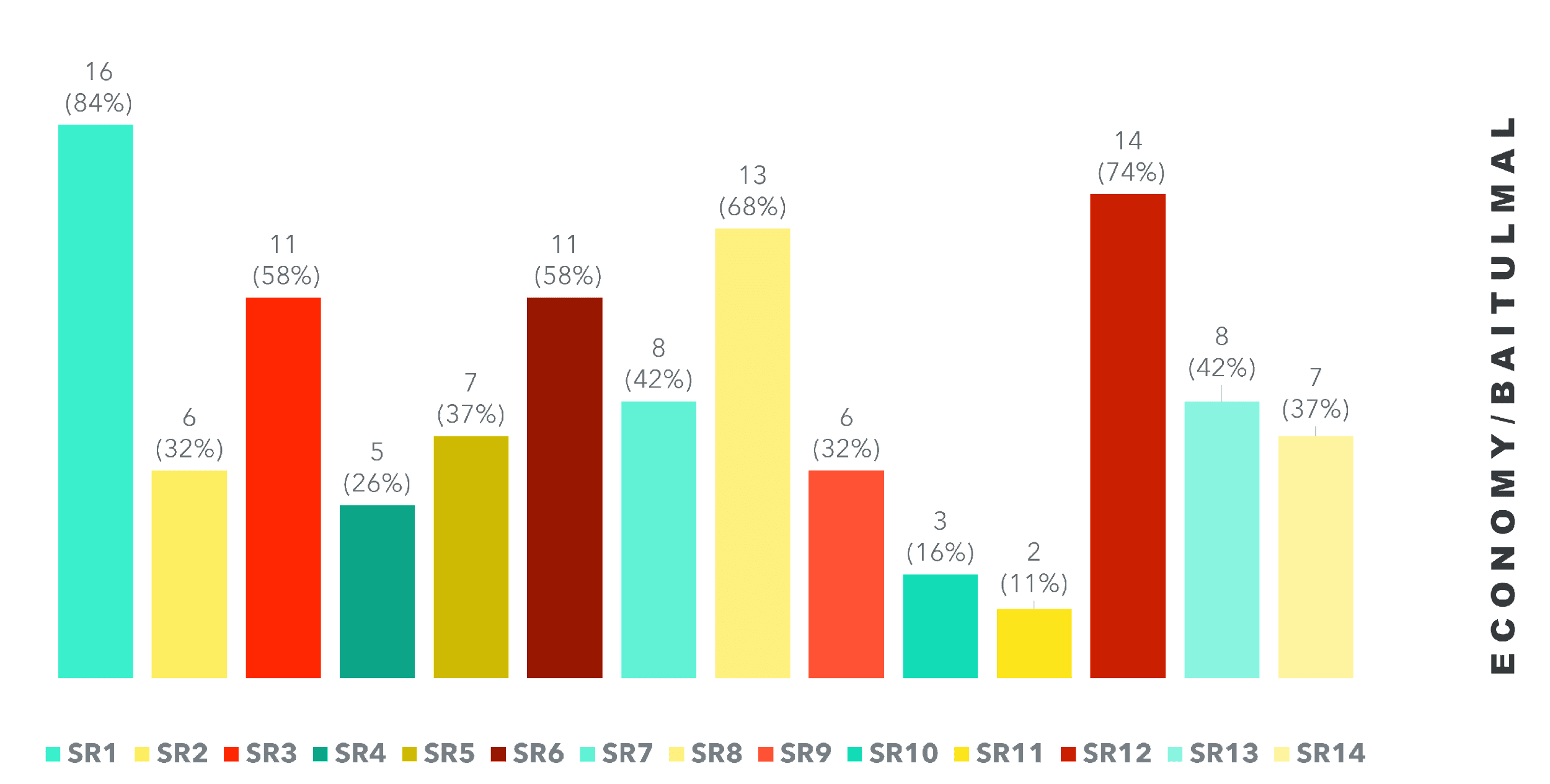

This study views the economic information in web-based reporting in the form of information on how Baitulmal is being managed. Each SIRC has a sub-entity called Baitulmal that is in charge of administering the money that is raised and given out by the SIRCs. Due to this, information on any Baitulmal activity is translated from disclosure of commercial concerns. 19 items were found to be communicated by SIRCs as Baitulmal information, mostly in the form of general statements, client charters, Baitulmal activities, services provided, and stakeholder comments. Additionally, they provided website users with information about the economy, including its vision, goal, objectives, and strategies. Figure 8 below shows the result of the analysis on economy/Baitulmal information, and all websites have disclosed the items of which SR1 scored the highest with 84% (16) and the lowest was scored by SR11 with 11% (2).

Analysis of disclosure of zakat information

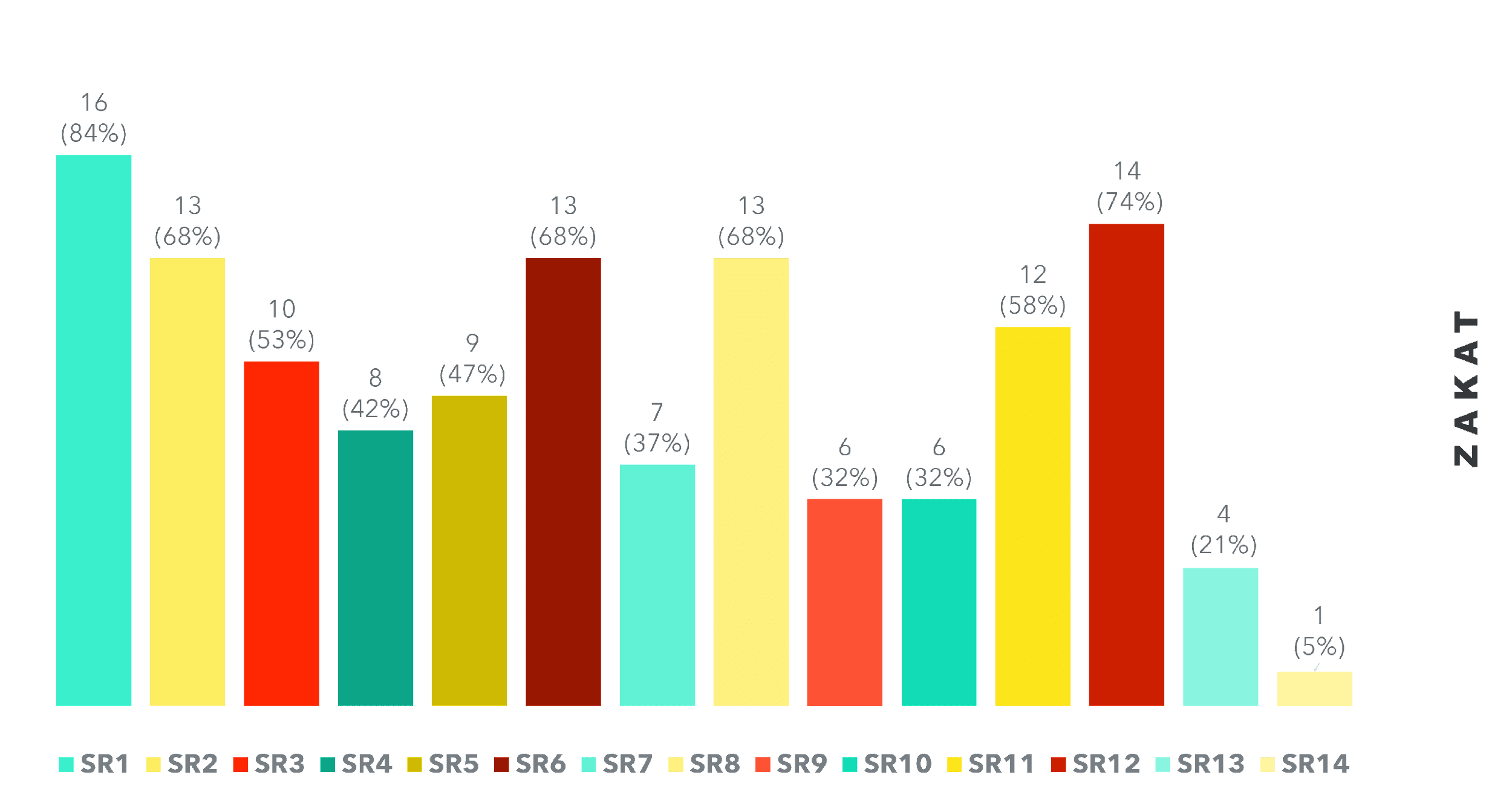

In general, this study found that all websites disclosed information on zakat extensively. Nineteen disclosure items were indexed to be categorised under Zakat information. General remarks and website headlines on the homepage are frequent disclosure items among websites. Additional zakat details are highlighted in several sections of the websites through their client charter, purpose, vision, core values, and as a part of continuous improvement programs within the quality management system. Every SIRC's website has a section dedicated to zakat that contains details about zakat operations, services, and financial disclosures. However, not all SIRCs make public their zakat-related plans, targets, and performance metrics including output, efficiency, and effectiveness. Figure 9 shows the result of analysis on zakat information of which SR1 scored the highest at 84% (16 items), while SR14 scored the lowest with 5% or only one item according to the disclosure index disclosed.

Analysis of disclosure of Islamic social finance information

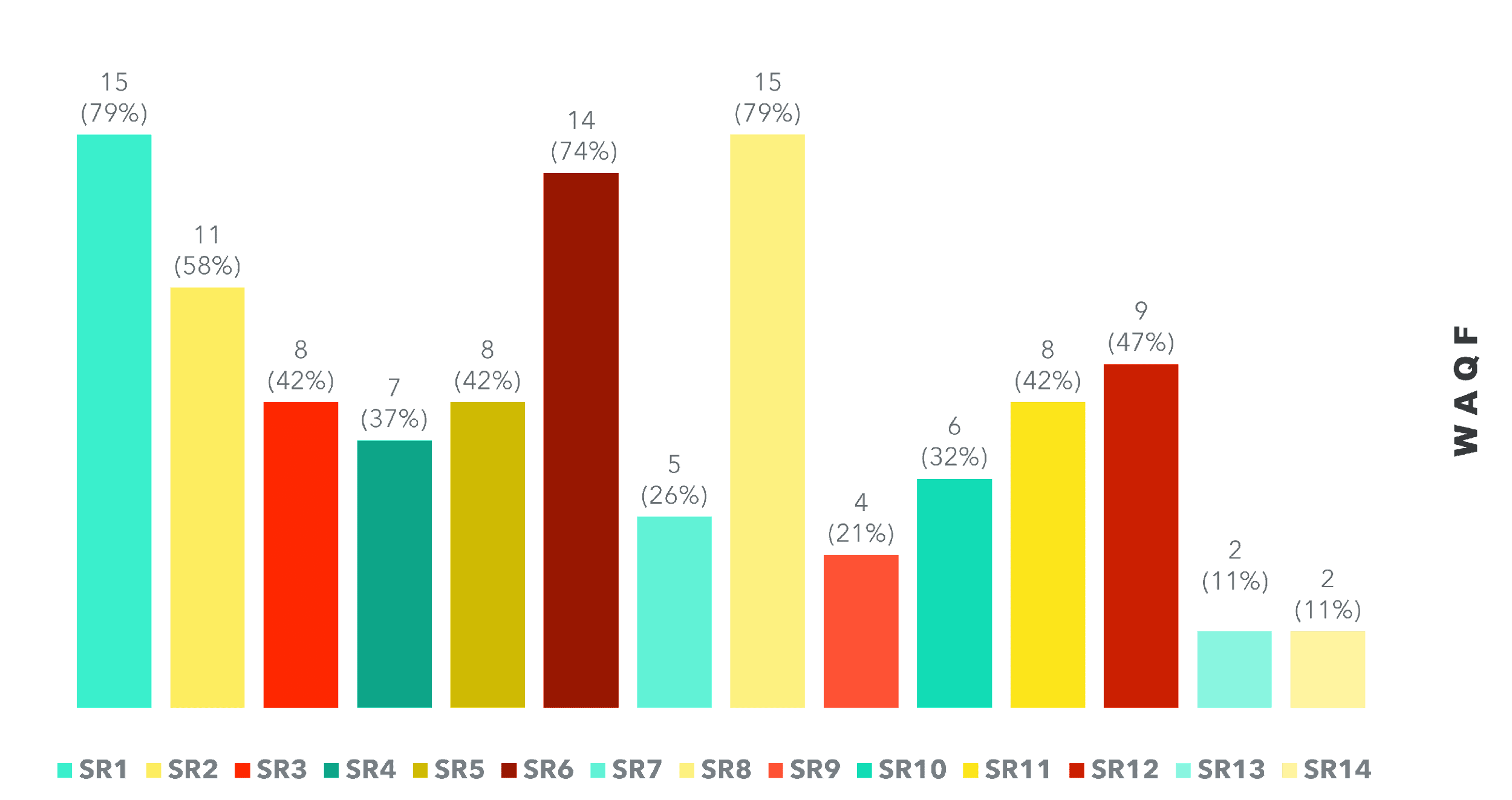

Figure 10 shows that both SR1 and SR8 have equally disclosed the most information on waqf among SIRCs with the highest score of 79% or 15 items of disclosure. In contrast, SR13 and SR14 reported the lowest score of 11% (2 items) on Islamic social finance disclosed. There are 19 items in the waqf information index, including any general waqf statements or policies and any mentions in the chairman's statement. The quality management system, waqf department, activities, and services, as well as stakeholder feedback on waqf concerns through forums and feedback channels, are all common waqf information that is given on websites. Information on finances, performance indicators, customer satisfaction metrics, productivity, efficiency, and effectiveness are also indexed in the waqf database.

Analysis of disclosure on Shariah-compliant statement

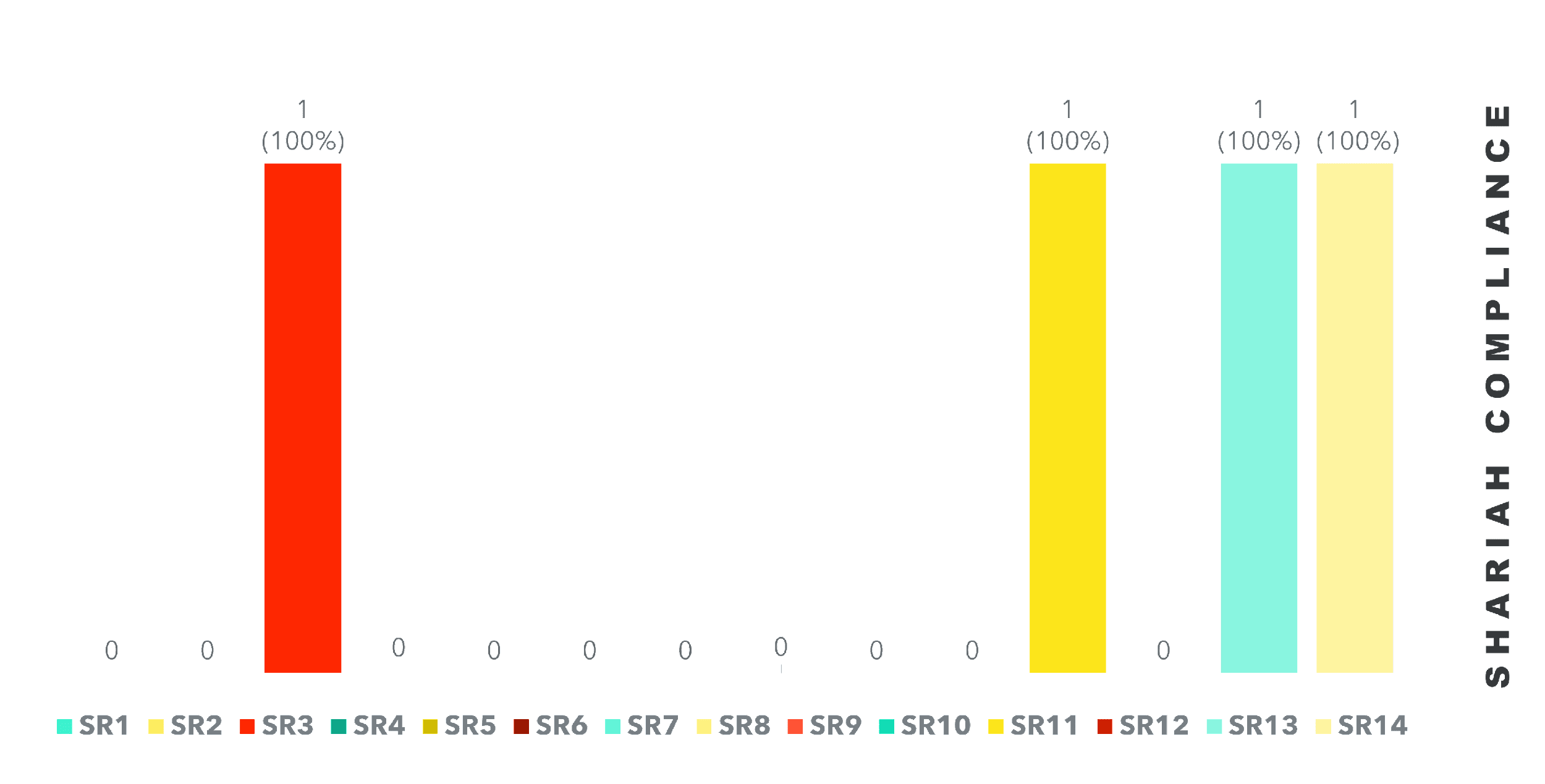

Despite the fact that Shariah law must be followed in all activities, records of transactions, risk mitigation, and other areas where SIRCs are recognized as religious institutions are required, this declaration is not made explicit on more than two-thirds (2/3) of the websites we looked at. As seen in Figure 11 above, only four SIRCs—SR3, SR11, SR13, and SR14—publicly pledged to uphold Shariah principles through a Shariah Compliance declaration on their website.

Analysis of disclosure of Environmental Information

Environmental-related information has been shown to be the least disclosed among SIRCs. Only one SIRC website—SR3—reported on an environmental topic, and that was in relation to the accolades they won for their 5S practice quality management system. This suggests that, despite the significance of the environment in accomplishing sustainability goals, the chosen SIRCs do not place a high priority on reporting environmental information.

Overall disclosure of SIRC on the Website

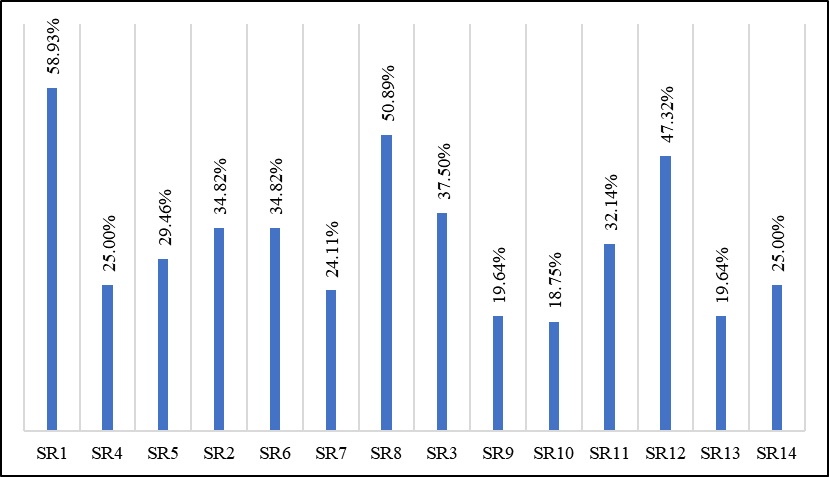

On average, the SIRCs disclosed only 33% of information regarding social (including sadaqah), economy/baitulmal, zakat, waqf, shariah compliant and environment in their websites or 37 items out of 112 items. Figure 12 revealed that SR1 disclosed the highest (58.9%) information on their websites followed by SR8 (50.89%) and SR12 (47.32%). Meanwhile, SR10 disclosed the least information on their websites with only 18.75%.

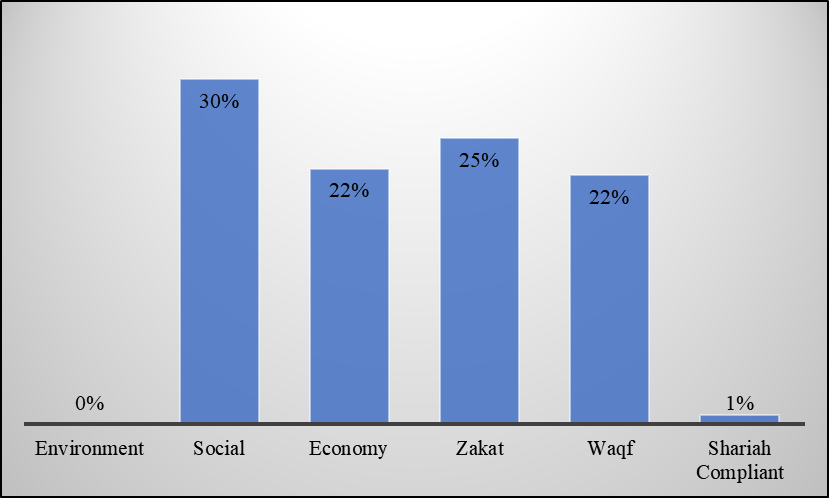

Figure 13 shows the percentage of website disclosure by themes. Social information (30%) was the highest information disclosed on the SIRCs websites, followed by zakat (25%) and economy and waqf (22%). Only 1% was reported regarding Shariah compliance and none for the environment.

In Malaysia, most of the SIRC’s websites are monitored by SPLaSK (Government Website and Online Service Monitoring System) to determine the level of availability of the agency's website and online services to ensure that the SIRC comply with the criteria set. Among the criteria set up by SPLaSK include quality of content (updated content, presence datasets, publication, understandable, accuracy), ease of use (quick link, search function, link to MyGov portal, find website using search tool, W3C disability accessibility), privacy/security (online service security), responsiveness (responsiveness to enquiries, feedback auto notification, feedback form), reliability (loading time, downtime), accessibility (browser compatibility, active link, device responsiveness, search engine optimisation) and web design (look and feel). (https://www.malaysia.gov.my/portal/content/30579?language=my)

The monitoring is conducted in real-time and continuously to ensure the SIRC and other government agencies can immediately improve their websites to support the national digital government transformation agenda. SPLaSK does not require SIRC to report activities related to the environment on the website. If SIRC does not report activities related to the environment, they can still get high reporting scores as long as they meet the criteria set by SPLaSK. Perhaps this is the reason why SIRC reported less on environmental-related activities on their website.

Conclusion

This study aims to examine the extent and quality of disclosure of SIRCs websites in communicating sustainability-related information to their stakeholders. A new SIRC sustainability-related web disclosure index has been developed in this study. The index is an adaptation of those used previously by Joseph (2010), Abu Bakar et al. (2020) and Masruki et al. (2016). The SIRC sustainability-related web disclosure index focuses on four (4) distinct sustainability elements: environmental, social, economic, zakat and waqf. Based on the study findings, it can be concluded that the SIRCs in Malaysia lack uniformity and consistency in disclosing sustainability-related information through their websites. There was a significant variation in the content and emphasis of sustainability disclosure across all four aspects of sustainability. In addition, only a few SIRCs reported on Shariah compliance on their website despite their status as the main Islamic religious bodies.

To address this issue, future work is required, which includes developing a standardised sustainability reporting framework specifically tailored to the needs of the SIRCs. This framework should provide clear guidelines for the disclosure of sustainability information, including specific metrics and indicators that should be disclosed. Additionally, the SIRCs should engage in capacity-building initiatives to improve their knowledge and understanding of sustainability reporting practices. This will enable them to communicate their sustainability performance to their stakeholders better and contribute to Malaysia's sustainable development agenda.

Acknowledgments

The authors would like to thank the Ministry of Higher Education Malaysia for funding the research project through the Fundamental Research Grant Scheme (FRGS/1/2021/SS01/UITM/02/41).

References

AAOIFI. (2019). Statement of Financial Accounting No. 1 on Conceptual Framework for Financial Reporting by Islamic Financial Institutions. https://www.aaoifi.com

Abdi, H., Kacem, H., & Omri, M. (2021). Web-based disclosure: Explanatory in the Mena Region. International Journal of Business and Management Review, 9(5) 49-77. https://www.eajournals.org/wp-content/uploads/Web-based-Disclosure.pdf

Abdillah, M. R., Anita, R., Hadiyati, & Zakaria, N. B. (2021). Trust in leaders and employee silence behaviour: Evidence from higher education institutions in Indonesia. Human Systems Management, 40(4), 567-580. DOI:

Abu Bakar, F., Derashid, C., Sawandi, N., Abdul Wahab, M. S., Ku Ismail, K. N. I., & Shaari, H. (2020). Financial Reporting and Disclosure Requirements for State Religious Councils. 4th UUM International Qualitative Research Conference 2020, 123-127.

Alsartawi, A., & Reyad, S. (2021). Shariah presentation and content dimensions of Web2.0 applications and the firms value of Islamic financial institutions in GCC countries. Journal of Islamic Marketing, 13(9), 1988-2005. DOI:

Baydoun, N., & Willett, R. (2000). Islamic Corporate Reports. Abacus, 36(1), 71-90. DOI:

Bilu, R., Abdul Aziz, A., & Darus, F. (2016). The influence of governance structure on sustainability disclosure: empirical evidence from Federal Statutory Bodies. Malaysian Accounting Review, 15(2), 11-33. https://mar.uitm.edu.my/images/Vol-15-2/01.pdf

Burgess, S., Bingley, S., & Parker, C. M. (2021). The value of local sporting clubs' websites. Information & Management, 58(8), 103531. DOI:

Carvalho, F., Santos, G., & Gonçalves, J. (2018). The disclosure of information on Sustainable Development on the corporate website of the certified Portuguese organizations. International Journal for Quality Research, 12(1) 253-276. http://ijqr.net/paper.php?id=670

Che Ku Kassim, C. K. H., Ahmad, S., Mohd Nasir, N. E., Wan Mohd Nori, W. M. N., & Mod Arifin, N. N. (2019). Environmental reporting by the Malaysian local governments. Meditari Accountancy Research, 27(4), 633-651. DOI:

Correia, E., Garrido, S., & Carvalho, H. (2021). Online sustainability information disclosure of mold companies. Corporate Communications: An International Journal, 26(3), 557-588. DOI:

Darus, F., Hamzah, E. A. C. K., & Yusoff, H. (2013). CSR Web Reporting: The Influence of Ownership Structure and Mimetic Isomorphism. Procedia Economics and Finance, 7, 236-242. DOI:

Farook, S. (2007). On Corporate Social Responsibility of Islamic Financial Institutions. Islamic Economic Studies, 15(1), 31-46. http://iesjournal.org/english/Docs/084.pdf

Gaia, S., & John Jones, M. (2017). UK local councils reporting of biodiversity values: a stakeholder perspective. Accounting, Auditing & Accountability Journal, 30(7), 1614-1638. DOI:

Global Reporting Initiative. (2004). Public Agency Sustainability Reporting a GRI Resource Document in Support of the Public Agency Sector Supplement Project. https://www.globalreporting.org

Global Reporting Initiative. (2021). Sustainability Reporting Guidelines. https://www.globalreporting.org

Hamid, N. H. A., Zakaria, N. B., & Aziz, N. H. A. (2014). Firms' Performance and Risk with the Presence of Sukuk Rating as Default Risk. Procedia - Social and Behavioral Sciences, 145, 181-188. DOI:

Ibrahim, S., Yusof, W. S., Handayani, W., Abu Samah, I. H., & Abd Rashid, I. M. (2022). Web-based accountability disclosure: Understanding performance and practices in the Malaysian States Government. Journal of Tianjin University Science and Technology, 55(4), 678-699. https://doi.org/

Jerry, M. S., Teru, P., & Musa, B. (2015). Environmental accounting disclosure practice of Nigerian quoted firms: A case study of some selected quoted consumer goods companies. Research journal of finance and Accounting, 6(22), 31-37. https://www.iiste.org/Journals/index.php/RJFA/ article/viewFile/26915/27598

Joseph, C. (2010). Content analysis of sustainability reporting on Malaysian local authority websites. The Journal of Administrative Science, 7(1), 101-125. https://www.researchgate.net/profile/Corina-Joseph/publication/265436111_Content_Analysis_of_Sustainability_Reporting_on_Malaysian_Local_Authority_Websites/links/540ef8bc0cf2d8daaacfe9e4/Content-Analysis-of-Sustainability-Reporting-on-Malaysian-Local-Authority-Websites.pdf

Joseph, C., Pilcher, R., & Taplin, R. (2014). Malaysian local government internet sustainability reporting. Pacific Accounting Review, 26(1/2), 75-93. DOI:

Lodhia, S. (2018). Is the medium the message?: Advancing the research agenda on the role of communication media in sustainability reporting. Meditari Accountancy Research, 26(1), 2-12. DOI:

Mahadi, R., Sariman, N. K., Noordin, R., Mail, R., & Fatah, N. S. A. (2018). Corporate Governance Structure of State Islamic Religious Councils in Malaysia. International Journal of Asian Social Science, 8(7), 388-395. DOI:

Masruki, R., Hussainey, K., & Aly, D. (2016). Expectations of Stakeholders on the Information Disclosure from the Malaysian State Islamic Religious Councils (SIRCs) Reporting. Global Review of Accounting and Finance, 7(2), 112-128. DOI:

Masruki, R., Hussainey, K., & Aly, D. (2018). Developing accountability disclosure index for malaysian state islamic religious councils (sircs): quantity and quality. Management and Accounting Review (MAR), 17(1), 1. DOI:

Masruki, R., Hussainey, K., & Aly, D. (2022). Stakeholder expectations of the accountability of Malaysian State Islamic Religious Councils (SIRCS): to whom and for what? Journal of Islamic Accounting and Business Research, 13(5), 760-777. DOI:

Meutia, I., Yaacob, Z., & Kartasari, S. F. (2021). Sustainability reporting: An overview of the recent development. Accounting and Financial Control, 3(1), 23-39. DOI:

Michener, G., Schuster, J., & Gerring, J. (2020). Digital Democracy and Political Change: Analyzing the Impact of the Internet on Governance and Politics. Perspectives on Politics, 18(1), 1-15. https://core.ac.uk/download/pdf/10653235.pdf

Midin, M., Joseph, C., & Mohamed, N. (2017). Promoting societal governance: Stakeholders' engagement disclosure on Malaysian local authorities' websites. Journal of Cleaner Production, 142, 1672-1683. DOI:

Mion, G., & Loza Adaui, C. R. (2019). Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability, 11(17), 4612. DOI:

Nair, R., Arshad, R., Muda, R., & Joharry, S. A. (2023). Web-disclosure practices for transparency and the sustainability of non-profit organisations. International Review on Public and Nonprofit Marketing, 20(1), 1-23. DOI:

Nicolò, G., Aversano, N., Sannino, G., & Tartaglia Polcini, P. (2021). Investigating Web-Based Sustainability Reporting in Italian Public Universities in the Era of Covid-19. Sustainability, 13(6), 3468. DOI:

Othman, M. H., Razali, R., & Nasrudin, M. F. (2020). Key factors for e-government towards sustainable development goals. International Journal of Advance Science and Technology, 29(6), 2864-2876. https://sersc.org/journals/index.php/IJAST/article/view/15798

Parker, L., & Gould, G. (1999). Changing public sector accountability: critiquing new directions. Accounting Forum, 23(2), 109-135. DOI:

Rainie, L., Anderson, J., & Perrin, A. (2021). Americans' attitudes about government information resources and data privacy. Pew Research Center. https://www.pewresearch.org/internet/2021/03/26/americans-attitudes-about-government-information-resources-and-data-privacy/

Ramli, N., & Kamaruddin, M. (2017). Disclosure of web-based accountability: Evidence from Zakat Institutions in Malaysia. 5th South East Asia International Islamic Philanthropy Conference, 2017 (5th SEAIIPC2017), 14-16 February 2017.

Saxton, G. D., & Guo, C. (2011). Accountability Online: Understanding the Web-Based Accountability Practices of Nonprofit Organizations. Nonprofit and Voluntary Sector Quarterly, 40(2), 270–295. DOI:

Selahudin, N. F., Zakaria, N. B., Sanusi, Z. M., & Budsaratragoon, P. (2014). Monitoring Financial Risk Ratios and Earnings Management: Evidence from Malaysia and Thailand. Procedia - Social and Behavioral Sciences, 145, 51-60. DOI:

Utama, A. A. G. S. (2020). The implementation of e-government in indonesia. International Journal of Research in Business and Social Science (2147- 4478), 9(7), 190-196. DOI:

Yusof, N. (2016). The Credibility of Islamic Religious Institutional Websites in Malaysia. Jurnal Komunikasi, Malaysian Journal of Communication, 32(2), 82-104. DOI:

Zain, S. R. M., Yaacob, N. M., Jusoh, R., & Taib, A. (2014). Financial Reporting Disclosure on Annual Reports of State Islamic Religious Councils in Malaysia. Journal of Applied Environmental and Biological Sciences, 4(6), 8-13.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

15 November 2023

Article Doi

eBook ISBN

978-1-80296-130-0

Publisher

European Publisher

Volume

131

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1281

Subjects

Technology advancement, humanities, management, sustainability, business

Cite this article as:

Minhad, S. F. N., Ahmad, K., Abdullah, Z., Kasim, E. S., Ali, N. A. M., & Nawawi, N. H. A. (2023). Web-Based Sustainability Reporting: Evidence From State Islamic Religious Councils in Malaysia. In J. Said, D. Daud, N. Erum, N. B. Zakaria, S. Zolkaflil, & N. Yahya (Eds.), Building a Sustainable Future: Fostering Synergy Between Technology, Business and Humanity, vol 131. European Proceedings of Social and Behavioural Sciences (pp. 11-28). European Publisher. https://doi.org/10.15405/epsbs.2023.11.2