The Influence of Human Governance Towards Sustainable Supply Chain Management Disclosure

Abstract

The traditional development mode for social and economic progress has resulted in crises and challenges; therefore, various countries have begun to actively explore sustainable development, especially in supply chain management. However, sustainable supply chain management disclosure practice is limited to reach. The purpose of this paper is to explore the relationship between human governance and sustainable supply chain management disclosure using Scopus, Web of Science, and Google Scholar as the main databases. The findings of this paper discovered three main themes namely 1) sustainable supply chain management disclosure; 2) human governance; and 3) board characteristics. In order to eventually achieve successful human governance, it is strongly advocated that companies have valuable directors on board to apply Sustainable Supply Chain Management disclosure as a tool for identifying and controlling sustainable supply chain management. The study includes different recommendations for policymakers, the government, and accounting professional organizations, as well as recommendations for future research.

Keywords: Board Characteristics, Human Governance, Sustainable Supply Chain Management Disclosure

Introduction

The Sustainable Development Goals (SDGs) were established in order to promote societal prosperity and environmental protection. As a result, organizations must have a consistent, relevant, and credible method for reporting on their sustainability supply chains (Said et al., 2020). SDGs are a set of 17 objectives, and goal number 12 in particular (ensure sustainable consumption and production patterns) encourages businesses to incorporate sustainable practices into all aspects of their operations. The company's best strategy for achieving the intended result and complying with SDG12 is Sustainable Supply Chain Management (SSCM) disclosure. Companies are able to participate in the SDGs by incorporating SSCM transparency into their regular operations. The practice of SSCM disclosure in annual reports is extremely sought-after, particularly for huge companies with comprehensive supply chains that reach over the management of suppliers, natural resource management, the handling of solid waste, transportation management, and customer relationship management without ignoring sustainability regardless of stage. The public and its stakeholders are putting pressure on manufacturers to accept accountability for the environmental effects of their internal and supplier activities (Koberg & Longoni, 2019). The triple bottom line of sustainability, which incorporates social, environmental, and economic considerations, can be considered when planning for a company's revenue growth (Shekarian et al., 2022). On top of that, experts have been appreciative of reforming business set-ups as a result of the fluctuations triggered by the community's growing facts of the eco-friendly jeopardies posed by productions. Over a long time period, such operations have been the main causes of a lot of waste, both solid and liquid, degradation of water and the atmosphere, rising temperatures, and a decrease in the number of resources that are not renewable and important minerals (Shekarian et al., 2022).

The task should come as no surprise that SSCM disclosure requires a certain level of competence and skill, specifically from accountancy and management leaders to disclose each supply chain activity consistent with sustainable goals. For truly thorough SSCM disclosure in annual reports, practitioners are in need of a framework that serves as a guide. Stakeholders will be able to assess a company's supply chain management performance effectively if the information is properly disclosed by the company (Said et al., 2020). Numerous studies have shown the value of SSCM disclosure in promoting informed decision-making and improving the performance of the five pillars of sustainability (Fritz, 2019; Said et al., 2020; Strohmandl & Čujan, 2019; Truong et al., 2017; Yu et al., 2022). Fritz (2019) suggested the example of reverse logistics, concentrating on how to lessen the environmental effects of supply chains by capturing the reverse flows of products, as one of the key SSCM concepts. Moreover, Marshall et al. (2016) stated that the directors of the company need to be aware of the various causes and people influencing and enabling in order to know how to strategically manage public information regarding supply chain disclosure. This demonstrates that SSCM disclosure is still in its infancy and that, except from Said et al., (2020)'s outline of 60 elements that essentially be included in the annual report for SSCM disclosure, no study has yet been done to define the framework of SSCM disclosure. Stakeholders are putting more pressure on supply chains to adopt a wide range of corporate responsibility and sustainability practices in the business practices of their constituents (Sabat & Krishnamoorthy, 2020).

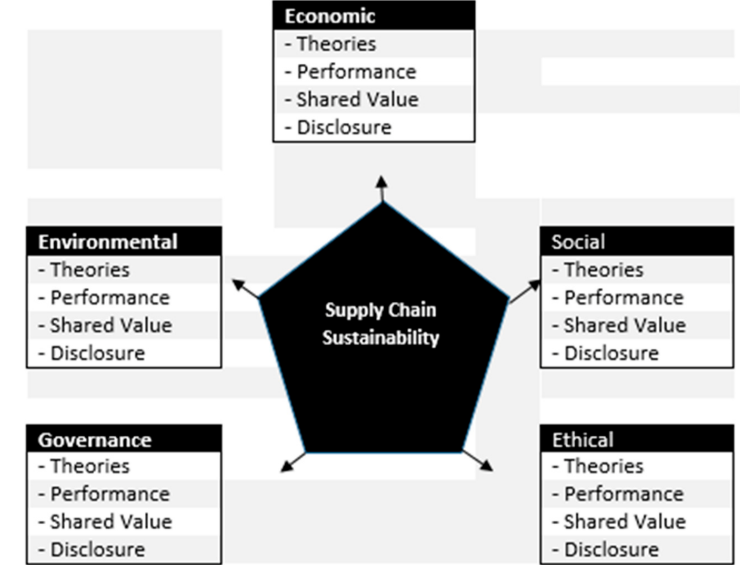

The components that must exist for an organization to adopt sustainability in the supply chain are shown in Figure 1. With regard to the reason for developing shared value for all stakeholders, the sustainability of companies facilitates the combination of both financial economic sustainability performance and non-financial environmental, social, ethical, and governance sustainability performance facets (Rezaee, 2018). Figure 1 indicates that all pillars of supply chain sustainability should have theories, performance, shared value, and disclosure. From the five pillars in the figure, the study chose governance (human governance) in the disclosure of SSCM. Therefore, this study aims to fill the gap in the factors that influence corporate disclosure (particularly SSCM disclosure) by using a systematic literature review to look at how human governance affects the level of SSCM disclosure globally. The subsequent research question developed out of this.

RQ: Does human governance act as a strong determinant towards SSCM disclosure?

Human governance is the development of impacting human behavior by means of internal and value-based beliefs. To stand in trust, it highlights principles, morals, and cultural and ethical norms (Hanapiyah et al., 2016). The idea that certain human goals transcend human-made laws and regulations is incorporated into human governance. The requirements that directors must meet include awareness, morals, and values, and as a result, they are capable of making wise decisions on corporate disclosure, particularly SSCM disclosure.

Material and methods

Identification

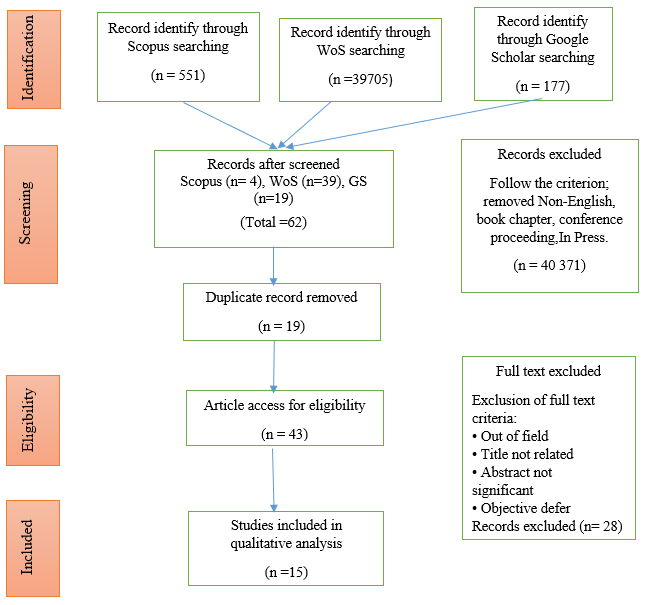

Three fundamental stages of the systematic review procedure were employed to choose a large number of pertinent papers for this investigation. In the first stage, keywords are chosen, and related terms are sought to utilize thesaurus, dictionaries, encyclopedias, and previous research. Search strings have been created for the Scopus, Web of Science, and Google Scholar databases after all relevant terms have been chosen (see Table 1). The first stage of the systematic review approach for the current study resulted in the successful retrieval of 40,433 papers from three databases.

Screening

The collection of possibly relevant research articles is screened to ensure that its content relates to the stated research question. One illustration of a content-related criterion that is frequently used in the screening phase is the selection of research topics based on the disclosure of the relationship between human governance and sustainable supply chain management. The list of documents to be searched in this stage will be purged of any duplicate papers. In the first step of screening, 40,371 publications were rejected, and 62 papers were evaluated in the second stage using different exclusion and inclusion criteria for this study (see Table 2). The primary source of beneficial knowledge in the literature (research articles), served as the first criterion. Reviews, meta-synthesis, meta-analyses, monographs, book series, chapters, and conference proceedings are also excluded from the most recent study. Additionally, only English-language articles were included in the review. It is crucial to keep in mind that human governance and SSCM disclosure were given top priority in the strategy from 2016 to 2022. The timeframe for these five years was chosen due to the latest research pertaining to human governance and corporate disclosure. This historical period is used to support more recent reviews. Nineteen publications in all were ignored because of duplicate concerns.

Eligibility

There are a total of 43 articles accessible at the third level, called eligibility. At this point, all article titles and significant texts were thoroughly scrutinized to ensure that they met the criteria for inclusion and complemented the goals of the current study. As a result, twenty-eight publications were disregarded because they failed to underline the main purpose of the study, which was backed by empirical evidence. There are a total of 15 papers available for review.

A recognized standard for doing a systematic literature review is PRISMA, or Preferred Reporting Items for Systematic Reviews and Meta-Analyses (Mohamed Shaffril et al., 2019). In general, publication standards are crucial to providing authors with the pertinent and important knowledge they need to assess and look into the caliber and rigor of a review. Additionally, PRISMA places a strong emphasis on reviews that assess randomized trials since they can serve as the foundation for publishing systematic reviews of other types of research (Moher et al., 2009). Figure 2 shows the flow diagram of the proposed search study as indicated by Moher et al. (2009).

Data Abstraction and Analysis

Results and Findings

Only 1 of the 15 articles that were discovered created a new index for SSCM disclosure; five publications discussed SSCM. While ten publications addressed the urgency of human governance in corporations, they made no connection involving HG and SSCM disclosure, but with other corporate disclosure or reporting such as sustainable reporting, corporate social responsibilities (CSR) disclosure, management commentary disclosure, voluntary disclosure, and environment, social and governance (ESG) disclosure.

Discussions

Sustainable Supply Chain Management Disclosure

Sustainability in the supply chain refers to the control of the effects on the environment, society, and the economy as well as the promotion of ethical behaviour in public life (Kusrini & Primadasa, 2018). After being first used in the late 1980s, the term "supply chain management (SCM)" ended up being well-known in the 1990s. The terms ``logistics" and "operations management" had been utilized by businesses prior to that (Hugos, 2018). With respect to the product or service, industries, and business models of companies, Supply Chain Management is the overseeing of products or services from the initial design stage to the various production stages beginning with the extraction of raw materials and concluding with the completion of the delivery of the product/service to the final customer (Fritz, 2019). Hugos (2018) added that SCM is the particular, systematic direction of old-style corporate operations and methods across productions in the supply chain and in the bounds of one specific business by means of the aim of improving the future viability of particular companies and the supply chain altogether. To recognize and handle the frequent responsibilities required to form the undertaking of goods and services in a way that optimally satisfies the end users, SCM customs an arrangements method. Supply chain partners must simultaneously increase their operational effectiveness and quality of service to qualify for SCM to be operative. It is advised that supply chain management take environmentally friendly practices into consideration while extending the concept of sustainability to activities related to production and consumption.

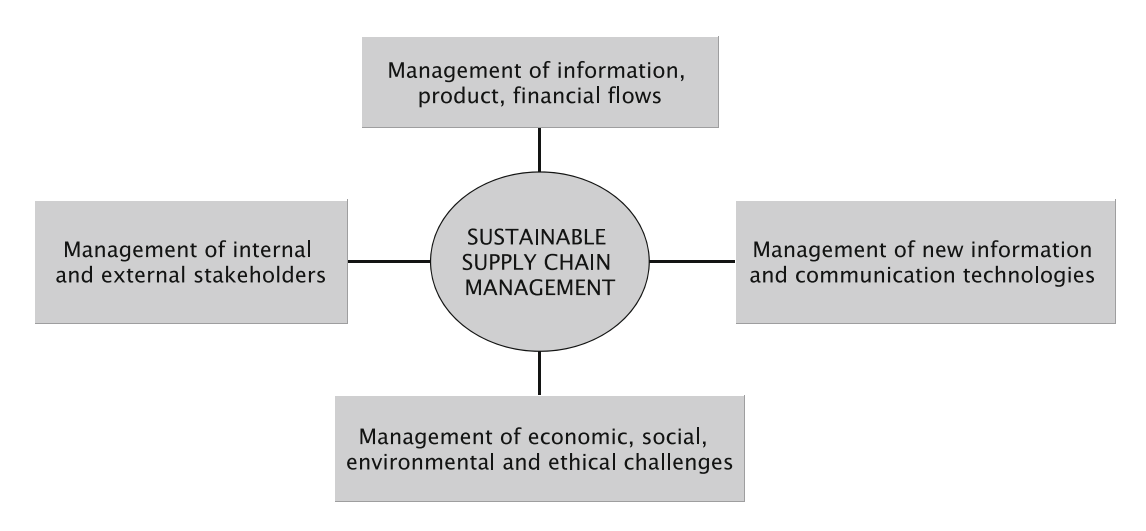

Figure 3 demonstrates the SSCM framework proposed by Fritz (2019). The framework suggests that SSCM should comprise management of information regarding products, financial flows, communication technologies, management of pillars of sustainability (economic, social, environmental, and ethical), and management of all stakeholders.

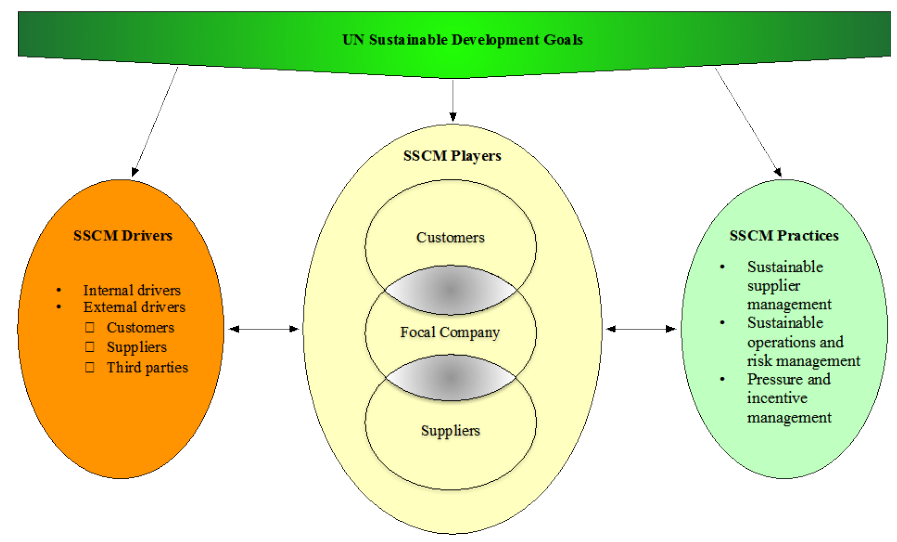

Meanwhile, Zimon et al. (2020) also developed a suggested framework for the implementation of sustainable supply chains as shown in Figure 4. Leaders who are effective, qualified, and capable of making efficient decisions are needed to oversee all aspects (Amin et al., 2019) according to the framework.

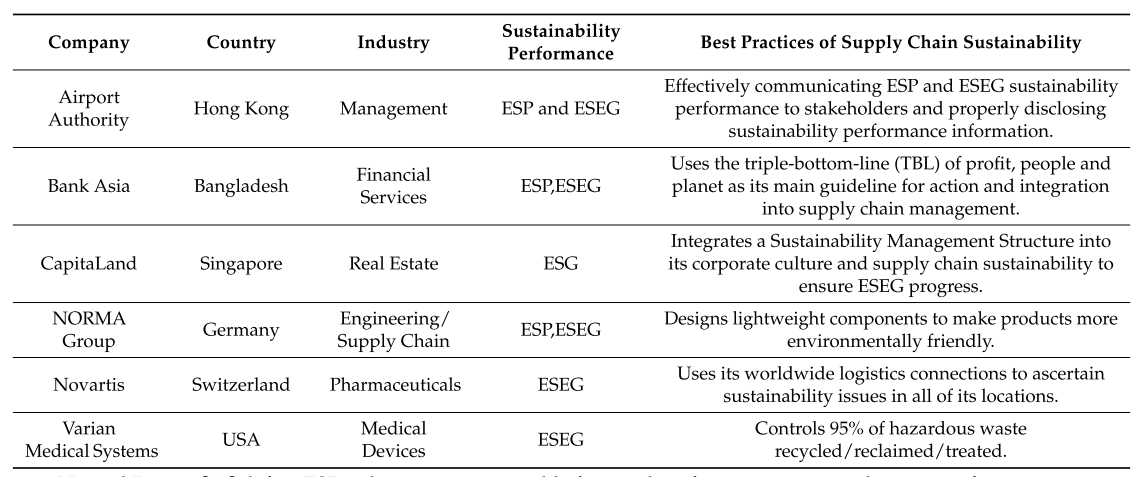

The sustainability performance and worldwide supply chain sustainability benchmarks are presented in Figure 5.

Global Reporting Initiatives (GRI) suggested the company explore the sustainable context in order to identify and describe its material themes (GRI 3: Material themes 2021). The GRI Sector Standards make available a viewpoint for each division and are able to assist a company in having a handle on its sustainability viewpoint. The GRI's essential ideologies and content mechanisms, along with previous studies for example Said et al. (2020), aid the company to generate the finest SSCM for its annual report. The SSCM develops an apparent goal, specifically to undertake a system that expands certainty and builds it conceivable to implicitly appraise and reveal the significance of a business to stakeholders who signify the economy, society, and environment.

There are abundant benefits when integrating SSCM disclosure in annual reports for a corporation. The value of sustainable supply chain management will only become apparent if it contributes to the improvement of strategic management and acknowledges its importance to consumer needs. The emphasis on numerous significant SSCM benefits has given companies recent chances to contend in the worldwide marketplace (Chaopaisarn & Woschank, 2019). SSCM represents one of the aforementioned benefits since it serves businesses and the people and organizations along the supply chain. Furthermore, exercising social and environmental awareness is crucial for sustainability (Rouse & Piro, 2021). Which includes ensuring product safety, employee welfare, environmental protection, resource efficiency, and superior quality. According to Rouse and Piro (2021), businesses can make a return by means of costs that can be lessened by applying sustainable procedures in the supply chains. Companies' performance is well controlled if risks are well managed (Hamid et al., 2014), hence lowering and avoiding risks, developing appropriate company policies, enhancing innovation and openness, maintaining higher standards in the company's sector, and collaboratively generating values are some of the benefits of SSCM that Chowdhury et al. (2023) previously investigated.

Human Governance

Human Governance (HG) refers to the governors' dedication to enhancing workers' morals and ethical conduct at work. Humans are an important capital asset and a major factor in the success of businesses. According to Abdullah and Said (2018), the implementation of human governance should be designated in management over other kinds of governance because it is connected to ethical conduct in the workplace. In contrast to corporate governance (CG), which focuses on processes, policies, and other factors, HG places a greater emphasis on and close relationship with employees by instilling quality values through ethics, moral conduct, and behavior (Abdullah & Said, 2018). Relationships that are beneficial to the business may result from human governance (Haron et al., 2022). The subject can be used to concentrate on the failure of CG or as a category of corporate control. According to Hanapiyah et al. (2016), corporate governance focuses on external rules designed to regulate how the corporation conducts business. Consequently, HG must enhance CG to succeed, especially in terms of humanity. Previous studies have employed HG to discover corporate reporting, corporate performance, and corporate disclosure (Abdullah & Said, 2018; Amin, 2018; Haron et al., 2022; Kumar, 2019; Said et al., 2018).

Headship, truthfulness, religiousness, belief, philosophy, training and expansion, employment and assessment, and domestic policy regulation are the eight components of human governance that Exploratory Factor Analysis (EFA) has discovered (Hanapiyah et al., 2016). In contrast, Said et al. (2018) proved human governance through the education of the board. In order to promote a culture based on trust where people within the organization are considered as the organization's soul, human governance considers the axiology, encompassing the traits of values, religion, belief systems, culture, and ethics (Hanapiyah et al., 2016). Human governance is a religiously oriented kind of government that directs the leaders' behaviour, way of thinking, and perception of the natural world. Decisions affecting the efficient preservation of the supply chain management will significantly benefit all parties as a result of the critical thinking of high-quality human governance. All parties involved will always be included, and their rights will be upheld. Hanapiyah et al. (2016) identified that HG potentially helps the firm's director in providing value and being able to maximize company value since a successful company comes from a valued individual who has high ethics and integrity. The upper echelons theory contends that top executives have distinct cognitive underpinnings and demographic traits that have an impact on how they interpret and make valuable decisions (Thambugala & Rathwatta, 2021). The policies and decisions made by a corporation are influenced by these traits of top management.

The director's qualities and personality have a major influence on the company's ability to effectively utilize SSCM disclosure (Franco-García et al., 2019; Sabat & Krishnamoorthy, 2020). The smooth operation of supply chain management in a sustainable direction that satisfies the needs of the three main factors in SSCM disclosure, particularly with regard to the environment, economy, and society, depends on the nature of the personality of the manager when selecting strategies concerning company activities, particularly those related to the supply chain. The effectiveness of the supply chain for the end user is susceptible to compromise by improper supply chain activities such invoicing manipulation, wrongly set prices, and subpar product quality.

Human Governance and SSCM Disclosure

Past research on the issue of HG and SSCM disclosure was scarce. However, the study seemed to favor the connection between HG and corporate reporting. The results of those investigations show a strong connection between HG and sustainability reporting (So et al., 2021); no relationship between human governance and management commentary disclosure (Said et al., 2018); the HG Index for Shariah-compliant businesses was favourable and highly correlated with sustainability reporting (Haron et al., 2022). According to Haron et al., (2022), there needs to be a robust HG structure in place in order to improve the sustainability reporting of companies that adhere to Islamic Concept. Moreover, Thambugala and Rathwatta (2021) pointed out that directors with a variety of educational and professional backgrounds as well as those with extensive industry experience are also more concerned with CSR and urged real CSR practice. The expertise of the board of directors will improve the decision-making process.

The decision-making process is crucial since it affects the business's operations. Investors in particular are very interested in learning whether the money they have invested is being used profitably. They are looking for human governance, which is a crucial component that may direct how businesses create value in the new economy. It will be essential for businesses to incorporate HG since it is a component of CG mechanisms that represents the background and features of the board and would result in the establishment of SSCM disclosure. Additionally, there is an advantageous relationship between HG characteristics and the performance of the SSCM. An earlier study focused on the director's role in personally planning and developing every supply chain action to be more sustainable. For the organization to apply SSCM, the director's personality and character have a major impact (Franco-García et al., 2019; Sabat & Krishnamoorthy, 2020).

Board Characteristics

Values, opinions, and character traits can influence a person's decision-making. The systematic investigation considers the board's characteristics, such as age, in determining how companies should be conducted including disclosing the company’s information. Older directors are perceived as having more knowledge, better judgment, more straightforward beliefs, and a conventional approach to business. Ismail and Latiff (2019) explored how board diversity affects a company's sustainability practices. Aspects of the board age are examined to determine how they impact the company's sustainable practices. The information collected covers the ESG Scores of 38 Malaysian PLCs from 2010 to 2016, and the results showed a strong correlation between board age and sustainable business practices. Nevertheless, it has been discovered that board age diversity is strongly and negatively correlated with high-quality CSR disclosure (Khan et al., 2019) board age negatively weakens the CSR (Fahad & Rahman, 2020), and the age of the board variables did not present statistical significance towards voluntary disclosures (Bueno et al., 2018).

The measurement of board age by Fahad and Rahman (2020) is the average age of directors of the company (Ismail & Latiff, 2019), while Bueno et al. (2018) measured board age as a range of an average of 50 years. The average age of the board members can be used to gauge the company expertise of the board of directors members; a board with more experienced directors has a higher average age than one with more inexperienced directors. The age of corporate directors' decision-making maturity is viewed as being crucial to the company's vulnerability in SSCM. Companies need competent directors to sustain long-term survival, particularly with the aging of the baby boomer population. When considering sustainable practices, such as corporate disclosure and reporting, board age is not a significant determinant, according to the findings of previous studies. To construct and create a thorough SSCM disclosure, analytical and creative thinking is required from directors regardless of their age.

Conclusion and Future Research Recommendation

This study uses Scopus, Web of Science, and Google Scholar as its primary databases to investigate the connection between human governance and SSCM disclosure. Three key topics were identified by this study's findings: 1) sustainable supply chain management disclosure; 2) human governance; and 3) board characteristics. In this review, board age acts as a human governance characteristic that can be a factor in corporate reporting and corporate disclosure, particularly SSCM disclosure. It is strongly encouraged for companies to have experienced directors who have relevant and important perspectives on the sustainability of the company and who incorporate SSCM disclosures as one of the ways to accomplish SDGs.

More human governance traits should be considered in future studies as a major factor regulating SSCM disclosure. Human governance that is effective can benefit stakeholders through SSCM disclosure. A company is more likely to have a thorough understanding of sustainable supply chain management and be better able to disclose it to stakeholders when it has robust governance mechanisms in place. This can lessen the chance of unfavorable consequences, including lawsuits, reputational damage, and financial losses, as well as promote openness and stakeholders’ confidence.

Acknowledgment

The authors thank the Accounting Research Institute, (ARI- HICoE), Universiti Teknologi MARA, Shah Alam, Malaysia, and the Ministry of Higher Education for funding research.

References

Abdullah, W. N., & Said, R. (2018). The Influence of Corporate Governance and Human Governance towards Corporate Financial Crime: A Conceptual Paper. Developments in Corporate Governance and Responsibility, 193-215. DOI:

Amin, B., Hakimah, Y., Madjir, S., & Noviantoro, D. (2019). The role of transformation leadership in enhancing corporate sustainability capabilities and sustainable supply chain management. Polish Journal of Management Studies, 20(2), 83–92. DOI:

Amin, H. (2018). Why human governance is needed. https://www.nst.com.my/opinion/letters/2018/02/336834/why-human-governance-needed

Bueno, G., Marcon, R., Pruner-da-Silva, A. L., & Ribeirete, F. (2018). The role of the board in voluntary disclosure. Corporate Governance: The International Journal of Business in Society, 18(5), 886-910. DOI:

Chaopaisarn, P., & Woschank, M. (2019). Requirement analysis for SMART supply chain management for SMEs. Proceedings of the International Conference on Industrial Engineering and Operations Management, 2019(MAR), 3715–3725.

Chowdhury, S., Rodriguez-Espindola, O., Dey, P., & Budhwar, P. (2023). Blockchain technology adoption for managing risks in operations and supply chain management: evidence from the UK. Annals of Operations Research, 327(1), 539-574. DOI:

Fahad, P., & Rahman, P. M. (2020). Impact of corporate governance on CSR disclosure. International Journal of Disclosure and Governance, 17(2-3), 155-167. DOI:

Franco-García, M.-L., Carpio-Aguilar, J. C., & Bressers, H. (2019). The Future of Circular Economy and Zero Waste. Greening of Industry Networks Studies, 265-273. DOI:

Fritz, M. M. C. (2019). Sustainable Supply Chain Management. Encyclopedia of the UN Sustainable Development Goals, 1-14. DOI:

Hamid, N. H. A., Zakaria, N. B., & Aziz, N. H. A. (2014). Firms' Performance and Risk with the Presence of Sukuk Rating as Default Risk. Procedia - Social and Behavioral Sciences, 145, 181-188. DOI:

Hanapiyah, Z. M., Daud, S., & Wan Abdullah, W. M. T. (2016). Institutionalising Human Governance Determinant: Steering Organizations towards Sustainability. IOP Conference Series: Earth and Environmental Science, 32, 012056. DOI:

Haron, H., Jamil, N. N., Ramli, N. M., Aziz, S. A., Sulaiman, S., Gautama, I., Gui, A., Sari, S. A., Nurul 'Athirah Rosli, & Nurul Kamarina Kamarudin. (2022). Human Governance Index of Manufacturing Sector of Shariah Compliant Companies in Malaysia: A Preliminary Analysis. Journal of Governance and Integrity, 5(2), 283-296. DOI:

Hugos, M. (2018). Key Concepts of Supply Chain Management. In Essentials of Supply Chain Management (Issue March 2018). DOI:

Ismail, A. M., & Latiff, I. H. M. (2019). Board Diversity and Corporate Sustainability Practices: Evidence on Environmental, Social and Governance (ESG) Reporting. International Journal of Financial Research, 10(3), 31. DOI:

Khan, I., Khan, I., & Senturk, I. (2019). Board diversity and quality of CSR disclosure: evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 19(6), 1187-1203. DOI:

Koberg, E., & Longoni, A. (2019). A systematic review of sustainable supply chain management in global supply chains. Journal of Cleaner Production, 207, 1084-1098. DOI:

Kumar, P. C. (2019). Human governance is key to better corporate integrity | The Star. https://www.thestar.com.my/business/business-news/2019/02/09/human-governance-is-key-to-better-corporate-integrity

Kusrini, E., & Primadasa, R. (2018). Design of Key Performance Indicators (KPI) for Sustainable Supply Chain Management (SSCM) Palm Oil Industry in Indonesia. MATEC Web of Conferences, 159, 02068. DOI:

Marshall, D., McCarthy, L., McGrath, P., & Harrigan, F. (2016). What's your strategy for supply chain disclosure? MIT Sloan Management Review.

Mohamed Shaffril, H. A., Samah, A. A., Samsuddin, S. F., & Ali, Z. (2019). Mirror-mirror on the wall, what climate change adaptation strategies are practiced by the Asian's fishermen of all? Journal of Cleaner Production, 232, 104-117. DOI:

Moher, D., Liberati, A., Tetzlaff, J., Altman, D. G., & PRISMA Group. (2009). Preferred reporting items for systematic reviews and meta-analyses: the PRISMA statement. Annals of Internal Medicine, 151(4), 264-269. DOI:

Rezaee, Z. (2018). Supply Chain Management and Business Sustainability Synergy: A Theoretical and Integrated Perspective. Sustainability, 10(2), 275. DOI:

Rouse, D., & Piro, R. (2021). The Comprehensive Plan. DOI:

Sabat, K. C., & Krishnamoorthy, B. (2020). Sustainable supply chain management practices and their mediation effect on economic returns. Corporate Governance and Sustainability Review, 4(1), 8-20. DOI:

Said, R., Joseph, C., Rahmat, M., Abdullah, W. N., Radjeman, L. A., Hotrawaisaya, C., & Moryadee, C. (2020). Development of supply chain management sustainability index (SCMsi). International Journal of Supply Chain Management, 9(1), 902–907.

Said, R., Abdul Rahim, A. A., & Hassan, R. (2018). Exploring the effects of corporate governance and human governance on management commentary disclosure. Social Responsibility Journal, 14(4), 843-858. DOI:

Shekarian, E., Ijadi, B., Zare, A., & Majava, J. (2022). Sustainable Supply Chain Management: A Comprehensive Systematic Review of Industrial Practices. Sustainability, 14(13), 7892. DOI:

So, I. G., Haron, H., Gui, A., Princes, E., & Sari, S. A. (2021). Sustainability Reporting Disclosure in Islamic Corporates: Do Human Governance, Corporate Governance, and IT Usage Matter? Sustainability, 13(23), 13023. DOI:

Strohmandl, J., & Čujan, Z. (2019). Risk Minimisation in Integrated Supply Chains. Open Engineering, 9(1), 593-599. DOI:

Thambugala, T., & Rathwatta, H. (2021). Board characteristics and corporate social responsibility practices: in upper echelon theory perspective evidence from Sri Lankan Firms. International Journal of Accounting and Business Finance, 7(1), 140. DOI:

Truong, H. Q., Sameiro, M., Fernandes, A. C., Sampaio, P., Duong, B. A. T., Duong, H. H., & Vilhenac, E. (2017). Supply chain management practices and firms' operational performance. International Journal of Quality & Reliability Management, 34(2), 176-193. DOI:

Yu, Z., Waqas, M., Tabish, M., Tanveer, M., Haq, I. U., & Khan, S. A. R. (2022). Sustainable supply chain management and green technologies: a bibliometric review of the literature. Environmental Science and Pollution Research, 29(39), 58454-58470. DOI:

Zimon, D., Tyan, J., & Sroufe, R. (2020). Drivers of Sustainable Supply Chain Management: Practices to Alignment with Un Sustainable Development Goals Journal of Sustainable Development of Transport and Logistics View project Integrated Management View project Drivers of Sustainable Supply Chain. International Journal for Quality Research, 14(1), 219–236. DOI:

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

15 November 2023

Article Doi

eBook ISBN

978-1-80296-130-0

Publisher

European Publisher

Volume

131

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1281

Subjects

Technology advancement, humanities, management, sustainability, business

Cite this article as:

Adenan, N. Z. C., Said, R., & Joseph, C. (2023). The Influence of Human Governance Towards Sustainable Supply Chain Management Disclosure. In J. Said, D. Daud, N. Erum, N. B. Zakaria, S. Zolkaflil, & N. Yahya (Eds.), Building a Sustainable Future: Fostering Synergy Between Technology, Business and Humanity, vol 131. European Proceedings of Social and Behavioural Sciences (pp. 237-249). European Publisher. https://doi.org/10.15405/epsbs.2023.11.19