Forecasting As Method Of Internal Control Of Production Activities In Agricultural Organizations

Abstract

In modern conditions, the economic efficiency of internal control of production activities in agricultural organizations is determined by the reliability of the reflection of the information obtained during the control and the assessment of the prospects for the further functioning of the organization on the basis of analysis and forecasting. The article discusses the features of forecasting as a method of internal control of the production activities of agricultural organizations, aimed at determining the main indicators of their production activities, reflecting the relationships and patterns of development based on a detailed analysis of market conditions and changes in them for the coming period. The authors’ definition of the concept of “forecasting” is given, which is interpreted as a specific method of internal control, focused on determining the main indicators of the production activity of an agricultural organization taking into account market conditions. The role and place of forecasting in the system of internal control of production activities of agricultural organizations are determined due to the close unity of specific tasks and directions of control actions. An economic and mathematical model based on the definition of guaranteed production in the crop growing industry and focused on obtaining the maximum amount of revenue is proposed. The goals of forecasting the production activity of agricultural organizations are substantiated, depending on which various economic and mathematical models differing in the degree of aggregation of the indicators included in the model can be used.

Keywords: Agricultural organizations, efficiency, forecasting, internal control, production activities

Introduction

The final results of production activities mainly depend on the rational use of resources, compliance with agrotechnical and veterinary requirements, the degree of implementation of sowing plans, crop yields, animal productivity and finished product yield. In this regard, the competent organization of internal control of production activities gains particular importance.

Problem Statement

Internal control of production activities allows monitoring the progress of planned targets, preventing resource overruns and identifying unused reserves.

The effectiveness of internal control of production activities in agricultural organizations largely depends on how reliably the features of the further development of an agricultural organization are reflected and an objective assessment of further prospects for functioning is carried out based on an analysis of market conditions and changes in them.

In this regard, particular importance is given to forecasting the production activities of agricultural organizations. The economic essence of production forecasting lies in increasing the efficiency of resource use and lies in the most complete and rational use of resource potential, the purpose of which is to create a situation in which a large number of high quality products are produced with the condition of minimizing various costs used in the manufacture of a unit of the product.

Research Questions

The questions to which this work is devoted directly follow from the hypothesis of the study, which is that the effectiveness of the functioning of agricultural organizations depends on the competent organization of internal control of production activities using the forecasting technique based on an assessment of the future prospects for the functioning of an economic entity.

In accordance with this, in our opinion, it is advisable to consider the following issues:

– to investigate the issues of the place and role of forecasting in the system of internal control of production activities of agricultural organizations;

– to determine forecasting as a specific method of internal control;

– to substantiate the possibility of using an economic and mathematical model based on the definition of guaranteed production in the plant growing industry, focused on obtaining maximum revenue.

Purpose of the Study

The purpose of the work is to determine the meta and the role of forecasting in the production activities of agricultural organizations in the internal control system and in the development of an economic and mathematical model that allows assessing the future prospects for the functioning of an economic entity.

Research Methods

The studies were carried out on the basis of financial statements and the results of internal control of agricultural organizations in the Tambov region.

The research materials include the following sources of information required for internal control of production activities: balance sheet; accounting policy, production and financial plan, estimates, production calculations, primary documents and accounting registers for expense accounts 20, 23, 25, 26, 29.

In the course of the study, the methods of induction, deduction, generalization, analogy, system analysis, and evaluation were used. In addition, the techniques of documentary and factual control were used.

Findings

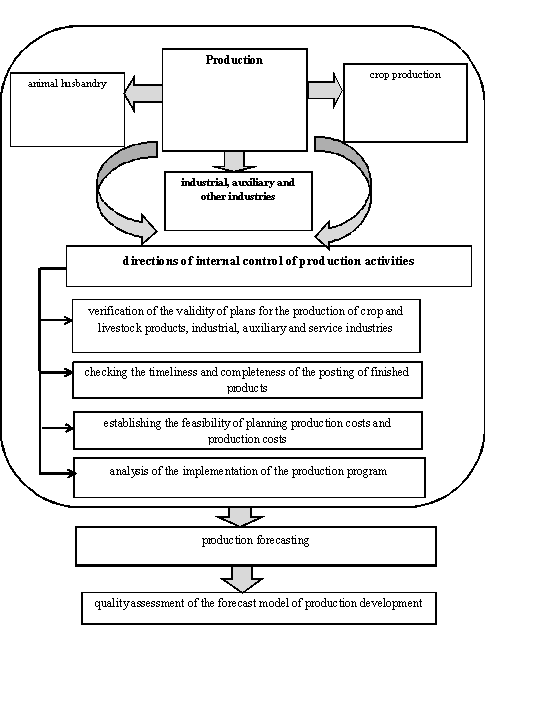

In agricultural organizations, the directions of internal control are manifested not only in the key objects of inspection, but also in the planned measures and procedures aimed at ensuring the efficient conduct of production activities, promoting finished products, using a set of technological processes using innovative technologies, developing clear recommendations for the development of production and prevention of on-farm risks.

The more complex the structure of the internal environment of an agricultural organization, the more is required not only actual, but also predictive information to make effective management decisions (Nikitin et al., 2019).

Forecasting plays an important role in the implementation of internal control tasks, consisting in establishing the feasibility of planning the development of branches of the main production, as well as checking the correct use of resources and the implementation of technological discipline (Figure 1).

The place and role of forecasting in the system of internal control of the production activities of agricultural organizations is determined by the close unity of specific tasks and directions of control actions (Korobeynikova et al., 2021).

Internal control techniques implemented for the purposes of further planning and forecasting of production activities are associated not only with checking the validity of production plans, the timeliness and completeness of the posting of products, establishing the validity of cost planning, but also with analyzing the implementation of the production program (Vedenkina, 2021).

The use of forecasting in the course of internal control of production activities allows specialists to improve information transparency, to organize their verification qualitatively (Popova, 2015).

Forecasting can be defined as a specific technique of internal control aimed at determining the main indicators of the production activity of an agricultural organization, reflecting the relationships and patterns of development based on a detailed analysis of market conditions, changes in market conditions for the coming period (Gorlov et al., 2021).

To forecast production, it is advisable to use an economic and mathematical model based on the definition of guaranteed production in the crop production industry, focused on obtaining maximum revenue (Popova & Fetskovich, 2015).

Let us consider the features of using the proposed model on the example of a typical agricultural organization of the Tambov region—LLC “Vishnevskoe”.

The model contains the following restrictions.

Maximum revenue: Z m a x = X i,

where Xi is the revenue from the sale of crop products;

In terms of resources: ∑ a i j * x i ≥ B i,

where aij are the costs of the-th type of resources per 1 ha of the-th cultivated crop;

xi is the area of the-th cultivated crop;

Bi is the the amount of the-th resources.

Arable land, ha: X j ≤ B j,

where Bj is the planned area of the-th arable land.

Non-negativity of the variables included in the problem: xj ≥ 0

The maximum arable land area of 4719 hectares is limited for the area under crops:

- x1 + x2 + x3 + x4 + x5 + x6 + x7 + x8 ≤ 4719;

Labor costs are limited to 110,000 man-hours:

- 18x1+12x2+14x3+20x4+30x5+22x6+15x7≤110000;

The following limitations of the model guarantee the production of winter cereals, spring cereals, corn for grain, pulses, sunflowers, etc. and look as follows:

- 45x1≥20000;

- 40x2≥35000;

- 90x3≥25000;

- 25,5x4≥5500;

- 600x5≥100000;

- 28х6≥20000;

- 30х7≥15000;

Winter grain area in the MAX grain group (40%), ha:

- 0.6х1-0.4х2-0.4х3-0.4х4≤0;

Grain area MAX 60%, ha:

- 0.4x1+0.4x2+0.4x3+0.4x4-0.6x5-0.6x6-0.6x7-0.6x8≤0;

Area of corn for grain MAX 60%, ha:

- -0.08x-0.08x2+0.92x3-0.08x4-0.08x5-0.08x6-0.08x7-0.08x8≤0;

Sugar beet area MAX 10%, ha:

- -0.1x1-0.1x2-0.1x3-0.1x4+0.9x5-0.1x6-0.1x7-0.1x8≤0;

Sunflower area MAX 20%, ha:

- -0.2X-0.2x1-0.2x2-0.2x3-0.2x4-0.2x5-0.2x6+0.8x7-0.2x8≤0;

Soybean area MAX 20%, ha:

- -0.2X-0.2x-0.2x2-0.2x3-0.2x4-0.2x5+0.8x6-0.2x7-0.2x8≤0;

Fallow area, MAX20%, ha:

- -0.2X-0.2x1-0.2x2-0.2x3-0.2x4-0.2x5-0.2x6-0.2x7+0.8x8≤0;

Fallow area, MIN 10%, ha:

- -0.1X-0.1x1-0.1x2-0.1x3-0.1x4-0.1x5-0.1x6-0.1x7+0.9x8≥0;

Costs per hectare, rubles:

33750x1 +28000 x2 + 60300x3 +25500 x4 + 90000x5 +50400x6 + 45000x7

Revenue per hectare, rubles:

54000x1 + 44000x2 + 108000x3 + 30600x4 + 108000x5 + 56000x6 + 75000x7

Optimality criterion is maximum profit:

Z(max) = X j - Х j', where:

X j is the amount of revenue from the sale of crop production;

Х j' is the amount of production costs in crop production.

The solutions obtained during the analysis are presented in Table 1.

According to the results of the studies carried out using the economic and mathematical model, it can be seen that according to the recommended planned indicators, it is possible to achieve revenue of 255,284.4 thousand rubles, which is 48% more than in 2019. At the same time, the planned costs should be 172,510 thousand rubles, which is 21% more than in 2019. The planned profit of LLC “Vishnevskoye” under favorable circumstances will amount to 82,775 thousand rubles. The total amount of profit will increase by 54002.4 thousand rubles, and the level of production profitability will increase to 48%.

According to resource constraints, the organization is recommended to get the maximum profit, the following crop rotation: winter cereals - 1133 hectares, spring crops - 1106 hectares, corn for grain - 378 hectares, legumes - 216 hectares, sugar beets - 167 hectares, soybeans - 714 hectares, sunflower - 535 hectares, fallow - 472 hectares.

In this optimal planning of the production activity of the analyzed enterprise, all possible influencing factors are taken into account, with the exception of natural ones, since they cannot be predicted (Smagin, 2015).

It must also be said that the initial model for the production of products obtained at the planning stage can be edited during the entire production cycle.

Conclusion

For the purposes of forecasting production activities, various economic and mathematical models can be used, which differ not only in the degree of aggregation of the indicators included in the model, but also in accordance with the goals and objectives of internal control of production activities.

Thus, forecasting, being the most important method of internal control of production activities, is a purposeful activity of regulatory bodies to develop prospects for the development of an agricultural organization in the medium and long term on the basis of scientifically grounded prediction of the dynamics of economic processes.

References

Gorlov, I. F., Usenko, L. N., Kholodov, O. A., Kholodova, M. A., Mosolova, N. I., & Mosolova, D. A. (2021). Conceptual approaches to planning and forecasting agricultural production transformed by digitalization. IOP Conference Series: Earth and Environmental Science, 677(3), 032022.

Korobeynikova, O. M., Korobeynikov, D. A., Popova, L. V., Chekrygina, T. A., & Shemet, E. S. (2021). Artificial intelligence for digitalization of management accounting of agricultural organizations. IOP Conference Series: Earth and Environmental Science, 699(1), 012049.

Nikitin, A., Kuzicheva, N., & Karamnova, N. (2019). Establishing efficient conditions for agriculture development. International Journal of Recent Technology and Engineering, 8(2), 1-6.

Popova, V. B. (2015). Statistical analysis of economic data. Bulletin of the University of the Russian Academy of Education, 4, 13-20. (In Rus)

Popova, V. B., & Fetskovich, I. V. (2015). Statistical analysis of agricultural production in the Tambov region. Finance and Credit, 23(647), 40-51. (In Rus)

Smagin, B. I. (2015). Cluster analysis in economic research of the agricultural sector of production. Bulletin of the Michurinsk State Agrarian University, 2, 97-105. (In Rus)

Vedenkina, I. V. (2021). Financial forecasting at the enterprises of the poultry subcomplex. IOP Conference Series: Earth and Environmental Science, 677(2), 022069.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 February 2022

Article Doi

eBook ISBN

978-1-80296-123-2

Publisher

European Publisher

Volume

124

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-886

Subjects

Land economy, land planning, rural development, resource management, real estates, agricultural policies

Cite this article as:

Akindinov, V. V., Loseva, A. S., Popova, V. B., & Fetskovich, I. V. (2022). Forecasting As Method Of Internal Control Of Production Activities In Agricultural Organizations. In D. S. Nardin, O. V. Stepanova, & E. V. Demchuk (Eds.), Land Economy and Rural Studies Essentials, vol 124. European Proceedings of Social and Behavioural Sciences (pp. 90-96). European Publisher. https://doi.org/10.15405/epsbs.2022.02.12