An Approach To Developing Digital Enterprise Business Models

Abstract

Traditional business models often do not cope with the modern requirements of the main stakeholders of enterprises. Successful business models and strategies the companies had previously focused on are not relevant for digital businesses. To make rational management decisions, today’s business models must take into account the characteristics of the digital enterprises. Modern business models are developed in accordance with the approach proposed in the works of A. Osterwalder. At the same time, this approach is more applicable to the enterprises of the industrial era. In particular, the author focuses on key activities, resources, partners, customers, and the company's cost structure. For digital enterprises, the main competitive advantage is the ability to quickly adapt under the influence of changes caused by external and internal factors. To do this, companies need to identify their key technological competencies and use them effectively. Therefore, the business models that are formed in digital enterprises must take this aspect into account. This article proposes an approach to business models development for digital enterprises based on the identification of the company's key technological competencies. In turn, technological competencies are formed on the basis of knowledge, skills of technological personnel, as well as resources of enterprises. In addition, new business models of digital enterprises imply the formation of strategic network models based on the key technological competencies of enterprises that are part of them. This will eventually lead to a change in approaches to the formation of business models.

Keywords: Digital enterprise, business model, technological competences, digital transformation

Introduction

In the modern world of rapidly changing processes and technologies, driven by the end consumer demands, companies need to be adaptive to new market requirements in order to maintain and increase their competitiveness. Shortened product life cycles, market turbulence and customization lead to digitalization of enterprise business processes and require them to review and develop new business models.

Companies using traditional business processes are often unable to satisfy customers. Strategies previously effective that may keep under the implementation of successful approaches to enterprise digitalization in the future, need to be completely revised. To accelerate decision-making, companies around the world are digitally transforming.

Digital transformation is defined as a process that is initiated and occurs under the influence of external factors, among which a positive customer experience is the main one. The partners and customers of a company today have high expectations regarding access to information about its work, services and products. This level of user experience can only be achieved by using the technologies able to aggregate and process data and then provide it to the customers and partners.

It is the positive customer experience which not only keeps companies on the market but also to broaden their presence. This is closely connected with the increase in operational efficiency, which is achieved through the enterprise digital transformation.

For the purposes of this work, a digital enterprise is referred to as an extensive network of digital models, methods and tools, as well as, among other things, modeling tools and three-dimensional visualization. Their integration is executed by means of a comprehensive data management system.

What is the specific thing about digital enterprises that is the use of a network of digital models, methods, tools and modeling tools and three-dimensional visualization, which are managed through an integrated big data analysis system. The goals of a digital enterprise are the complex planning, evaluation and ongoing optimization of the most important structures, processes and resources of a real enterprise in relation to its products.

Taking into account the above said, the approach to developing a business model of a digital enterprise will have its own characteristics and specifics.

Problem Statement

Since the main competitive advantage of digital enterprises is the ability to quickly cross over under the influence of changes caused by external and internal factors, the traditional approach to developing a company business model proposed by A. Osterwalder and I. Pigne, requires certain changes and additions.

The classic model of A. Osterwalder consists of 9 basic elements which are usually represented in a table (Carter & Carter, 2020; Corbo et al., 2020; Osterwalder & Pigne, 2010):

- value (exactly what we deliver to customers?);

- resources (what key resources do our value propositions require?);

- activities (what activities do our value propositions require?);

- partners (who are our key partners?);

- customer relations (what type of relationship does each of our customer segments expect from us?);

- customers (for whom are we creating our values?);

- sales channels (through which channels do we interact with our customers and deliver our value propositions to them?);

- costs (what are the most important costs inherent in our model?);

- revenues (what revenue streams do we generate?).

Research Questions

The main questions that had been raised in the study are:

- identification of problems of enterprises within business process digitalization;

- development of an approach to adapting the company's business model for operation in the digital economy;

- identification of the key technological competencies that drive the growth of a company's value;

- approbation of the research results in a high-tech enterprise.

Purpose of the Study

The purpose of the study is to create an approach to developing digital enterprise business models. This approach involves the identification of a core in each element of the business model, in the process of enterprise digital transformation. The classical Osterwalder model focuses on key activities, resources, partners, customers, and a company's cost structure. For digital enterprises, the main competitive advantage is the ability to quickly adapt under the influence of changes caused by external and internal factors. The approach proposed in the article allows us to achieve this goal.

Research Methods

In order to adapt the classical approach to the formation of a business model for digital enterprises, the authors propose to transform it by identifying a key core within each element of the model (Figure 1).

This model development is based on Penrose resource approach to management and the competency-based approach of Prahalad and Hamel (2009), Prahalad and Ramaswamy (2004a, 2004b). These approaches emphasize the importance of resources and key competencies for creating strategic competitive advantages.

Penrose's resource approach implies that a company is a resource pool, not a set of products or market share. Resources are considered as elements of an enterprise, which are its strengths and weaknesses. From the technology management point of view, the following types of resources can be identified: material (physical objects, financial resources); intangible (high technology assets, information, corporate culture, organizational structure) and human (personnel and their knowledge and skills in the field of development, production, technology or infrastructure).

In order to gain a competitive advantage, a company must be able to determine the potential of a resource before acquiring or expanding it. And for a digital enterprise, resources must also be given a digital maturity outlook. A digital maturity outlook of a resource should be given upon six criteria: level of informational support, level of connectivity, level of visibility, level of transparency, level of predictability, level of adaptability (Schuh & Klappert, 2011).

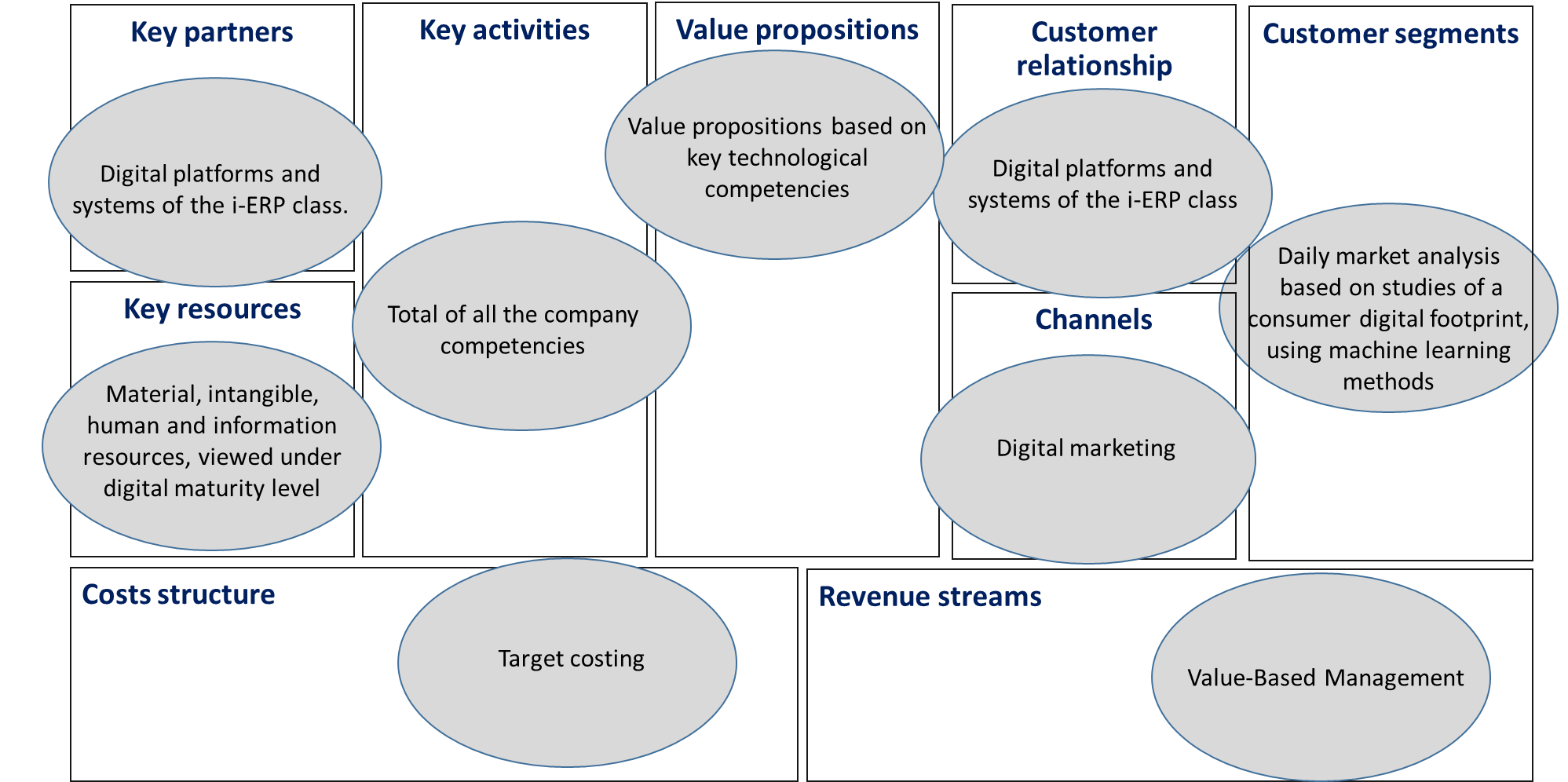

Thus, the key core of the “resources” element in a digital enterprise business model will be material, intangible, human and information resources, viewed under digital maturity level.

The essence of the competency-based approach by Prahalad and Hamel implies that the basis of a company’s competitiveness is its unique abilities and competencies, which can be used synergistically in several areas of business, products and services. The success can be achieved by the company if it manages to use the synergetic effect faster and at lower cost.

Key technological competencies include a set of competencies that provide а company with a sustainable source of its competitive advantage. A sustainable competitive advantage is formed when four conditions are simultaneously completed: competence is rare, difficult to reproduce, not replaceable and valuable (Prahalad & Hamel, 2009). Competencies should be valuable, then they lead to efficiency and increase productivity. Competencies should be rare, and thus provide potential for differentiation. To maintain this potential in the long term, competencies must be non-reproducible and non-replaceable at the same time. The imitation of the technological competencies must be difficult for the enterprise competitors to complete. The competitive advantage of an enterprise becomes sustainable if all four criteria are completed.

Innovative technologies used both in the production process and other business processes of an enterprise are the basis for a digital enterprise. Then, the key technological competencies of a digital enterprise will be aimed not only at harmonizing technological flows, but also organizing business processes and maximizing the consumer value of final goods and services.

It is worth mentioning that technological competencies link existing businesses and drive creation of new ones. At the same time, areas of enterprise diversification and market choice for expansion should be determined exactly by the technological competencies, but not only by the market attractiveness.

The identification of key technological competencies is based on three criteria: the ability to enter a variety of markets, the high value of final goods and services for consumers, and effortful imitation of a competence. The ability to harmonize complex set of technological and production skills definitely satisfies these criteria. A competitor who manages to master technologies related to key competencies will face a much more difficult task of reproducing interrelated processes of coordination and training (Grant, 1991; Müller-Stewens & Lechner, 2005).

The development of key competencies requires employees’ communication, involvement and willingness to cooperate across intra-organizational boundaries. Employees of the majority of levels and all functional units should have these qualities. The organizers of the process of developing core competencies should be employees with sufficiently broad interests, able to see new unusual combinations of their knowledge and experience with the knowledge and experience of employees of other specialties (Khoroshko & Kuznetsov, 2021).

The key competencies are not lost while using them. Unlike tangible assets that depreciate over the time, competencies are intensified as they are used collectively. However, competencies must be consciously developed and protected: knowledge is lost if it is not used. The key competencies connect existing businesses.

Therefore, the core value of a digital enterprise from the consumer point of view should be formed on the basis of its key technological competencies (the core of the “value” element), which in return should be identified from the total of all the company competencies (core of the “key activities” element).

It can therefore be concluded that resources, abilities and core competencies are not independent. They are interconnected and together form the technological expertise of the company.

For the “customer interaction” element in a digital enterprise business model, the organization’s use of i-ERP and i-MES digital platforms and systems will be essential.

Today, the platform approach has become a leading one and almost all the largest companies in the world use platform business models to promote their business. The basic configuration of the platform implies that manufacturers and end consumers are brought together and get the opportunity to interact directly (Kuprevich, 2018). Using digital platforms allows companies to reduce their transaction costs and time required to deliver new products to the market.

Currently, the only i-ERP system that meets the requirements of a digital enterprise is SAP S / 4 HANA. The optimization of this system is aimed at the interaction of RAM and processor. In addition, SAP S / 4 HANA implements a multi-layer method of storing information, which allows the system to use data compression mechanisms. Thus, the platform works with already compressed information and may not waste time and other resources to unzip. Column storage also helps to reduce the amount of data stored in the system. This is due to the fact that the system can aggregate information quickly, and the user can work with detailed information and make better decisions.

Thus, this system performs advanced analytics (intelligent analytics, spatial data processing, text analytics, text search, stream analytics, graphic data processing) and includes the capabilities of an ETL system. Also, this system has the ability to integrate both a number of applications contained in the application server, and third-party applications.

In addition to the above said, SAP Se developed a digital platform - SAP S / 4 HANA Cloud Platform for IoT based on the SAP S / 4 HANA system.

For the “key partners” element, an integral term for a digital enterprise will be an interaction with its counterparts via digital platforms and systems of the i-ERP class.

In the “sales channels” element the core will be marketing strategy development for the company based on a digital consumer footprint, the so-called Agile marketing.

Agile marketing is characterized by a high degree of adaptation of the company’s marketing strategy as a response to the external market changes. According to this approach, a daily market analysis is carried out, based on studies of a consumer digital footprint, using machine learning methods. This will allow to make more accurate segmentation of consumers, individualize a product and transfer the transactional marketing to the relationship marketing even in B2C markets, thereby increasing customer satisfaction.

When describing the “costs” element, it is necessary to concentrate on the costs size and structure as well as cost optimization process. For this, it is necessary to classify the most considerable and relevant currently well-known approaches to cost management, which can be fully or partially implemented on digital enterprises.

So for digital enterprises, one of the priority methods aimed at achieving the goal - cost optimization is target-costing.

The idea of the target costing method is to produce only those products which estimated cost does not exceed the target one, that is cost is calculated based on a predetermined (target) sale price (Chervenkova & Prosvirina, 2011).

The process of setting a product target price involves the use of a three-level analysis "product quality - a set of the product functional characteristics - product price", where price is assumed or set by both market as a whole and direct consumer. This price is determined through the market research, in fact being the expected market price of products. Target profit represents the amount of profit required for an enterprise to develop and meet the needs of owners.

To determine the target cost of the product, the target profit value is subtracted from the expected market price. Then, all parts of the production process, from a manager to a worker, work on designing and manufacturing products corresponding the target cost.

The main principles of the target costing are the following:

- constant focus on market and customer requirements;

- calculation of target costs for new products, as well as their components, allowing to achieve the desired, predetermined profit in the existing market conditions;

- taking into account the impact on the cost of production of consumer requirements to the quality and timing of production;

- use of the product life cycle concept.

The element "revenue" in the traditional interpretation presupposes the priority for the formation of the total of revenue and cash flows from them. For a digital enterprise, it’s not enough to know what flows we generate and what their size is. A clear idea is necessary of how to manage these cash flows in order to achieve the main goal - to accelerate the growth of an enterprise value. Therefore, the ability to identify key cost factors that have the greatest impact on the cash flow and a digital enterprise value respectively is critical. That is why the core of the “revenue” element will be the introduction of a cost-based management approach (or value-based management system-VBM) within an enterprise (Copeland et al., 2008).

The company's value management is an integrating process aimed at the qualitative improvement of strategic, tactical and operational decisions at all levels of the company's management by concentrating common efforts on the key cost factors. The value of the company is determined by its discounted future cash flows, and new value is created only when the companies receive a return on invested capital that exceeds the cost of capital raising (Butko et al., 2020; Chervenkova & Prosvirina, 2019; Yeleneva et al., 2018). Therefore, the task of the digital enterprise management is to identify the key cost factors that have the highest impact on these indicators.

The cost factor is the characteristic of an enterprise, which the effectiveness of its operation depends on. The algorithm for identifying the key cost factors should be as follows:

- value creation analysis, establishing the relationship of the operating elements of a company with the value creation process;

- priorities setting, identifying factors with the most significant impact on value;

- target setting and planning. Based on the key cost factors, the goals of an enterprise, its main business areas and structural divisions, an enterprise performance evaluation system is being created.

The implementation of this approach can significantly improve the quality of management, as well contributing to the growth of the business investment attractiveness.

Findings

The developed approach was tested in the project of the digital production design of aircraft engines.

The key technological competencies were determined as follows: products (engines) with a long service life and high reliability based on a single product platform, the production of principle components and assembly units, assembly of the finished product. The key technological competencies of the enterprise are providing intangible resources such as knowledge database, human resources (highly qualified personnel) and material resources (technological equipment). Since the digital maturity of the enterprise was assessed as low according to all criteria, it was decided to redefine the innovative business model of the designed digital production based on its key technological competencies.

First of all, to support key competencies, an innovative technological process was developed to ensure the target cost of an aircraft engine production. For this process, the missing resources were identified in accordance with the required digital maturity criteria, capable to provide the digital enterprise operation.

To ensure interaction with the client, a digital platform was selected based on the CRM module of SAP S/4 HANA. It will allow to reduce the cost of the product life cycle in the future. In addition, the SAP S/4 HANA system will ensure high manageability of supply chain owing to a digital twin of the supply chain system from other enterprises.

It is planned to increase customer satisfaction in the future through the use of PLM - a system that will allow continuous analysis of the engines operation and wear as well as their service maintenance.

As an approach to managing the company's value, a balanced scorecard was developed, the analysis of which is carried out continuously on the basis of data collected by the i-ERP system in four areas - finance (indicators of the target cost of the product, business value), customer satisfaction (quality and after sales service), indicators of digital maturity of business and human resources management processes.

As a result of the project, an innovative business model for the aircraft engines production of was developed, which will allow the company to achieve a high level of competitiveness not only in Russia but also on the world market.

Conclusion

Summing up, it may be concluded that the business model of a digital enterprise is a structure that describes the value of the organization offered to its customers, formed by the identification of its key technological competencies. It also reflects the resources and abilities of the company, a list of its key partners, tools and methods necessary for the promotion and delivering its value to customers, and a description of its managerial influences aimed at increasing the value of its business.

References

Butko, A. O., Kuznetsov, P. M., & Khoroshko, L. L. (2020). Creating a digital twin of crushing and milling equipment reconditioning process. Mining Informational and Analytical Bulletin, 8, 130-144.

Carter, M., & Carter, C. (2020). The Creative Business Model Canvas. Social enterprise journal, 16(2), 141-158.

Chervenkova, S. G., & Prosvirina, M. E. (2011). Formirovanie metodov upravleniya zatratami na mashinostroitel'nom predpriyatii [Forming methods of cost management for machine-building company]. Russian entrepreneurship, 5-2, 136-141. [in Rus.].

Chervenkova, S. G., & Prosvirina, M. E. (2019). Primenenie metodov matematicheskogo modelirovaniya pri planirovanii denezhnyh potokov predpriyatiya [Application of mathematical modelling methods for cash flow planning]. Vestnik MSTU Stankin, 1(48), 135-140. [in Rus.].

Copeland, T., Koller, T., & Murrin, J. (2008). Valuation. Measuring and managing the value of companies. M.: Olymp-Business.

Corbo, L., Mahassel, S., & Ferraris, A. (2020). Translational mechanisms in business model design: introducing the continuous validation framework. Management decision, 58(9), 2011-2026.

Grant, R. M. (1991). The resource-based theory of competitive advantage: implications for strategy formulation. Calif. Manag. Rev, 33(3), 114–135.

Khoroshko, L. L., & Kuznetsov, P. M. (2021). Information Environment for the Design of Industrial Processes. Russian Engineering Research, 41(3), 277-280.

Kuprevich, T. (2018). Cifrovye platformy v mirovoj ekonomike: sovremennye tendencii i napravleniya razvitiya [Digital platforms current trends and directions for the development in the world economy]. Economic Bulletin of the University, 37(1), 311-318. [in Rus.].

Müller-Stewens, G., & Lechner, C. (2005). Strategisches Management, 3. Aufl. Schäffer-Poeschel, Heidelberg.

Osterwalder, A., & Pigne, I. (2010). Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. John Wiley and Sons.

Prahalad, C. K., & Hamel, G. (2009). The core competence of the corporation. Knowledge and Strategy.

Prahalad, C. K., & Ramaswamy, V. (2004a). Co-creating unique value with customers. Strategy & Leadership, 32(3), 4-9.

Prahalad, C. K., & Ramaswamy, V. (2004b). Co-creation experiences: The next practice in value creation. Journal of Interactive Marketing, 18(3), 5-14.

Schuh, G., & Klappert, S. (2011). Technologiemanagement Handbuch Produktion und Management. Springer.

Yeleneva, J., Kharin, A., Yelenev, K., Andreev, V., Kharina, O., & Kruchkova, E. (2018). Corporate knowledge management in Ramp-up conditions: The stakeholder interests account, the responsibility centers allocation. CIRP Journal of Manufacturing Science and Technology, 23, 207-216.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

25 September 2021

Article Doi

eBook ISBN

978-1-80296-115-7

Publisher

European Publisher

Volume

116

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-2895

Subjects

Economics, social trends, sustainability, modern society, behavioural sciences, education

Cite this article as:

Andreev, V. N., Eleneva, J. Y., Chervenkova, S. G., Charuyskaya, M. A., Popolitova, S. V., & Kryzhanovskaya, A. S. (2021). An Approach To Developing Digital Enterprise Business Models. In I. V. Kovalev, A. A. Voroshilova, & A. S. Budagov (Eds.), Economic and Social Trends for Sustainability of Modern Society (ICEST-II 2021), vol 116. European Proceedings of Social and Behavioural Sciences (pp. 612-620). European Publisher. https://doi.org/10.15405/epsbs.2021.09.02.68