Financial And Insurance Market Trends

Abstract

The insurance market in the Russian Federation allows it to act as a financial intermediary. The activities of insurance organizations can compensate for the consequences arising from unforeseen random events that cause damage to economic entities. As a result of the stated research problem, the subject of the research is the process of development of the insurance market in the Russian Federation, and the object of research is the insurance market. The aim of the study is to analyze the dynamics of the national insurance market development and insurance services market by federal districts. The methodological framework of the research is based on the works of Russian and foreign scientists. The main methods that allow us to study the specifics of the insurance market are the general economics methods applicable for the statistical information analysis and collecting the set of data of insurance market development. As a result, the systematic analytical approach is applied in the research. It is suitable for correlating and systemizing the statistical information in order to conclude what the directions of the insurance market development are. The results obtained in the framework of the study can be used in the formation of conceptual directions for the development of the insurance market. The trends and competitive advantages of the insurance market identified form strategic blocks, which can be relevantly used to form an actively functioning insurance services market.

Keywords: Financial activities, insurance activities, insurance market

Introduction

In today’s business environment it is essential to form institutional tendencies that guarantee economic entities protection and reduction of social and economic risks (Grigoryeva & Tarasova. 2010).

The insurance system functioning allows economic entities to mitigate the consequences of the economic and business processes entailing different kinds of losses. The positive aspect of the insurance framework operation is providing the market with the long-term financial resources. The government sector is exempt from the expenses for various implications of economic activities. The implications can be of natural, technological and socio-economic origin.

Problem Statement

The problem of insurance effective functioning as an economic system has been under active discussion in the scientific community. Some researchers define the changes taking place on the insurance market as a tendency to increasing activity. Others note that there is a restructuring of the insurance market. This trend is caused by various risks and the menace to safety and growth of public wealth (Fedorova, 2004).

Research Questions

Let us take a look at the main directions of the insurance industry development as the essential part of the insurance market.

In Platonova’s work (2015), the important factor characterizing development and sustainability of the insurance industry is the amount of insurance agents. The more agents there is, the more positive the influence of the industry of the competition on the market. With higher competition, there are more opportunities for smaller companies, including regional ones, to effectively handle particular cases that cannot be solved by bigger organizations.

Furthermore, Kirilyuk and Sviridov (2019) who appeal to the Russian Central Bank annual reports, consider that the development of insurance market is characterized by the following factors:

- the number of contracts concluded to assess the prevalence of insurance among the population and determines the possible number of insured events provided by insurance;

- the volume of collected insurance premiums, which allows you to determine the income of insurers, and is also associated with the level of stability of the economy.

- the volume of insurance payments by which it is possible to assess not only the costs of insurers, but also the amount of compensation for damage to the economy.

Kirilyuk and Sviridov (2019) talk about the necessity of approximating the rules of the Russian insurance companies to the rules that foreign companies follow. This is possible to be executed by integrating international principles and rules.

However, in Lampsie’s (2018) opinion, the transition to the international standards of accounting and reports has been complicated. For example, 11 out of 67 professional insurance brokers had to quit.

Tsibulevsky (2019) in his review of regulatory requirements for the risk management system in insurance companies points to a number of shortcomings in the regulation of the insurance industry noted by European insurers and supervisory authorities, in particular:

- formal requirements did not sufficiently consider individual risks;

- the ratio of liabilities and assets was not sufficiently considered;

- companies had little motivation to implement risk management;

- the requirements of the regulator were poorly coordinated with internal corporate standards for risk management.

According to previously mentioned experts, such as Chistyukhin and Buravleva (2016); Daihel (2011); Tsibulevsky (2019), the above deficiencies can be eliminated by introducing a legislative base based on the principles of a risk-based approach and oriented to the market value of assets.

Otherwise, Antyushina (2019a, 2019b) thinks that this is associated with significant costs, which will lead to an increase in the concentration of capital, a decrease in the level of competition, which will cause a decrease in the quality of services, higher prices and slow down the development of the insurance market in general.

Speaking about improving the insurance market, experts such as Koziy and Samiev (2019) note the need of using information technology (IT) in insurance. This is called Insurtech. It simplifies the workflow, automatization of the work of insurers, and the possibility of obtaining more detailed and personalized information about the insured. This also will improve the transparency of the industry.

Purpose of the Study

The purpose of the work is to analyze the dynamics of changes in the indicators of insurance activity in the federal districts of the Russian Federation.

Research Methods

The operating conditions of economic entities in the Russian Federation are characterized by a high level of manifestation of the risk environment, which is confirmed by statistical data (Vinnikova et al., 2018). Under the current conditions, the existence of a functioning insurance market will ensure the necessary level of reduction of negative consequences. Changes in the field of insurance, occurring as a result of demand for services in this area, are the response to changes in society. The emergence of innovative developments in society entails the needs of economic entities in insurance protection. The implementation of this direction is possible under the following conditions: the emergence of a need for protection, reinforced by the desire and opportunities for protection. The criterion for the functioning of insurance activities is a sufficient amount of free cash from consumers of insurance services, the availability of free choice of high-quality services in the market, the presence of solvent, financially stable organizations that are ready to provide insurance services (Orlanyuk-Malitskaya & Yanova, 2010).

Findings

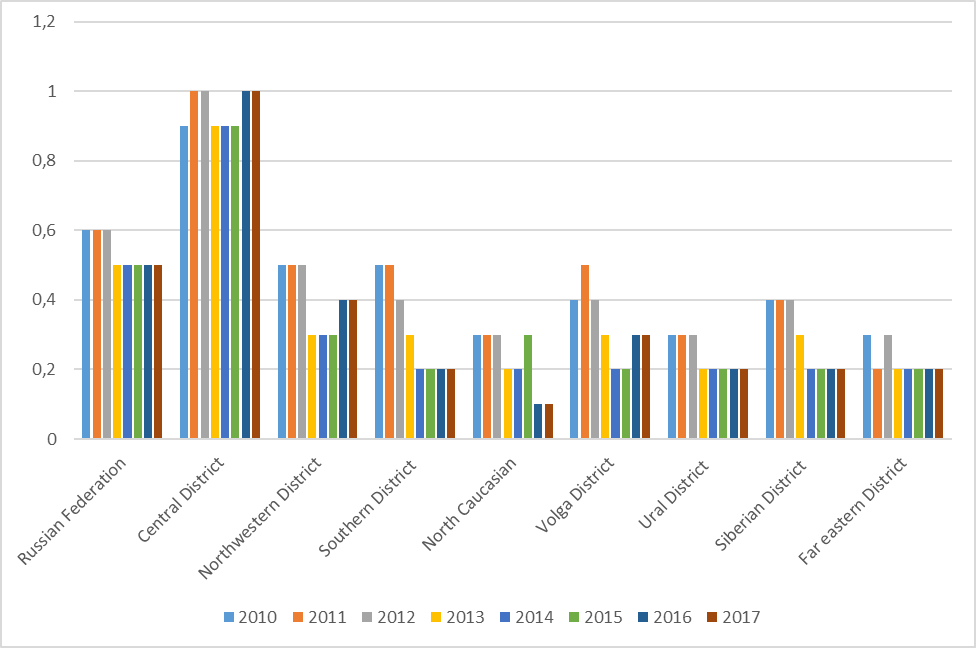

An assessment of the dynamics of development of the financial and insurance sectors by regions and federal districts in the sectoral structure of gross value added showed an uneven distribution of economic activity. Analysis of the activities of insurance organizations showed that the center of attraction is the Central Federal District, which includes Moscow (table 1).

*Source: Rosstat data, compiled by the authors

Statistics show that the leader with a significant margin from the rest of the districts is the Central Federal District. This fact confirms the trends that were determined by the geographical concentration of insurance and financial activities (Rezanova & Moroshkina, 2019). The data are shown in Figure 1.

The analysis showed that from 2010-2011, most of the constituent entities of the Russian Federation have a higher gross value added than in the subsequent period. There is a decrease in the economic activity of the insurance market. The leading position is held by the Central Federal District, which includes the capital and its metropolis, being the center of financial and banking activities. The maximum decrease is in the North Caucasian Federal District. This decline is due to the low level of economic activity in the district, leading to a reduction in insurance activity.

Conclusion

In general, the insurance industry gave good development indicators for the study period. It should be recognized that the expansion of the Russian insurance market in 2018 is mainly ensured, as before, by consumer credit and mortgage insurance. Thus, if we exclude the banking insurance sector, the quality of growth of the Russian insurance market in the last three to four years should be recognized as unsatisfactory.

The completeness of meeting the requirements for insurance coverage is extremely low. In particular, about 6% of the country's adult population use life insurance services. The main factor in the accelerated development of life insurance is the development of retail banking insurance, accompanied by borrower life insurance (Aliev & Atakaev, 2016).

Branch offices in the regions, as before, serve as a source of planned additional financial flows, while the parent companies, as a rule, have little concern about how these funds will be obtained. The problem of the effectiveness of state regulation of the activities of insurance market entities, including the intermediary environment, has not been completely resolved. The negative image of Russian insurers remains, based both on the quality of the services provided by the companies and on the preference of the insurers for their own interests to the detriment of the interests of the insurers.

To sum up, Russia, as before, despite the relatively high growth rates of insurance, is characterized by the weak development of this sector of the economy that does not meet the needs of society.

Acknowledgments

The study was carried out as part of a research work at the Institute of Economics of the Karelian Research Centre of the Russian Academy of Sciences (No. AAAA-A19-119010990087-1).

References

Aliev, O. M., & Atakaev, A. Z. (2016). The development of the Russian insurance market. Fundamental research, 12-5, 1034-1038.

Antyushina, V. (2019a). Basel III International Banking Standards: Reform Continues. Young Scientist, 3(241), 142-145.

Antyushina, V. (2019b). European solvency standards for Solvency II insurance companies in the EU and the Russian Federation at the present stage. Young scientist, 3(241), 145–148.

Chistyukhin, V., & Buravleva, N. (2016). From Basel II to Solvency II or what is a risk-based approach to assessing the solvency of insurers: first steps towards implementation, tasks and prospects Analytical Banking Journal. www.insur-info.ru/press/125074

Daihel, V. (2011). Adaptation of Solvency requirements to Russian conditions. International Conference on Insurance. www.insuranceconference.ru/2011/files/presentations/3-4_1/RIS_2011_DeichlW.pdf

Fedorova, T. A. (Ed.) (2004). Insurance: Textbook: Types of insurance, p. 126-140.

Grigoryeva, E., & Tarasova, Yu. (2010). Financial entrepreneurial structures: transformation under the influence of market conditions. Monograph. St. Petersburg: Publishing House Petropolis.

Kirilyuk, I. L., & Sviridov, A. P. (2019). Insurance Market in Russia. Current Status and Prospects Issues of Theoretical Economics (VTE), 2, 43–61.

Koziy, S., & Samiev, P. (2019). Transition to XBRL: fiction or productive implementation? Banking review. bosfera.ru/bo/perehod-na-xbrl-fikciya-ili-produktivnoe-vnedrenie

Lampsie, A. (2018). XBRL: Painful and noticeable Bank Review. bosfera.ru/bo/xbrl-boleznenno-i-zametno

Orlanyuk-Malitskaya, L. A., & Yanova, S. Yu. (Eds.) (2010). Insurance: textbook. M.: Publishing house Yurayt; Higher Education, p. 240-254.

Platonova, E. (2015). Trends in the development of the insurance market in Russia. Regional aspect Actual problems of the functioning of the insurance system of the Russian Federation. Sat. materials on the basis of the scientific method. Seminar of the Analytical Department of the Staff of the Council of the Federation on November 5, 2015. Moscow, p. 58–70.

Rezanova, L. V., & Moroshkina, M. V. (2019). The insurance market of Russia on the modern. Finance and credit, 25(9)(789), p. 2179-2192.

Tsibulevsky, M. (2019). Overview of regulatory requirements for a risk management system in insurance companies. uainsur.com/wp-content/uploads/2019/02/2.-Solvency-II-short-version.pdf

Vinnikova, I. S., Kuznetsova, E. A., Kokina, K. M., & Kurylev, A. I. (2018). Prospects for the development of strass business at the present stage. International Journal of Applied and Fundamental Research, 5-1, 204-208.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 July 2021

Article Doi

eBook ISBN

978-1-80296-112-6

Publisher

European Publisher

Volume

113

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-944

Subjects

Land economy, land planning, rural development, resource management, real estates, agricultural policies

Cite this article as:

Moroshkina, M. V., & Rezanova, L. V. (2021). Financial And Insurance Market Trends. In D. S. Nardin, O. V. Stepanova, & V. V. Kuznetsova (Eds.), Land Economy and Rural Studies Essentials, vol 113. European Proceedings of Social and Behavioural Sciences (pp. 563-568). European Publisher. https://doi.org/10.15405/epsbs.2021.07.68