Program-Targeted Budgeting In Constituent Entities Of The Russian Federation: Implementation Algorithm

Abstract

Currently, in Russia, the emphasis in budgeting has been shifted to planning and evaluating the effectiveness of public spending, Budgeting is generally orientated to the result by measuring the effects obtained. The full implementation of program-targeted budgeting in the budget process is the task for the subjects of the Russian Federation. Program-targeted budgeting represents the allocation of budgetary resources aimed at obtaining significant, quantitatively measurable results and is accompanied by monitoring and control of the process of achieving goals, planned results, as well as ensuring the quality of budget planning. The main goal of targeted budgeting is to increase the utilization efficiency of the state budget resources. State program is the major tool to increase the budget spending efficiency. The transition to targeted budgeting is caused by the state financial resources significant reduction that was the result of lower budget revenues, increased budget deficit and public debt. This article is aimed at the development of an algorithm for the implementation of targeted budgeting in the subjects of the RF. The logical correlation of all stages of program-targeted budgeting at the regional level was determined based on the relevant regulatory framework analysis. The study resulted in the construction of an algorithm for targeted budgeting in the RF constituent entities. This algorithm provides transparency and effectiveness of program-targeted budgeting and reflects the logical sequence of its main stages.

Keywords: Budget policyexpenditure planningprogram-target budgetingpublic financesefficiencyalgorithm

Introduction

Over the past few years, the goal of Russia's budget policy has been to introduce a program-targeted method for planning public spending. However, the transition to program-targeted budgeting is a rather complicated process, which requires restructuring the public administration system and organizing the budget process, strengthening the autonomy and responsibility of the ministries and departments involved in implementing state programs. With the proper organization of program-targeted budgeting, the quality of budget funds management improves, the processes of formation, implementation and monitoring of state programs are significantly simplified, the effectiveness of public spending is increased ( Mulendeeva, Glukhova, & Glukhov, 2019). Many Russian regions, including the Samara region, are conducting active rule-making activities to introduce targeted budgeting into strategic planning. Understanding the content of the main stages of program-targeted budgeting in the constituent entities of the Russian Federation will contribute to the transparency and efficiency of budget spending.

Problem Statement

Program budgets have been used in Russia since 2010. At this time, budget planning was transformed into program-targeted budgeting. In modern Russian economic literature there are no studies reflecting the content of program-targeted budgeting at the regional level and the logical sequence of its main stages. In this regard, there is a need to develop an algorithm for implementing targeted budgeting in the subjects of the Russian Federation in order to ensure its transparency and efficiency.

Research Questions

This study aims to solve the following research tasks:

To study the regulatory framework of targeted budgeting;

To determine the logical sequence of the implementation of targeted budgeting in the constituent entities of the Russian Federation;

To identify the main participants in targeted budgeting at the regional level;

To develop an algorithm for the implementation of targeted budgeting in the constituent entities of the Russian Federation.

Purpose of the Study

The major purpose of the study is to develop an algorithm for the implementation of targeted budgeting in the constituent entities of the Russian Federation. This requires a study of the regulatory framework for targeted budgeting in the regions of Russia This framework determines the sequence of the main stages of budget planning based on the targeted program method. The algorithm helps to increase the transparency of program-targeted budgeting and increase the efficiency of spending state budget funds.

Research Methods

The methodologically and theoretically the study is based on academic works of domestic and foreign economists in the field of research on targeted budgeting, federal and regional legal acts regulating the implementation of targeted budgeting. The methodology of the study is comprised of the general scientific set of methods: systems and comparative analysis methods, generalization and grouping methods, factor analysis method. To build an algorithm for program-targeted budgeting, a graphical method was used.

Findings

Reviewing the literature

The study of budget planning based on the program-targeted method has been the subject of many works by domestic and foreign economists. The literature review revealed that all researchers agree that program-targeted budgeting contributes to an increase in the efficiency of budget expenditures at all levels. Dyrina and Bannova ( 2015), Altundemir and Gonca ( 2016) note that more efficient use of financial resources is one of the most important tasks of the state budget policy. According to Lytvynchenko ( 2014), the effective implementation of fiscal policy requires the methodologically sound management of the state budget based on the program method.

Targeted budgeting helps the budget process participants to efficiently distribute limited financial resources between various government programs ( Ellul, 2018). The distribution of budgetary funds for the implementation of state programs will make it possible to more clearly determine the relationship between expected results and costs ( Leksin & Porfiryev, 2016). Thus, the socio-economic development of the country depends on establishing the correct budget indicators in state programs ( Melnichuk, 2015).

Results

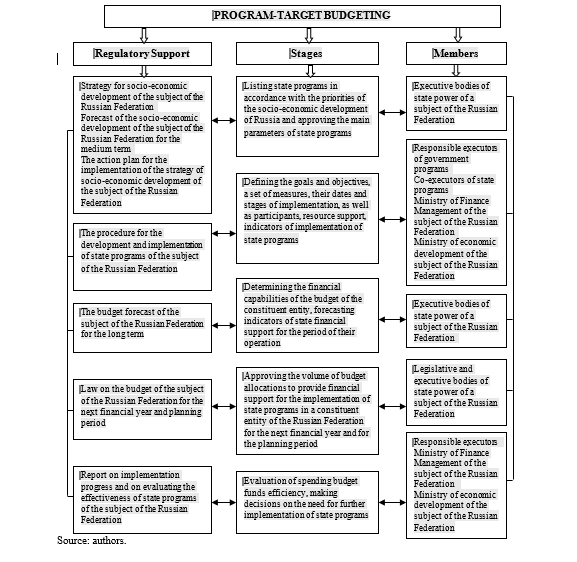

The appropriate decree (Decree of the Government of the Russian Federation of 02 August 2010 N 588. The procedure for the development, implementation and evaluation of the effectiveness of state programs of the Russian Federation) and guidelines (Order of the Ministry of economic development of the Russian Federation of 16 September 2016 N 582.Guidelines for the development and implementation of state programs of the Russian Federation) regulate the process of developing and implementing government programs in Russia is regulated by. The development of state programs at the regional level is regulated by the documents in the field of strategic planning ( Brusca & Labrador, 2016). According to Russian law ( Federal law of 28 June 2014 N 172-FL. On strategic planning in the Russian Federation, 2014), in the Samara region such documents are:

“Strategy social and economic development Samara region for the period until 2030” (Decree of the government of the Samara region of 12 July 2017 N 441. Strategy social and economic development Samara region for the period until 2030) reflects the priorities of the socio-economic policy of the constituent entity of the Russian Federation, The state programs are developed in accordance with the priorities

“The Forecast of socio-economic development of the Samara region for 2019-2021” (Decree of the government of the Samara region of 31 October 2018 N 620. The Forecast of socio-economic development of the Samara region for 2019-2021) indicates the parameters of state programs;

“The action plan of measures for the implementation in 2018 - 2020 (stage I) of the Strategy for socio-economic development of the Samara region for the period until 2030” (Order of the government of the Samara region of 29 December 2018 N 1080-o. The action plan of measures for the implementation in 2018 - 2020 (stage I) of the Strategy for socio-economic development of the Samara region for the period until 2030) establishes a list of state programs, the implementation of which serves the long-term goals of socio-economic development of the RF constituent entity at each stage of the strategy implementation.

A budget forecast of the subject of the Russian Federation for a long-term period (12 years or more) is developed based on the forecast of region socio-economic development. It contains a forecast of the regional budget main characteristics, the limitations for the financial support of state programs, a forecast of costs for the implementation of non-programmed activities of state authorities of a constituent entity of the Russian Federation. The "Budget forecast of the Samara region for the long term until 2030" (Decree of the government of the Samara region of 17 February 2017 N 104. Budget forecast of the Samara region for the long term until 2030) is adopted in the Samara region.

The annual financial support for the implementation of state programs regarding expenditure obligations of a constituent entity of the Russian Federation is carried out at the expense of budgetary allocations of the regional budget, the amount of which is approved by the law on the budget of the constituent entity of the Russian Federation for the next financial year and planning period ( Budget code of the Russian Federation of 17 July 1998 Federation).

State programs of the RF constituent entities may provide for subsidies from the federal budget as financial support. The subsidies are to achieve goals on the joint subjects’ and regions’ issues ( Knyazeva & Lvova, 2015).

In addition, the state program should contain information on the forecast expenses of these organizations if the implementation of the regional state program involves the participation of state organizations, business entities with the participation of state capital, scientific, public and other organizations, extra budgetary funds.

The state program may provide for the institutional provision of services to individuals or legal entities. In this case, the program should reflect the forecast values of the consolidated indicators of state tasks at the stages of its implementation. Implementation of government programs is based on government contracts. State contracts establish the rights and obligations of the customer via the state authority and the executor, regulate relations between them in the process of fulfilling the state contract, including monitoring by the customer ( Kovaleva, Glukhova, & Valieva, 2017).

Russian legislation requires continuous monitoring and evaluation of the effectiveness of the implementation of state programs. The results of the programs are reflected in the combined annual report on the implementation and evaluation of the effectiveness of state programs of the subject of the Russian Federation (Decree of the Government of the Russian Federation of 02 August 2010 N 588. The procedure for the development, implementation and evaluation of the effectiveness of state programs of the Russian Federation).

A thorough study of the relevant regulatory framework allowed us to develop an algorithm that provides a logical relationship between all stages of program-targeted budgeting in the constituent entities of the Russian Federation. Theoretically we have identified 5 main stages of program-targeted budgeting in the constituent entity of the Russian Federation. The content of each stage is determined by the corresponding regulatory legal act. Also, each stage of the program-targeted budgeting involves the participation of certain state authorities of the constituent entity of the Russian Federation in it (Figure

Conclusion

Overall this study provides an account of regulatory framework for the development and implementation of government programs in the constituent entities of the Russian Federation. This analysis allowed us to determine the algorithm of target-targeted budgeting at the regional level. The practical significance of the research results lies in the fact that this algorithm determines the logical sequence of stages of program-targeted budgeting, which ensures its transparency and the possibility of increasing the efficiency of budget expenditures of the constituent entities of the Russian Federation.

The findings of this study provide important practical implications regarding the capacity of the algorithm to determine the logical sequence of stages of program-targeted budgeting. The algorithm ensures the transparency of the budgeting and the possibility of increasing the efficiency of budget expenditures of the constituent entities of the Russian Federation.

References

- Altundemir, M. E., & Gonca, G. G. (2016). Performance-based budgeting on strategic planning: The case study in Turkish higher education system. New Trends and Issues Proceedings on Humanities and Social Sciences, 3, 263-270.

- Brusca, I., & Labrador, M. (2016). Budgeting in the public sector. In A. Farazmand (Ed.), Global Encyclopedia of Public Administration, Public Policy, and Governance. Springer, Cham. Retrieved from: https://link.springer.com/referenceworkentry/10.1007/978-3-319-20928-9_2361 Accessed: 05.11.2019.

- Budget code of the Russian Federation of 17 July 1998 Federation. Retrieved from: Retrieved from: http://www.consultant.ru/document/cons_doc_LAW_19702/ Accessed: 20.11.2019.

- Decree of the Government of the Russian Federation of 02 August 2010 N 588. The procedure for the development, implementation and evaluation of the effectiveness of state programs of the Russian Federation. Retrieved from http://www.consultant.ru/document/cons_doc_LAW_103481/ Accessed: 20.11.2019.

- Decree of the government of the Samara region of 12 July 2017 N 441. Strategy social and economic development Samara region for the period until 2030. Retrieved from https://economy.samregion.ru/upload/iblock/25a/Strategiya-SO_2030.pdf - Accessed: 20.11.2019.

- Decree of the government of the Samara region of 31 October 2018 N 620. The Forecast of socio-economic development of the Samara region for 2019-2021. Retrieved from https://economy.samregion.ru/ upload/iblock/473/Postanovlenie-Pravitelstva-Samarskoy-oblasti-ot-31.10.2018-_-620.pdf Accessed: 20.11.2019.

- Decree of the government of the Samara region of 17 February 2017 N 104. Budget forecast of the Samara region for the long term until 2030. Retrieved from http://docs.cntd.ru/document/434611714. Accessed: 20.11.2019.

- Dyrina, E. N., & Bannova, K. A. (2015). Improvement in implementation of fiscal policy of Russia. In I. Ardashkin, A. Bogdan, N. Martyushev (Eds.), International Conference on Research Paradigms Transformation in Social Sciences 2014. Procedia - Social and Behavioral Sciences 166 (pp. 58 – 61). Amsterdam: Elsevier.

- Ellul, L. (2018). Results and output-based budgeting. In Farazmand A. (Ed.), Global Encyclopedia of Public Administration, Public Policy, and Governance. Springer, Cham. Retrieved from: https://link.springer.com/referenceworkentry/10.1007/978-3-319-31816-5_2262-1#howtocite. Accessed: 05.11.2019.

- Federal law of 28 June 2014 N 172-FL. On strategic planning in the Russian Federation. Retrieved from: http://www.consultant.ru/document/cons_doc_LAW_164841/ Accessed: 12.12.2019.

- Knyazeva, E. G., & Lvova, S. D. (2015). Program-targeted approach to the formation and implementation of financial support for a new quality of life for Russian citizens. Economics and Entrepreneurship, 10(2), 669-671.

- Kovaleva, T. M., Glukhova, A. G., & Valieva, E. N. (2017). The role of the contract system in the efficient spending of budget funds. Economics and Entrepreneurship, 8(3), 1177 - 1182.

- Leksin, V. N., & Porfiryev, B. N. (2016). Evaluation of the effectiveness of government programs of socioeconomic development of regions of Russia. Studies on Russian Economic Development, 27, 418-428.

- Lytvynchenko, G. (2014). Programme management for public budgeting and fiscal policy. In M. Radujković, M. Vukomanović, R. Wagner (Eds.), 27th International Project Management Association), World Congress. Procedia - Social and Behavioral Sciences, 119 (pp. 576 – 580). Amsterdam: Elsevier.

- Melnichuk, N. (2015). Budget planning in financial management. Baltic Journal of Economic Studies, 1(2), 95-100.

- Mulendeeva, L. N., Glukhova, A. G., & Glukhov, G. V. (2019). Development model for program-target budgeting in constituent entities of the Russian Federation. In V. Mantulenko (Ed.), Eurasia: Sustainable Development, Security, Cooperation – 2019. SHS Web of Conferences, 71 (02003). Les Ulis: EDP Sciences.

- Order of the Ministry of economic development of the Russian Federation of 16 September 2016 N 582. Guidelines for the development and implementation of state programs of the Russian Federation. Retrieved from http://base.garant.ru/71508802/ Accessed: 05.11.2019.

- Order of the government of the Samara region of 29 December 2018 N 1080-o. The action plan of measures for the implementation in 2018 - 2020 (stage I) of the Strategy for socio-economic development of the Samara region for the period until 2030. Retrieved from https://economy.samregion.ru/ upload/iblock/95e/Plan-meropriyatiy.pdf Accessed: 20.11.2019.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

01 April 2020

Article Doi

eBook ISBN

978-1-80296-081-5

Publisher

European Publisher

Volume

82

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1004

Subjects

Business, innovation, management, management techniques, development studies

Cite this article as:

Mulendeeva, L. N. (2020). Program-Targeted Budgeting In Constituent Entities Of The Russian Federation: Implementation Algorithm. In V. V. Mantulenko (Ed.), Problems of Enterprise Development: Theory and Practice, vol 82. European Proceedings of Social and Behavioural Sciences (pp. 714-720). European Publisher. https://doi.org/10.15405/epsbs.2020.04.90