The System Of Economic Methods As An Instrument For Business Effectiveness Growth

Abstract

One of the main reasons for the broad use of economic methods in business activities of enterprises is the complexity and large variety of business forms that force managers to come to recurring operational decisions. Economic methods stimulate those responsible to take initiative based on material interest and encourage to make effective managerial decisions. Economic methods are constantly developing and adapt to changing market economy. The use of economic methods facilitates the research of markets and allows assessing the demand for the products of an enterprise, determining whether this demand can be satisfied and compare the demand and the offer. This helps business to establish both short and long-term strategy. The importance of this research results from the necessity to asses the economic effectiveness of business and the ways for risk-hedging. The aim of the research is to study the concept of business development based on economic analysis. Management always means an impact on managed objects to obtain the necessary results. In terms of business the managed objects are organizational structures or departments, carrying out business activities. The results of business activities depend on the character of an impact on structural units and on how effective these entities in organizing their work. The effectiveness of units can be determined based on performance indicators that should assess the completeness, quality and timeliness of unit operations as well as evaluate the contribution of each unit into the results of business activities.

Keywords: Economic performance indicatorsmethodscommercial estimations

Introduction

Modern business is seriously changing in the way that its participants act based on the principle of full equality of partners, economic independence, strict financial responsibility and liability for commitments made.

The traditional idea of business as only selling goods is disappearing. Nowadays business activities are a combination of processes aimed for management and support of these activities. Business needs a special organizational structure to carry out commercial operations. This organizational structure should match the specificity and character of the functions being carried out. Such an approach will provide the most effective way to manage commercial activities.

The research analyses the ways to organize business activities effectively in the context of the modern Russian economy. The subject of this research is the possible measures for preventing the risks in the commercial activities of enterprises.

The work determines the essence, aims, and tasks of business activities in enterprises, describe economic methods in business activities of enterprises, define the place of economic methods in the system of methods used to make managerial decisions in enterprises.

Problem Statement

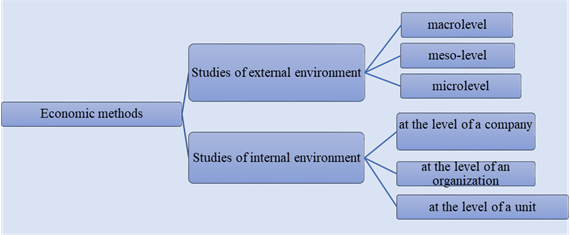

To enhance the effectiveness, bearing objective external factors and subjective internal factors in mind, economic methods in the agricultural business seek to determine requirements and form qualitative changes in business activities of an organization (fig.

The changes in macroeconomy aimed at improving the positions of enterprises in a highly competitive market are caused by the necessity to use the advances of science and engineering in the agricultural business (Kuznetsov, Soldatova, Ignatova, & Arkhipov, 2014). For example, agriculture has progressed in financial and economic indicators, but they are still lower than in developed countries, especially those in similar natural and climatic conditions. (Frolova, Pogorelova, Likhatskaya, & Matytsyna, 2017). The importance of economic methods is that they simultaneously impact the economic interests of a consumer (using flexible prices, credit products, and additional services) and the personnel of agricultural enterprises (by a system of payments, profit-sharing and other economic mechanisms for effective business activities). In this case, only the goals and the general strategy of business development are defined to search for the most suitable ways of achieving results (Kosyakova, 2017).

The improvement of management based on the rational use of economic methods is the most important constituent of effective business activities, stability, and competitiveness of enterprises in the modern market. (Frolova, Pogorelova, Lebedeva, Matytsyna, & Polenova, 2018). The assessment of business activities based on economic methods is one of the main directions in the work of organizations.

In a fundamental way, the system of economic methods is based on management instruments and contains direct centralized accounting, cost accounting, planning, financing, pricing, economic stimulation, financial analysis and etc. (Tebekin, 2017).

Research Questions

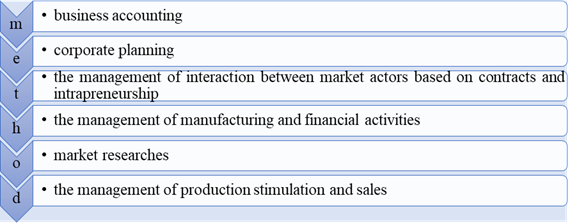

The effectiveness, financial stability, and competitiveness of an agricultural business depend on management improvement that is based on economic methods understood as a combination of means and instruments influencing on the creation of a favourable climate for the development and functioning of a business (Ignatova & Pavlyukova, 2017). The main methods applied in the agricultural business are represented in fig.

Business accounting is an active method of business containing and implementing management functions and mechanisms aimed at balancing expenditures and results as well as ensuring the efficiency of manufacturing. Corporate planning deals with budgeting and plans for business development (Bespamyatnova & Lichatskaya, 2016).

Adaptive planning of manufacturing and development of an organization is recommended when the market environment is dynamic and unpredictable. In this case, the in-company plans are produced based on the from future to past principle (Matytsyna, 2016).

The management of the business effectiveness highly depends on the transition to the relationships with counterparties based on agreed prices established on a competitive basis (Besolov & Kelehsaev, 2016).

Marketing is also an important management instrument. It is used to analyse the situation and provide management with information that is necessary to make effective decisions regarding strategical planning accounting and controlling business activities. Nowadays businesses use such stimulating means as salary, bonuses, financial aid, perks and etc. (Andreychenko, Bespamyatnova, & Lichatskaya, 2016).

Purpose of the Study

Financial management should stimulate the revenue growth and improvement of other financial indicators. It should enhance the development of business and elevate its use of a budget as well as financial control of reproduction processes. The main instruments for business management are prices, taxes, and loans as well as innovations.

Research Methods

One of the main issues when planning business is the choice of a taxation system. In the case of an agricultural business, the choice is limited to either the single agricultural tax or the general tax system or the simplified tax system with choosing a taxation subject. If an organization chooses the single agricultural tax, it pays VAT to a supplier, but the tax code of the Russian Federation limits the rights of organizations for the deduction of the accepted VAT from the budget (Anopchenko & Netkacheva, 2018). The simplified comparison of the three taxation systems can be found in table

Thus, an agricultural enterprise can choose among 4 variants of taxation. The simplified tax system is the most disadvantaged as the rate of the single agricultural tax is much lower. The single agricultural tax is good for small organizations that don’t employ highly qualified accountants (Frolova, 2017).

If an organization chooses the single agricultural tax, it pays VAT to a supplier, but the tax code of the Russian Federation limits the rights of organizations for the deduction of the accepted VAT from the budget. For example:

– The general tax system. An organization pays 59 million roubles to suppliers for goods and services, including 9 million VAT (18%). At the same time, it gets 132 million roubles for selling its products, including 12 million VAT (10%). The total income (other expenses excluded) – 73 million roubles. (The difference between selling and buying is 70 million roubles without VAT, while the difference between the VAT to be refunded and the VAT to be paid is 3 million roubles). Thus, the gross profit is 73 million roubles.

– The single agricultural tax. An organization pays 59 million roubles to suppliers for goods and services and gets 120 million roubles from selling products. The tax base is 61 million roubles. The rate of the single agricultural tax is 6%. The tax is 3 660 thousand roubles. The profit after taxation is 57.34 million roubles. The examples show that the general tax system has more advantages over the single agricultural tax (the gross profit is higher by 15.66 million roubles when using the general tax system) (Pogorelova, 2018).

Findings

The narrow group of manufacturers whose agricultural profits are higher than 70% can enjoy a low tax rate and simplified standards of accounting and tax reporting. The general system is good for big businesses that export their products. For agricultural enterprises, the rate of the income tax related to selling their raw and processed products is 0%. (Frolova, Panfilova, Matytsyna, Lebedeva, & Likhatskaya, 2016).

Philosophy is the scientific basis for all economic methods in business. The activities of any commercial organization are analysed according to the dialectic laws, i.e. all processes are studied in relationship and dynamics.

Each business process is a combination of many elements. Economic analysis is aimed at studying the conversion of quantity into quality, the old quality into a new one. Business processes are studied with a combination of analysis and synthesis.

Conclusion

Thus, the most important element to achieve the efficiency, financial stability and competitiveness of business in the modern market is the improvement of management based on the rational use of economic methods.

Economic methods used in business activities vary. They are classified based on different criteria, in particular forms, methods and trade instruments. The effectiveness of latter results from the sophistication of applied mechanisms that in turn depends on the implementation of main principles for their forming and improvement such as adequacy, comprehensiveness, adaptation, and competency.

The success of modern economic changes suggests the need to search for the most effective norms, methods, and instruments of trade, mechanisms to optimize buying and selling mechanisms and searching for factors of new growth. The diploma work tried to solve some principle problems in this sphere which will increase the efficiency of commercial activities of an enterprise.

References

- Andreychenko, N. V., Bespamyatnova, L. P., & Likhatskaya, E. A. (2016). Neobhodimost HR-brendinga y upravlencheskogo ucheta v systeme upravleniya personalom. Rostov-on-Don: IE Bespamyatnov S.V.

- Anopchenko, T. Yu., & Netkacheva, M. A. (2018). Tendentsii razvitiya agropromishlennogo kompleksa. In Upravlenie v usloviyakh globalnikh mirovikh transformatsiy: economica, politica, pravo. Proceedings of the international conference (pp. 19–21).

- Besolov, F. D., & Kelehsaev, H. T. (2016). Rol y znachenie economicheskih metodov upravleniya v selskom hoziaystve RSO-Alaniya. Journal of Proceedings of of the Gorsky SAU, 47(2), 149–154.

- Bespamyatnova, L. P., & Likhatskaya, E. A. (2016). Razvitie teorii y metodiki strategicheskogo ucheta. Rostov-on-Don: IE Bespamyatnov S.V.

- Frolova, I. V., Panfilova, E. A., Matytsyna, T. V., Lebedeva, N. Y., & Likhatskaya, E. A. (2016). Integration of the corporate reporting instruments of situational and matrix modeling. Social Sciences and Interdisciplinary Behavior. In Proceedings of the 4th International Congress on Interdisciplinary Behavior and Social Science, ICIBSOS 2015 (pp. 317–324). Bali: CRC Press.

- Frolova, I. V., Pogorelova, T. G., Lebedeva, N. U., Matytsyna, T. V., & Polenova, A. U. (2018). Improving the efficiency of hotel business through the use of tax alternatives. Financial and Economic Tools Used in the World Hospitality Industry. In Proceedings of the 5th International Conference on Management and Technology in Knowledge, Service, Tourism and Hospitality (pp. 29–34). Bali: CRC Press.

- Frolova, I. V., Pogorelova, T. G., Likhatskaya, E. A., & Matytsyna, T. V. (2017). Harmonization of the tax portfolio of an organization by means of situational matrix modeling. In Managing Service, Education and Knowledge Management in the Knowledge Economic Era. Proceedings of the Annual International Conference on Management and Technology in Knowledge, Service, Tourism and Hospitality, SERVE 2016 (pp. 69–74). Bali: CRC Press.

- Frolova, I.V. (2017). Problemy razvitiya autsorsingovikh uslug buhgalterskogo y nalogovogo ucheta v ramkah sozdaniya autsorsingovoy firmi po obsluzhivaniyu selskokhozyaistvennikh proizvoditeley. In Nauchnie idei v conekste modernizatsii sovremennogo obshestva International conference proceedings (pp. 117–122).

- Ignatova, T. V., & Pavlyukova, A. V. (2017). Upravlenye konkurentnymy preimushestvamy organisatsiy yuga Rossii. Competitiveness in the Global World. Economics, Science, Technology, 11(58), 1171–1173.

- Kosyakova, L. N. (2017). Prioritety innovatsionnoy politiki v APK Rossii. Nauchnoye obespechenye razvitiya APK v usloviyakh import zamescheniya. In Proceedings of the international conference “Nauchnoye obespechenye razvitiya selskogo khozyaistva y snizheniya technologicheskih riskov v prodovolstvennoy sfere”, part II (p. 130). St.-Petersburg: SPBGAU.

- Kuznetsov, В., Soldatova, I., Ignatova, Т., & Arkhipov, А. (2014). State support of russian agriculture entering the global market: global and national priorities. Deutshland: Research collective monography LAP LAMBERT.

- Matytsyna, T. V. (2016). Otraslevie kontury sovremennikh informatsionnikh technologiy: cpetsifica functsionirovaniya y traectoria razvitiya. Rostov-on-Don: IE Bespamyatnov S.V.

- Pogorelova, T. G. (2018). Vliyanie economicheskih metodov na povishenie effectivnosty agrarnogo biznesa. Competitiveness in the Global World. Economics, Science, Technology, 6–2, 111–113.

- Tebekin, A. V. (2017). Economicheskie metody v systeme metodov prinyatia upravlencheskih resheniy v menedzhmente. Moscow Witte University Bulletin, ser. 1: Economics and management, 3(22), 54–59.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

28 December 2019

Article Doi

eBook ISBN

978-1-80296-075-4

Publisher

Future Academy

Volume

76

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-3763

Subjects

Sociolinguistics, linguistics, semantics, discourse analysis, science, technology, society

Cite this article as:

Pogorelova*, T., Bespamyatnova, L., Brazhka, O., Pavliukova, A., & Maksimenko, A. (2019). The System Of Economic Methods As An Instrument For Business Effectiveness Growth. In D. Karim-Sultanovich Bataev, S. Aidievich Gapurov, A. Dogievich Osmaev, V. Khumaidovich Akaev, L. Musaevna Idigova, M. Rukmanovich Ovhadov, A. Ruslanovich Salgiriev, & M. Muslamovna Betilmerzaeva (Eds.), Social and Cultural Transformations in the Context of Modern Globalism, vol 76. European Proceedings of Social and Behavioural Sciences (pp. 2602-2608). Future Academy. https://doi.org/10.15405/epsbs.2019.12.04.349