Economic Sustainability As An Element Of The Company Efficiency Mechanism

Abstract

The article studies mechanisms for improving the economic efficiency of enterprises. Economic sustainability is a multifaceted socio-economic phenomenon which is dependent on market relations. There are economic, financial and credit, market, anti-crisis, management mechanisms. The key task of economic management is creation conditions for the development of economic mechanisms as an integral part of the complex economic system. Any economic activity is determined by the need to implement interests of direct and indirect participants. The main and most important condition for the economic efficiency of enterprises is their economic stability under constant dynamic transformations of business conditions. The authors conclude that economic sustainability as an element of the mechanism of economic efficiency of enterprises has several implementation directions. The main directions are as follows: the comprehensive study of the enterprise system as a whole taking into account internal and external factors; the study of the main elements of the enterprise (material and technical resources of the enterprise, financial resources, etc.). These approaches will contribute to the efficiency of economic sustainability mechanisms. The research subject is economic sustainability as a key element of the mechanism of economic efficiency of modern enterprises in new economic conditions. The aim is to develop directions of the mechanism for ensuring economic sustainability of enterprises operating in modern dynamic business conditions. The methodological basis is works by foreign and Russian scientists which are a theoretical and methodological platform for research. The systematic approach is used to analyze the enterprise as an object of sustainable development.

Keywords: Economic mechanismefficiencyeconomic sustainability

Introduction

The main task economic management is development of an economic mechanism as an integral element of the complex economic system. However, large-scale production needs a scientific management system because it is based on the division of labor. There is no consensus on the concepts "economic mechanism" and "efficiency mechanism." It is very important to determine the meaning of the word “mechanism” which forms a basis for the economic categories.

Problem Statement

It is necessary to develop of a mechanism that will contribute to efficient development of enterprises.

Research Questions

The research subject is economic sustainability as a key element of the mechanism of economic efficiency of modern enterprises in the new economic conditions.

Purpose of the Study

The aim is to develop directions of the mechanism for ensuring economic sustainability of enterprises operating in modern dynamic business conditions.

Research Methods

The methodological basis is works by foreign and Russian scientists which are a theoretical and methodological platform for research. The systematic approach is used to analyze the enterprise as an object of sustainable development.

Findings

It is necessary to develop of a mechanism that will contribute to efficient development of enterprises.

The main task is to develop an economic mechanism as an integral part of the complex economic system. Large-scale production needs a scientific management system because it is based on the division of labor.

There is no consensus on the concepts "economic mechanism" and "efficiency mechanism." It is very important to determine the meaning of the word “mechanism” which forms a basis for the economic categories

The study of economic mechanisms began in the 1960s. Gurvits defines a mechanism as a process of interaction of its constituent elements (as cited in Izmalkov, Sonin, & Yudkevich, 2008). Kulman (1993) defined the concept of economic mechanism as a process with a certain result, and isolated various types of economic mechanisms depending on the economic conditions.

Thus, the “economic mechanism” is defined either as a process with its inherent forms, methods and institutions, or as a system of interrelated elements. The theory of economic mechanisms allows us to describe the patterns of economic processes and understand the nature of the economic phenomena.

Researchers distinguishing the economic and organizational components deal with the organizational and economic mechanism, although the authors describing the economic mechanism do not deny its organizational component which manifests itself both in the function of organizing processes and in regulating institutions. Any economic activity cannot be carried out without its organizational design, and the management process cannot be carried out without organizational and planning functions. The economic mechanism manifests itself through specific economic interests with participation of the subjects which are represented in various organizational forms. The economic mechanism does not need to focus on the organizational component. The concept “organizational and economic mechanism” causes a confused understanding of these concepts and their duplication.

The term "efficiency" is used in relation to the sphere of production as achievement of a specific production goal in a timely manner taking into account available resources.

Based on the modern methods applied to the new economic conditions, market relations provide the opportunity to independently manage their activities, resources and labor results and take responsibility for their own decisions. Therefore, the efficiency of enterprises depends on the efficiency of its operation.

Efficiency of the enterprise is measured by absolute and relative indicators. There are indicators of economic effects and economic efficiency.

There are the following types of efficiency: production and economic, technological, socio-economic and environmental-economic.

Some experts focus on only economic and social types: economic efficiency can be determined by comparing the result obtained; social efficiency involves creation of the best conditions for reproduction of labor and growth of the welfare.

In his work "Scientific basis for the formation of economic mechanisms: forms, types, types", Semin (2012) says that "diversity of economic mechanisms reflects economic conditions" (p. 10).

Various mechanisms (economic, financial-credit, market, anti-crisis, management) are distinguished due to various economic conditions and individual economic processes.

If we proceed from the fact that “mechanisms are systems of interconnections of economic phenomena that arise in certain conditions under the influence of an initial impulse, there are so many economic mechanisms as there are different impulses in each system of interrelated phenomena under given conditions” (Kulman, 1993, p. 190).

If we talk about the economic mechanism of enterprise development efficiency, it should be assumed that any economic activity is determined by the need to implement interests of direct and indirect participants. These may be economic, social, cultural, and environmental interests. Their implementation is reduced to various forms of production, exchange, distribution of goods and services which depend on the level of development of society, productive forces and production relations.

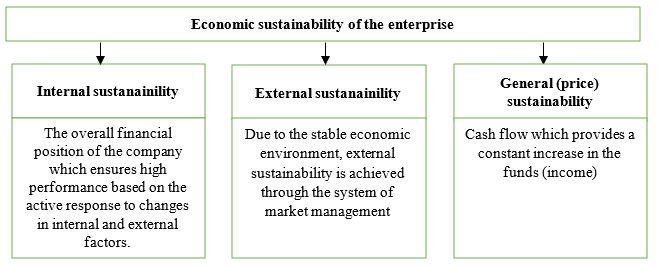

Thus, the efficiency of the economic mechanism of sustainability and enterprise development is influenced by external and internal factors and economic conditions. In the work “Economic Sustainability and Enterprise Development”, Gerasimov and Berezovsky (2018) classify the types of economic sustainability of enterprises depending on the factors affecting it (Figure

“Economic sustainability” is a state of the evolving business system in the conditions of equilibrium of all its elements. If we consider the concept of economic sustainability in relation to an organization, it is an ability and aspiration of the organization to maintain the optimal ratio of all the most important components in the process of its development.

The category “economic sustainability” describes all aspects of the business system in dynamics. It is an important integral indicator that combines such indicators of economic conditions as the level of project profitability, financial independence, economic security, etc. If we consider economic security, it is one of the key factors of business activities. The emergence of this concept is due to the desire of organizations to protect themselves against external and internal threats of the competitive environment. These threats include information leakage, loss of business reputation, etc.

It is necessary to pay more attention to the concept “economic security”. The economic security is a strategy aimed at increasing the efficiency of activities, achieving a high level of economic profit. The efficiency of the organization is characterized by low cost production. Enhancement of the efficiency increases economic security. It is necessary to reduce budget expenditures, use the government pressure on local authorities and other public organizations that work in partnership with each other in order to make decisions (Zabavskaya, 2018).

The key to survival and the basis for stability of the enterprise is its economic stability which is influenced by various factors:

- global conditions (the state of the world economy, globalization of the economy, external threats, participation in cross-border and global cooperation, regional integration);

- market relations (the market infrastructure, privatization, state regulation, state tax policies and tax incentives);

- materialized physical capital (land quantity and quality, volume, structure, efficiency of fixed assets, etc.);

- human capital (the size and structure of the population, the structure of employment, cultural and professional levels);

- financial resources of the enterprise;

- non-economic factors (political, socio-cultural environment).

The state can influence the economic sustainability of enterprises through tax policies. In developed countries, attention is paid to the tools of state influence on the economic development of enterprises. The role of the state may be different.

There are approaches that distinguish the two poles of state policies in the area of supporting economic development: the state does not interfere (the United States and the United Kingdom); the state stimulates innovation and investment activities (France and Japan). Among the methods of state influence on the economic development of enterprises are tax policies which belong to indirect methods of regulation. Tax incentives ensure objectivity of the criteria for providing state support which is important in terms of providing equal conditions for development of competitive relations. The dominance of indirect regulation of economic activities of enterprises is a modern trend of public administration. Tax tools are as follows:

- tax incentives for investing in enterprises that are carried out innovative activities;

- investment tax credit;

- reduction of tax rates;

- tax holidays for profit derived from implementation of innovative projects;

- tax zones with special preferential taxation within the technoparks (Gerasimov & Berezovsky, 2018).

Thus, “the economic sustainability of an enterprise is one of the development factors. The role of the analysis of economic sustainability is crucial” (Alimova, 2010, p. 91).

The assumption that the enterprise is constantly changing is confirmed by the cyclical development of any system (enterprise). The impact of external and internal factors on economic activities of the system (enterprise) can be positive (movement towards the final goal) and negative. Therefore, the economic system should have elements which help modify it in new market conditions and ensures sustainable development. (Tsybareva, 2008, p. 200)

Conclusion

Economic sustainability as an element of the mechanism of economic efficiency of enterprises should have certain directions of implementation.

The main areas of the mechanism of economic sustainability of enterprises are as follows:

- comprehensive study of the enterprise system as a whole taking into account internal and external factors;

- the study of the main elements of the enterprise (material and technical resources of the enterprise, financial resources, etc.);

These approaches will contribute to the effective operation of the mechanism for ensuring the economic sustainability of enterprises.

References

- Alimova, E. T. (2010). Identify the factors that ensure the economic sustainability of enterprises. Bulletin of Astrakhan State Technical University. Economy series, 89–91.

- Gerasimov, E. L., & Berezovsky, V.V. (2018). Economic sustainability and development of enterprises. Methods and technologies of accounting, analysis and management. Minsk: Publishing house: LLC "Kovcheg".

- Izmalkov, S., Sonin, K., & Yudkevich, M. (2008). Theory of Economic Mechanisms. Economic issues, pp. 4–26.

- Kulman, A. (1993). Economic mechanisms. Moscow: Publishing Group “Progress”; "Univers".

- Semin, A. N. (2012). Scientific basis for the formation of economic mechanisms: forms, types. Agricultural and food policy of Russia, 5–12.

- Tsybareva, M. E. (2008). The concept of "economic sustainability" of the company. Bulletin of SSU, 195–202.

- Zabavskaya, A. V. (2018). Economic sustainability of the organization. Strategic directions of socio-economic and financial support for the development of the national economy. Minsk: Publishing house: LLC "Law and Economics".

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

28 December 2019

Article Doi

eBook ISBN

978-1-80296-075-4

Publisher

Future Academy

Volume

76

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-3763

Subjects

Sociolinguistics, linguistics, semantics, discourse analysis, science, technology, society

Cite this article as:

Abdulkadyrova, M., Betilgiriev, M., Israilova, Y., Israilov*, M., & Tibilova, A. (2019). Economic Sustainability As An Element Of The Company Efficiency Mechanism. In D. Karim-Sultanovich Bataev, S. Aidievich Gapurov, A. Dogievich Osmaev, V. Khumaidovich Akaev, L. Musaevna Idigova, M. Rukmanovich Ovhadov, A. Ruslanovich Salgiriev, & M. Muslamovna Betilmerzaeva (Eds.), Social and Cultural Transformations in the Context of Modern Globalism, vol 76. European Proceedings of Social and Behavioural Sciences (pp. 1378-1383). Future Academy. https://doi.org/10.15405/epsbs.2019.12.04.186