The Impact of Business Intelligence Capabilities on Organisational Performance in Malaysia

Abstract

In today’s dynamic business environment, business organisations are driven by uncertainties and turbulence in market trends, in developed and emerging economies alike. Strategic agility allows businesses to adapt fast to changes and to be cost-effective in vigorous business settings. Industry Revolution 4.0 has created new challenges for Business Intelligence (BI) to analyse and solve problems efficiently, thus allowing senior managers to make fast decisions. The value of such BI projects on businesses depends largely on the BI capabilities. Previous researches have shown that BI capabilities have been considered an important function that enhances organisational performance, however, the impact of BI capabilities on organisational performance remains poorly understood in emerging economies such as Malaysia. The main objective of this paper is to present an integrated conceptual model which first examines the influence of Information Technology (IT) governance on BI capabilities moderated by risk management; and consequently the impact of BI capabilities on organisational performance moderated by the business strategy alignment. This conceptual model is developed by synthesising previous-related studies and is based on the Dynamic Capabilities Theory. This paper contributes to the field of organisational performance in the context of BI capabilities, while examining the interplay of IT governance, risk management as well as business strategy alignment in this context. Practically, this paper suggests the importance of IT governance as well as risk management on BI capabilities. It also justifies the crucial role of BI capabilities and business strategy alignment which impact the performance of business organisations in emerging economies.

Keywords: Business intelligenceCapabilitiesRisk managementGovernancePerformanceStrategy alignment

Introduction

Business organisations are driven by uncertainty and turbulence in market trends in today’s dynamic business environment, in developed and emerging economies alike. Global competition is one of the economic factors (Gröger, Kassner, Hoos, & Königsberger, 2016) which caused organisations to redesign production processes with greater adaptability to respond to market demands (Eiskop, Snatkin, Kõrgesaar, & Søren, 2014). At the same time, organisations are faced with decreased budgets each year, and pressure from top management to increase business performance and profitability. Organisations must respond fast to adapt to such changes, and to be innovative and agile (Sharda, Delon, & Turban, 2014). Many business owners face challenges in dealing with data quality due to the increasing numbers of applications and the exponential growth of structured/unstructured data issues relating to making quality decisions (Lee, Kao, & Yang, 2014).

Neuböck and Schrefl (2015) pointed out that manufacturing companies are transforming their business model to mass production of a wide range of customised products to tailor individual customer requirements under the Industrial Revolution 4.0. Organisations must act fast to adapt to such market requirements, with shorter product life cycles and fierce global competition. Businesses must be able to analyse and collect relevant data to determine the market trends and direction in order to stay competitive. Implementing Business Intelligence (BI) systems into an organisation will transform the way of performing and managing business activities and decision making process (Fink, Yogev, & Even, 2017). BI helps to address these issues by providing analytical tools to improve the business decision making (Fink at el., 2017). Ramakrishnan et al. (2016) defined BI as a set of tools and techniques that transform large amount of data from disparate sources. BI will use algorithms and analysis to consolidate these data silos and aggregate these data into meaningful information to support the decision making process and thus improve organisational performance. BI makes use of information and analyses within the business processes to support management in making better quality informed decisions and actions that lead to improved organisational performance.

Surveys found that the Business Intelligence and Analytics (BI&A) development and deployment will remain as one of the top priorities for many organisations and CIOs (Arnott, Lizama, & Song, 2017; Işik, Jones, & Sidorova, 2013). According to Gartner, the market demand for BI&A has grown to US$18.3 billion in 2017, an increase of 7.3% from 2016, and is forecasted to reach US$ 22.8 billion by 2020 (Gartner, 2017). Adoption of BI systems will bring benefits such as savings in cost and time, improvement in information and business processes, better quality decision making and better organisational performance (Wixom et al., 2011). Dresner Advisory Services in their recent survey reviewed that making better decisions, improving operational efficiencies, increasing revenues and gaining competitive advantage are the top four BI objectives of organisations today (Columbus, 2018).

Business Intelligence (BI) Capabilities

Capabilities is an important resource in an organisation in achieving differentiation and competitive advantage (Isik, Jones, & Sidorova, 2013). Information technology (IT) capabilities refer to the implementation and use of IT resources/assets such as humans, technologies and relationship with other resources to support business processes to gain competitive advantage (Rai, Pavlou, & Du, 2012). For the purpose of this study, BI capabilities are defined as the utilisation and interaction of BI resources with other resources to support business process, hereby referring to a more specific form of IT capabilities in the context of BI systems. BI resources comprise technologies such as data warehouses, dashboards, data mining, visualisation, reporting, software applications and other hardware. Other resources could be both tangible and intangible, including people, governance, culture, products, finances, skills and knowledge. Organisations integrate these resources into business processes to enhance operational performance.

BI capabilities can be categorised into internally-oriented BI and externally-oriented BI (Neirotti & Raguseo, 2017). Internally-oriented BI capabilities focus on internal information processing on a cross-functional area, production and quality control. Enterprise Resource Planning (ERP) solutions is an example of an internally-oriented BI capabilities to process organisational data based on internal operations, thus improve operational efficiency and produce reliable products. Externally-oriented BI capabilities focus on external environment such as customers’ and/or suppliers’ needs that allow organisations to respond to market changes in a timely manner or collaboration between internal organisation with external partners and customers. Supply Chain Management (CRM) and new product development activities are examples of externally-oriented BI capabilities. Internally-oriented BI capabilities focus on increased efficiency, cost reduction and reliability of products, while externally-oriented BI capabilities focus on product differentiation and support market research and CRM processes (Neirotti & Raguseo, 2017).

Information Technology (IT) Governance

The IT governance plays a vital role in the business process. Governance is considered as an organisational’s enabler (van den Broek & van Veenstra, 2018) and it is an integral structure of corporate governance (Alreemy, Chang, Walters, & Wills, 2016). It is the responsibility and practice exercises by the management and board of directors, which comprise of leadership, organisational structures and processes (Altemimi & Zakaria, 2016) with the goal of providing effectiveness and sustainability of IT initiatives (Yudatama, Nazief, & Hidayanto, 2017). The organisation’s strategy and direction are aligned to ensure that objectives are achieved, risks are managed appropriately and IT/BI resources are used responsibly (Madanoglu, Kizildag, & Ozdemir, 2018).

Prior researches have highlighted that IT governance provides the mechanism to allow organisations to manage the internal and external resources effectively to gain optimum performance (Park, Lee, Daniel Lee, & Koo, 2017). It is necessary for organisations to focus on the IT governance which allows a business to align with its strategies, goals and objectives towards the BI development and operations. Several studies revealed that organisations which have the ability to manage IT resources effectively are able to gain superior organisation performance (Park et al., 2017). Xue, Ray, and Gu (2010) found significant relationship between environmental uncertainty and decentralisation of IT infrastructure governance. Gu, Xue, and Ray (2008) analysed the effects of IT governance on the IT investment performance. Pang (2014) found positive impact of IT governance on performance. Alkhaldi & Wraikat (2015) also proved that the IT governance which consists of four key attributes (accountability, transparency, participation and predictability) enhanced performance in public organisations. Alkhaldi et al. (2017) further their research on a study and found that smart enterprise system capabilities and knowledge in organisational capabilities have a positive dynamic influence on IT governance activities.

Park et al. (2017) studied the alignments of internal and external IT governance in order to improve organisational performance. Internal IT governance is categorised into internal hierarchy, internal market and internal network. Sambamurthy and Zmud (1999) suggested three IT governance approaches (centralised, decentralised and federal approaches) based on the internal IT resources. External IT governance emphasises on the inter-organisational relationship, such as certain job functions being outsourced to another organisation. BI resources are often acquired from an outsource service provider but are managed internally by the organisation itself (Park et al., 2017). Under the external market, organisations demand low prices from the outsource service provider (Park et al., 2017). Park et al. (2017) studies showed that alignments between the internal and external IT resources significantly affect organisational performance.

Literature Gaps and Conceptual Framework

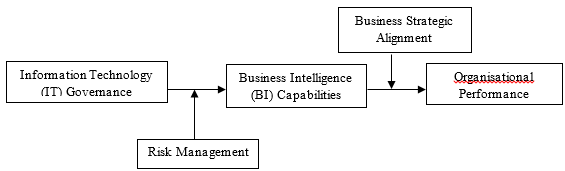

Based on the literature synthesised, there are still gaps in the existing research and empirical evidence on achieving effectiveness with BI capabilities which impact organisational performance (Sangari & Razmi, 2015; Ramakrishnan et al., 2016). Therefore, this paper proposes a conceptual framework which presents an integrated view of the influence of IT governance on BI capabilities, and the impact of such capabilities towards organisational performance. Particularly, this framework incorporates key elements of IT governance, namely top management commitment and sponsorship, end-users participation, change management and dynamic resource management. At the same time, the role of risk management is crucial and it influences the relationship between IT governance and BI capabilities; while business strategy alignment is deemed to influence the relationship between BI capabilities and organisational performance. Figure

Information Technology (IT) Governance and BI Capabilities

IT governance can be implemented using various structures, processes and mechanisms to make decisions for obtaining BI resources (Giovannetti & Marvasi, 2018). IT governance is an integrated set of actions, policies, responsibilities and organisational structures associated with IT to support effective decision makings (Chi, Zhao, George, Li, & Zhai, 2017). A good IT governance involves the managing of BI to produce supreme performance in the organisation, and assists in the decision making and problem- solving processes (Sandfreni & Adikara, 2017). Sirisomboonsuk, Gu, Cao, and Burns (2018) referred IT governance as the process of making decisions about BI investments, who is responsible in making decisions, how decisions are made and how to measure the outcomes.

An integrated business model and BI plans can be developed with specific accountability, responsibility, and priority on the BI initiative. Project managers benchmark the organisational performance and outcomes based on the plans (Sirisomboonsuk et al., 2018). A good implementation of IT governance can improve the accountability, transparency, participation and predictability issues in enhancing performance (Alkhaldi, Hammami, Kasem, Rashed, & Alraja , 2017) alongside with users’ participation in giving feedback in BI policies.

Without a good IT governance, BI capabilities could not be prioritised and channelled to the right users. If the IT governance and risks controls are not appropriately implemented, BI strategies will be greatly affected in meeting the organisation’s mission and goals (Al-Ruithe, Benkhelifa, & Hameed, 2016). Symons, Cecere, Young, and Lambert (2005) pointed out that the BI is expected to deliver value to the business and BI risks are mitigated under the IT governance. The IT governance aligned BI with business goals and objectives to ensure that BI operations are continuously supported (Lee & Widener, 2016). Therefore, this paper assumes that the IT governance has an impact on BI capabilities.

Proposition 1. IT governance has positive influence on BI capabilities.

BI Capabilities and Organisational Performance

The BI capabilities of an organisation have positive impact on the BI’s implementation effectiveness and success. The BI capabilities and BI implementation effectiveness have been examined in the BI maturity model literature (Richards, Yeoh, Chong, & Popovič, 2017). Cosic, Shanks, and Maynard (2012) divided the Business Analytics capabilities into four capability areas in the Business Analytics Capability Maturity Model which are governance, culture, technology and people. Technology capabilities is one of the important components to enable BI. Most enterprises use BI and analytical tools for extracting, transforming and loading data. The BI tools are able to produce accurate and real time information across users which in turn helps an organisation to increase productivity, quality and flexibility, and contributes to the effectiveness of BI implementation (Clark Thomas et al., 2007).

By deploying the right capabilities, BI can forecast the product demand and supply, monitor new products in the market and respond fast to market changes (Işik et al., 2013). The effectiveness of BI depends on the organisation such as increase in profitability, reduced operations costs and enhanced efficiency. Therefore, BI effectiveness is referred as the benefits obtained by organisations and implementations which effectively meet the dynamic changes in market demands through the use of BI (Grublješič & Jaklič, 2015). The success of BI continues to be a strong source of improving business performance (Ransbotham & Kiron, 2017). Organisations are ready to evolve with the times to garner the benefits from BI capabilities. It is also noted that not all organisations are able to deliver business value from the BI implementation due to mismatches between the BI and its goals (Işik et al., 2013; Richards et al., 2017). Therefore, this paper assumes that BI capabilities has an impact on organisational performance.

Proposition 2. BI capabilities has positive influence on organisational performance.

The Moderating Role of Risk Management

Risk management involves evaluating the impacts of business risks and the technical risks associated with BI investments, to mitigate the cost of losses. BI risks should be made aware by top management while risk management should protect BI assets (data, data warehouse, hardware, BI tools or facilities) and BI invention from threats (natural disaster or technical failures) (Sirisomboonsuk et al., 2018). Neural networks and support vector machine techniques are used as a warning monitoring system for finance (Wu, Chen, & Olson, 2014), insurance (Wang & Xu, 2018) or analysing credit card applications (Patil, Nemade, & Soni, 2018).

Implementing BI user policies within an organisations is an important step in managing BI risks (Demek, Raschke, Janvrin, & Dilla, 2018). Policies may include specific guidelines, specifying whether employees can or cannot access the BI data. IT governance and risk management provide an effective collaboration to safeguard BI assets, disaster recovery and data integrity/confidentiality within an organisation. Most BI tools (artificial neural networks models, data mining and optimisation techniques) have been used for enhancing risk management (Wu et al., 2014). Otim, Dow, Grover, and Wong (2012) studied the evaluation of business value and the risks of IT investment on organisational performance. Correctly managing IT governance with risk management will improve BI effectiveness (Ghirana & Bresfelean, 2012). Therefore, this paper assumes that risk management influences the relationship between IT governance and BI capabilities.

Proposition 3. Risk management moderates the relationship between IT governance and BI capabilities.

The Moderating Role of Business Strategy Alignment

The success of BI implementation depends on the alignment between a BI and its organisation’s goals and objectives. Chan and Reich (2007) showed that business performance improves when IT and business strategies are aligned in an organisation. Many research studies show that BI capabilities enhanced organisational performance (Elbashir, Collier, & Davern, 2008; Lee & Widener, 2016; Peters, Wieder, Sutton, & Wakefield, 2016). The support from top management and BI knowledge (Lee & Widener, 2016), together with BI culture, motivate low level or operational managers to use the BI (Elbashir et al., 2008). Strategy alignment occurs when BI is aligned with the business goals. Business strategies, management and business processes should be consistent. IT strategies are used to support the BI initiatives. IT infrastructure and IT organisation are used to enhance the management and business processes. Business strategies are the responsibility of the leaders to help synchronise BI capabilities with the goals and objectives (Akter, Wamba, Gunasekaran, Dubey, & Childe, 2016) which impact organisational performance.

The ability of an organisation to use BI to enhance performance is determined by the ability of an organisation to make alignment and government of BI initiative, and the business design must have the flexibility to fully leverage the BI initiative. In the context of business strategic perspective, business strategies and IT strategies should respond to environmental drivers (for example, demographic changes and competitor moves). Bhattacharjya & Chang (2010) studies found that enhancing the interaction between IT and business helps to generate values from IT practices. BI dashboards and analytic tools can be employed and balanced scorecards provide top management with the overall view on organisational strategy, and its metrics will assist in the process of improving business performance (González-Rodríguez, Jiménez-Caballero, Martín-Samper, Köseoglu, & Okumus, 2018). Therefore, this paper assumes that business strategy alignment influences the relationship between BI capabilities and organisational performance.

Proposition 4. Business strategy alignment moderates the relationship between BI capabilities and organisational performance.

Conclusion

Addressing the gaps in current literature as synthesised, this paper presents a conceptual framework which presents an integrated view of the influence of IT governance on BI capabilities, and the impact of such capabilities towards organisational performance. Furthermore, the role of risk management is crucial and it influences the relationship between IT governance and BI capabilities; while business strategy alignment is deemed to affect the relationship between BI capabilities and organisational performance. A set of propositions was formulated based on the conceptual framework as well as existing literature to establish the relationships among the variables. These propositions provide a theoretical basis for subsequent empirical study.

This paper contributes to the field of organisational performance particularly in the context of BI capabilities, while examining the interplay of IT governance, risk management as well as business strategy alignment in this context. Practically, this paper suggests the importance of IT governance as well as risk management on BI capabilities. In addition, this paper justifies the crucial role of BI capabilities and business strategy alignment which impact the performance of business organisations in emerging economies.

References

- Akter, S., Wamba, S. F., Gunasekaran, A., Dubey, R., & Childe, S. J. (2016). How to improve firm performance using big data analytics capability and business strategy alignment? International Journal of Production Economics, 182, 113–131.

- Al-Ruithe, M., Benkhelifa, E., & Hameed, K. (2016). A Conceptual Framework for Designing Data Governance for Cloud Computing. Procedia Computer Science, 94(MobiSPC), 160–167.

- Alkhaldi, F. M., & Wraikat, M. M. (2015). IT Governance and Organisationl Performance. International Journal in Social Sciences, 5(4).

- Alkhaldi, F. M., Hammami, S. M., Kasem, S., Rashed, A., & Alraja, M. N. (2017). Enterprise System as Business Intelligence and Knowledge Capabilities for Enhancing Applications and Practices of IT Governance. International Journal of Organizational and Collective Intelligence, 7(2), 63–77.

- Alreemy, Z., Chang, V., Walters, R., & Wills, G. (2016). Critical success factors (CSFs) for information technology governance (ITG). International Journal of Information Management, 36(6), 907–916.

- Altemimi, M. A. H., & Zakaria, M. S. (2016). Developing factors for effective IT governance mechanism. 2015 9th Malaysian Software Engineering Conference, MySEC 2015, 245–251.

- Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations. Decision Support Systems, 97, 58–68.

- Bhattacharjya, J., & Chang, V. (2010). Adoption and Implementation of IT Governance: Cases from Australian Higher Education. Strategic Information Systems: Concepts, Methodologies, Tools, and Applications.

- Chan, Y. E., & Reich, B. H. (2007). IT alignment: What have we learned? Journal of Information Technology, 22(4), 297–315.

- Chi, M., Zhao, J., George, J. F., Li, Y., & Zhai, S. (2017). The influence of inter-firm IT governance strategies on relational performance: The moderation effect of information technology ambidexterity. International Journal of Information Management, 37(2), 43–53.

- Clark Thomas D. J., Jones, M. C., & Armstrong, C. P. (2007). The Dynamic Structure Of Management Support Systems: Theory Development, Research Focus, And Direction. MIS Quarterly, 31(3), 579–615.

- Columbus, L. (2018). The State of Business Intelligence, 2018. Retrieved August 10, 2018, from https://www.forbes.com/sites/louiscolumbus/2018/06/08/the-state-of-business-intelligence-2018/

- Cosic, R., Shanks, G., & Maynard, S. (2012). Towards a business analytics capability maturity model. ACIS 2012: Location, Location, Location: Proceedings of the 23rd Australasian Conference on Information Systems 2012, 1–11.

- Demek, K. C., Raschke, R. L., Janvrin, D. J., & Dilla, W. N. (2018). Do organizations use a formalized risk management process to address social media risk? International Journal of Accounting Information Systems, 28(December 2017), 31–44.

- Eiskop, T., Snatkin, A., Kõrgesaar, K., & Søren, J. (2014). Development and application of a holistic production monitoring system. 9th International DAAAM Baltic Conference "INDUSTRIAL ENGINEERING”, (April), 85–91. Retrieved from http://innomet.ttu.ee/daaam14/proceedings/Production Engineering and Management/Eiskop.pdf

- Elbashir, M. Z., Collier, P. A., & Davern, M. J. (2008). Measuring the effects of business intelligence systems: The relationship between business process and organizational performance. International Journal of Accounting Information Systems, 9(3), 135–153.

- Fink, L., Yogev, N., & Even, A. (2017). Business intelligence and organizational learning: An empirical investigation of value creation processes. Information and Management, 54(1), 38–56.

- Gartner. (2017). Gartner Says Worldwide Business Intelligence and Analytics Market to Reach $18.3 Billion in 2017. Retrieved April 13, 2018, from https://www.gartner.com/newsroom/id/3845563

- Ghirana, A. M., & Bresfelean, V. P. (2012). Compliance Requirements for Dealing with Risks and Governance. Procedia Economics and Finance, 3(12), 752–756.

- Giovannetti, G., & Marvasi, E. (2018). Governance, value chain positioning and firms’ heterogeneous performance: The case of Tuscany. International Economics, 154(October 2017), 86–107.

- González-Rodríguez, M. R., Jiménez-Caballero, J. L., Martín-Samper, R. C., Köseoglu, M. A., & Okumus, F. (2018). Revisiting the link between business strategy and performance: Evidence from hotels. International Journal of Hospitality Management, 72(November 2017), 21–31.

- Gröger, C., Kassner, L., Hoos, E., Königsberger, J., Kiefer, C., Silcher, S., & Mitschang, B. (2016). The data-driven factory leveraging big industrial data for agile, learning and human-centric manufacturing. In 18th International Conference on Enterprise Infiormation Systems (pp. 40–52). SCITEPRESS - Science and Technology Publications,Lda.

- Grublješič, T., & Jaklič, J. (2015). Business Intelligence Acceptance: The Prominence of Organizational Factors. Information Systems Management.

- Gu, B., Xue, L., & Ray, G. (2008). IT Governance and IT Investment Performance: An Empirical Analysis. Ssrn, (July).

- Işik, Ö., Jones, M. C., & Sidorova, A. (2013). Business intelligence success: The roles of BI capabilities and decision environments. Information and Management, 50(1), 13–23.

- Lee, J., Kao, H. A., & Yang, S. (2014). Service innovation and smart analytics for Industry 4.0 and big data environment. Procedia CIRP, 16, 3–8.

- Lee, M. T., & Widener, S. K. (2016). The Performance Effects of Using Business Intelligence Systems for Exploitation and Exploration Learning. Journal of Information Systems, 30(3), 1–31.

- Madanoglu, M., Kizildag, M., & Ozdemir, O. (2018). Which bundles of corporate governance provisions lead to high firm performance among restaurant firms? International Journal of Hospitality Management, 72(January), 98–108.

- Neirotti, P., & Raguseo, E. (2017). On the contingent value of IT-based capabilities for the competitive advantage of SMEs: Mechanisms and empirical evidence. Information and Management, 54(2), 139–153.

- Neuböck, T., & Schrefl, M. (2015). Modelling knowledge about data analysis processes in manufacturing. IFAC-PapersOnLine, 28(3), 277–282.

- Otim, S., Dow, K. E., Grover, V., & Wong, J. A. (2012). The Impact of Information Technology Investments on Downside Risk of the Firm: Alternative Measurement of the Business Value of IT. Journal of Management Information Systems, 29(1), 159–194.

- Pang, M. S. (2014). IT governance and business value in the public sector organizations - The role of elected representatives in IT governance and its impact on IT value in U.S. state governments. Decision Support Systems, 59(1), 274–285.

- Park, J., Lee, J. N., Daniel Lee, O. K., & Koo, Y. (2017). Alignment between Internal and External IT Governance and Its Effects on Distinctive Firm Performance: An Extended Resource-Based View. IEEE Transactions on Engineering Management, 64(3), 351–364.

- Patil, S., Nemade, V., & Soni, P. K. (2018). Predictive Modelling for Credit Card Fraud Detection Using Data Analytics. Procedia Computer Science, 132, 385–395.

- Peters, M. D., Wieder, B., Sutton, S. G., & Wakefield, J. (2016). Business intelligence systems use in performance measurement capabilities: Implications for enhanced competitive advantage. International Journal of Accounting Information Systems, 21, 1–17.

- Rai, A., Pavlou, P. A., & Du, S. (2012). Interfirm It Capability P Rofiles and Communications for Cocreating R Elational Value : Evidence. MIS Quartely, 36(1), 233–262.

- Ramakrishnan, T., Khuntia, J., Kathuria, A., & Saldanha, T. (2016). Business intelligence capabilities and effectiveness: An integrative model. Proceedings of the Annual Hawaii International Conference on System Sciences, 2016–March, 5022–5031.

- Ransbotham, S., & Kiron, D. (2017). Analytics as a Source of Business Innovation. MIT Sloan Management Review, (58380), 1–21. Retrieved from http://sloanreview.mit.edu/projects/analytics-as-a-source-of-business-innovation/

- Richards, G., Yeoh, W., Chong, A. Y. L., & Popovič, A. (2017). Business Intelligence Effectiveness and Corporate Performance Management: An Empirical Analysis. Journal of Computer Information Systems.

- Sambamurthy, V., & Zmud, R. W. (1999). Arrangements for Information Technology Governance: A Theory of Multiple Contingencies. MIS Quarterly, 23(2), 261–290. Retrieved from https://www.jstor.org/stable/249754

- Sandfreni, & Adikara, F. (2017). Capability level assessment of IT governance in PTP Mitra Ogan: COBIT 5 framework for BAI 04 process. 2017 4th International Conference on Computer Applications and Information Processing Technology (CAIPT), 1–5.

- Sangari, M. S., & Razmi, J. (2015). Business intelligence competence, agile capabilities, and agile performance in supply chain An empirical study. International Journal of Logistics Management, 26(2), 356–380.

- Sharda, R., Delon, D., & Turban, E. (2014). Business Intelligence: A Managerial Perspective on Analytics. Essex, England: Pearson.

- Sirisomboonsuk, P., Gu, V. C., Cao, R. Q., & Burns, J. R. (2018). Relationships between project governance and information technology governance and their impact on project performance. International Journal of Project Management, 36(2), 287–300.

- Symons, C., Cecere, M., Young, G. O., & Lambert, N. (2005). IT Governance Framework - Best Practices. Forrester, 1–17.

- van den Broek, T., & van Veenstra, A. F. (2018). Governance of big data collaborations: How to balance regulatory compliance and disruptive innovation. Technological Forecasting and Social Change, 129(September 2017), 330–338.

- Wang, Y., & Xu, W. (2018). Leveraging deep learning with LDA-based text analytics to detect automobile insurance fraud. Decision Support Systems, 105, 87–95.

- Wixom, B., Ariyachandra, T., Goul, M., Gray, P., Kulkarni, U., & Phillips-Wren, G. (2011). The current state of Business Intelligence in academia. Communications of the Association for Information Systems, 29(1), 299–312.

- Wu, D. D., Chen, S. H., & Olson, D. L. (2014). Business intelligence in risk management: Some recent progresses. Information Sciences, 256.

- Xue, L., Ray, G., & Gu, B. (2010). Environmental Uncertainty and IT Infrastructure Governance: A Curvilinear Relationship. Information Systems Research, 22(2).

- Yudatama, U., Nazief, B. A. A., & Hidayanto, A. N. (2017). Benefits and Barriers as a Critical Success Factor in the Implementation of IT Governance: Literature Review. The International Conference on ICT for Smart Society (ICISS), 1–6.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

02 August 2019

Article Doi

eBook ISBN

978-1-80296-064-8

Publisher

Future Academy

Volume

65

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-749

Subjects

Business, innovation, sustainability, environment, green business, environmental issues

Cite this article as:

Yuen, P. K., & Ping, T. A. (2019). The Impact of Business Intelligence Capabilities on Organisational Performance in Malaysia. In C. Tze Haw, C. Richardson, & F. Johara (Eds.), Business Sustainability and Innovation, vol 65. European Proceedings of Social and Behavioural Sciences (pp. 381-390). Future Academy. https://doi.org/10.15405/epsbs.2019.08.38