Company Environmental Reporting: Experience And Prospects Of Practice In The Russian Federation

Abstract

The study was conducted in the form of international and Russian practice critical analysis in order to identify systemic problems of environmental reporting and factors that can contribute to its dissemination in the Russian Federation, as well as to improve the quality characteristics for greater awareness of stakeholders. On the basis of the various approaches to the environmental reports formation review, including the situation in developing countries, possible measures to promote this type of non-financial reports in Russia, in particular, on the basis of state participation, the "green" financing mechanisms introduction, corporate governance improvement are identified. The analysis of the environmental reporting process allowed establishing not only the General backlog of Russian practice from the world, but also problems with low transparency and verifiability of reports. Based on the review of Russian corporations’ non-financial statements, the low level of specific environmental indicators availability in most companies is also revealed. To solve these problems, measures are proposed to standardize the content of environmental reports in Russian economic entities and the public authorities motivating effects in the form of enterprises environmental protection projects co-financing, the introduction of tax relief. At the same time, taking into account the world experience, before the allocation of these preferences, a preliminary comprehensive assessment of companies environmental reporting quality and the establishment of the environmental reports mandatory certification requirement is recommended.

Keywords: Environmental reportingintegrated reportingnon-financial reportingstakeholderstransparencyquality of reporting

Introduction

The generally recognized information on financial and non-financial characteristics of the organization disclosure method is the companies public reporting. The quality of such reporting and its transparency determine the society, the state and investors awareness about the impact of the business entity not only on the economic, but also on the social and environmental environment.

Global trends in environmental reporting

Strengthening of anthropogenic impact, unsolved and accumulation of environmental problems on a global scale actualize the environmental management problems, which can be solved only with the all societies members participation, including business entities. The scale of environmental problems is steadily increasing and today the solution of individual aspects of environmental detail is not enough. So, the biodiversity conservation strategy of the European Union for the period up to 2020 calls its members to assess the state of ecosystems in its national territory, involving in this process public sector organizations, corporations and citizens (Maes et al., 2018; Bateman, 2013; Masko, 2014; Theobald, 2013).

Today, environmental impact assessment is a key tool for sustainable development in more than 200 countries (Drayson, Wood, & Thompson, 2015). In connection with these companies for environmental responsible management implemention, special attention should be paid to the environmental protection measures implementation and environmental reports for stakeholders preparation.

Russian environmental reporting genesis

The Russian scientific and technological development strategy (decree of the President of the Russian Federation from 01.12.2016) as a big challenge for society and the state called the increasing pressure of anthropogenic factors on the environment and the problem of natural resources shortage. At the same time, the environmental reporting formation in Russia began later than in the world practice, only at the beginning of the XXI century. Mandatory reporting on environmental impacts is provided by companies in the form of environmental reporting statistical forms that are not public accessible. Nowadays steps for increasing environmental information public disclosure are being taken. In 2012, the guidelines for the environmental policy of the Russian Federation at the period up to 2030 were approved, the document provides the development of voluntary non-financial reporting on sustainable development, the transition to mandatory publication by state corporations and companies with state participation, reports about sustainable development in accordance with international standards, assure the independent third party. Despite the expressed intention to improve environmental reporting, changes in this area were slow. According to H. Drager (Golovachev, 2013), Russia lags in the practice of reporting on sustainable development, part of which are environmental reports, for 10-20 years from Europe and 10-15 years from the United States. In order to reduce this gap, active measures are needed to increase the potential of environmental reporting in Russia and to develop its methodology.

Problem Statement

Interpretation of environmental reporting in Russian and world practice

Currently, as noted by H. Drager (Golovachev, 2013), there are more than 60 standards for the preparation of non-financial reporting in the world, which indicates serious problems of information presentation conceptual choice faced by the environmental reporting compilers.

Most companies that publicly disclose their non-financial results prepare reports using the approaches and principles of the three most popular standards sets:

Sustainable development reporting standards of the Global reporting initiative (GRI);

Standarts АА1000;

Standards for economic sectors developed by the sustainable development reporting standards board (SASB).

The updated version of the G4 management issued by GRI, an independent non-governmental organization, provides that the sustainable development report of the company should characterize its positive or negative impact on the environment. That is, at present, the development of environmental reporting in the world is interpreted within the framework of the sustainable development concept.

The methodology for assessing the corporate reporting quality developed within the framework of the UN Conference on trade and development (UNCTAD) by the Intergovernmental working group of the United Nations accounting and reporting standards experts, environmental reporting is treated as a structural element of corporate reporting.

Today in Russia, researchers have not formed a unified approach to the environmental reporting concept. Some scientists (Ilyicheva, 2009) interpret environmental reporting as part of the environmental accounting system, other researchers (Sapozhnikova & Khudhur, 2014) characterize environmental reporting as a special type of statistical reporting and financial reporting separate elements. Some of the presented interpretations are controversial, since statistical reporting in Russia is available to users only after the aggregation carried out by special organizations, that is, stakeholders do not have the opportunity to directly familiarize themselves with it in its original form. The authors share the vision of environmental reporting as a special part of corporate reporting.

Environmental reporting development global experience

For reporting, it is important to be realistic about what factors affect the environmental reports quality. A number of scientists pay attention to the analysis of the state influence on the environmental reporting development. So, Hui, Carol, & Pi-Shen (2018) in the study on the example of the Chineese national republic established direct influence of the Government to the development of environmental reporting by Chinese companies. In connection with the aggravation of environmental problems against the extremely rapid economic development background, the Chinese Government adopted a policy of encouraging businesses that provide environmental information. In particular, such a company is given priority in obtaining funds allocated by the state for the implementation of environmental protection programs. As a result of these policy since 2008, the number of environmental reports disclosed by Chinese companies has increased significantly. At the same time, it should be taken into account that in the country under consideration the mechanism of state power differs significantly from traditional European countries, China's economy can be characterized as transitional and identified as authoritarian capitalism. In addition, the regulatory influence of the Chinese government does not have a strong impact on the quality of environmental reporting information, since the types of information included and the level of detail are not standardized.

A serious factor that can influence the environmental reportings development is the emergence of possible advantage in obtaining funding. The results of the "green" banking programs in developing countries have been studied by Hossain, Bir, Tarique, & Momen (2016). Such programs involve promoting environmental business by providing loans at lower interest rates, investing in resource-saving equipment and transport, and other energy-efficient facilities. Banks in order to check the validity of the application by companies specified preferences to implement certain environmental standards for lending and evaluate environmental reporting.

Lu, Abeysekera, & Cortese (2015) based on the results of the study using regression analysis methods, concluded that the environmental reporting quality is directly determined by the specifics of corporate governance.

No less important for the environmental reporting practice are the research results by Hoque, Clarke, & Huang (2016), in which all stakeholders in the prevention of the Chittagong city environmental pollution (Bangladesh) were divided into 11 groups. With the general awareness of all the selected groups, only one of them, represented by environmental public organizations, was ready to take an active part in the protection of the environment and to involve participants of other groups in this process. These findings in the context of developing countries raise concerns about the capacity of civil society to prevent pollution in general and the the environmental reporting institute development in particular. This fact also points the different interest and activity of stakeholders, which should be taken into account by the drafters of environmental reports. Understanding these processes will allow the government and business to take into account the world experience in the transformation of approaches to environmental reporting in Russia.

Research Questions

In accordance with the identified environmental reporting problems in the framework of this study, the following questions were formulated:

What does the experience of Russian companies in the environmental statements preparation demonstrate?

What factors will contribute to the development of the methodology for the preparation of environmental statements?

Purpose of the Study

The objectives of this study are:

To analyze the Russian environmental reporting practice.

To develop proposals that contributes to the environmental reporting methodology development and increases its transparency.

Research Methods

Research hypothesis formation

Environmental reporting has been formed by Russian companies since the 2000s. During this time, a number of stable trends and systemic problems have been set, the identification of which is extremely important for the environmental reporting approaches for transformation in the Russian Federation conditions.

Russian business environmental responsibility

According to the definition given by the European Commission, environmental responsibility is the free decision of an enterprise to participate in improving the living conditions and protecting the environment. This understanding is enshrined in international documents (UN Global compact, ISO 26000 Standard) and is shared by Russian business (social Charter of Russian business). The definition of environmental responsibility leads to the conclusion that environmental programmes and activities undertaken by companies are voluntary. Currently, this responsibility and the burden of its financial support falls primarily on business entities as active participants in economic relations. Environmental responsibility and its financial implications will increase every year, and it is differentiated by the companies’ economic activities types.

Н1 In Russia, the environmental responsibility of business is increasing every year and this trend is manifested mainly in the sectors engaged in active nature resources use.

Environmental capital as part of financial reporting

Environmental resources for companies, as a source of economic benefits, play an important role in the production and maintenance of sustainable development. Such resources are primarily non-renewable. In this regard, environmental protection measures and investments of companies in resource-saving technologies become a special object of accounting. In modern practice of integrated reporting, environmental capital is considered as a structural element that systematically characterizes the company's participation in programs and activities for environmental protection, resource conservation, carefully evaluated by stakeholders.

Н2 A new object of accounting and an element of non – financial reporting-environmental capital-has been formed for the Russian practice.

Russian companies environmental reporting quality

To ensure sustainable development and increase their investment attractiveness, companies need to pay much more attention to environmental reporting. Investors point to the long-term benefits of investing in companies that pay close attention to these issues, and to the lower level of risk in such investments. Despite the current environmental reporting practice, some Russian corporation's environmental reporting is not always useful for users and transparent. One of their main drawbacks is information overload.

Н3 Environmental reporting by Russian companies is not systematic and therefore not always transparent and useful.

Environmental reporting standardization

In Russia, there are no standards for public reporting that would oblige economic entities to disclose environmental information, which is a serious obstacle to the environmental reporting methodology development. World experience shows a positive impact on the formation of environmental reporting regulation by public authorities through this kind of information disclosure standards establishment. So, in 2010 in the US, the concept of large greenhouse gas issuers is regulated, which are required to form a special report in the context of this negative impact on the environment. In France, the obligation to disclose environmental information, which is also subject to mandatory audit, has been introduced for listed companies since 2010. In 2013, England established the public sector organizations obligation to assess the environmental impact of procurement.

Н4 It is necessary to form and implement environmental reporting standards, as well as to develop a system of measures for the application of these standards by business entities.

Research methodology

In the research process the methods of chronological analysis, synthesis, modeling and abstraction were used. The composition, structure and Russian business entities non-financial reporting content analysis to form an informed opinion on the current environmental reporting practice and its transparency was carried out.

Data collection procedure for the study

Analysis of the composition, current costs and investments in environmental protection structure was made on the state statistics basis. The number of environmental reports and companies-compilers industry affiliation was analyzed according to the National register and the corporate non-financial reports Library, The Russian Union of Industrialists and entrepreneurs.

Findings

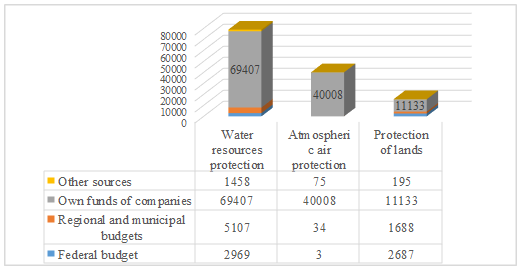

Due to the environmental problems aggravation in Russia, various statistical, economic and environmental agencies publish information on the sources of enterprise's activities financing in the field of environmental responsibility and their investment directions on a regular basis. In the table

It is of the interest to assess the current Russian investment in environmental projects structure (Fig. 1), which clearly demonstrates the dominant role of business entities in the environmental-saving measures implementation.

Source: compiled by the authors on the basis of the statistical collection "environmental Protection in Russia (2016)"

It is important to understand which companies are responsible for environmental reporting. Figure

Source: compiled by the authors on the basis of the National Register and The library of corporate non-financial reports (2018).

Enterprises within the framework of their activities will also incur current costs due to environmental responsibility. The current costs include the costs of fixed assets maintenance for environmental purposes (including maintenance personnel labor costs, maintenance and overhaul, depreciation, energy costs, etc.), as well as the costs of third-party services related to environmental protection.

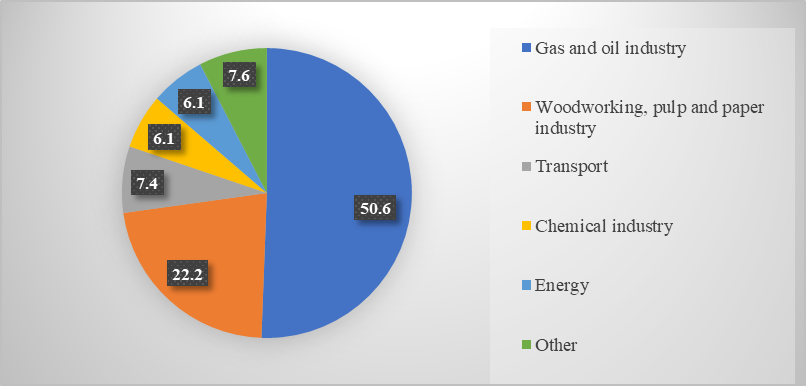

To identify industries that make significant investments in environmental protection measures, we will analyze the current Russian companies’ costs in 2015 (Table

In some Russian corporations reporting not only the characteristics of the environmental management system is given, but also the environmental capital value, environmental efficiency indicators disclosure, within the characteristics of which can be represented by the following indicators:

the company costs to ensure environmental safety (personnel training, utilization or disposal of production waste, waste removal to specialized landfills, making legally established charges for environmental pollution);

natural resources consumption;

the emissions into the atmosphere volume;

information about waste amount and their disposal with the hazard class division.

Thus, the environmental reporting provides diverse information, which indicates the need for an independent external public non-financial reporting evaluation on the initiative of its issuing organizations, which can be carried out in the public confirmation form, and in the professional assurance form. The independent confirmation of non-financial reporting practice has not yet received proper distribution in Russia. Only 16% of Russian companies independently verify their non-financial reports (EY (Ernst & Young), 2017), while in the world 82% of all reports prepared according to the most popular reporting standard – GRI, are audited by a third party.

At the same time, the most common in the world practice tools of independent external evaluation in the sustainable development field, corporate responsibility and public non-financial reporting, carried out on the third party initiative, include indices, ratings, rankings, as well as competitions, awards. In Russia, the most widespread were: Ratings of fundamental (environmental-energy) efficiency Interfax-ERA, Rating of environmental responsibility in oil and gas companies, Rating of environmental responsibility in mining companies in Russia, Rating of forest management, Rating of sustainable development in cities, Environmental rating in regions and cities of Russia. At the same time, the information of these ratings is scattered, which makes it difficult for stakeholders to find it.

At the same time, to verify the environmental reporting reliability in Russia, the environmental audit practice has become widespread, within the framework of which the organization environmental policy validity is checked for compliance by the methods used with the legislation, the environmental protection audit costs in terms of their reliability taking into account the anthropogenic impact significance, the assessment of the production and consumption waste value, the environmental reporting audit in General, which allows to express reasonable confidence in the reliability of such a non-financial report.

Environmental information disclosure analysis clearly demonstrates availability of specific environmental indicators even in the reports of market leaders, despite the fact that these information can help to characterize the stakeholders of result achievement in environmental policy. The highest disclosed performance indicators level observed in terms of air pollutant gross emission, water withdrawal and waste disposal, with reports of some corporations are published not only information about the results over the years, but also plans for the future, but rarely recognized target quantitative indicators. At the same time, data on greenhouse gas emissions reveal just over half of the companies for different reporting periods.

Thus, the established problems in the environmental reporting practice in Russia lead to the conclusion that for the transparent environmental reports dissemination as a form of non-financial information qualitative presentation, the state participation is necessary. At the same time, state influence, according to the authors, can be implemented in the following areas.

1. Environmental reporting standard development and adoption. Such standards must include requirements for the environmental policy characteristics, responsibilities for nature use indicators disclosure – gross and specific (for example, the intensity of resource consumption, rate of emissions and waste), as well as indicators to measure the investments and costs performance for the protection of the environment.

2. Motivating companies that provide transparent environmental reporting on a regular basis, such as co-financing of environmental protection costs (possibly under public and private partnerships), tax or other preferences. At the same time, it is necessary to develop a methodology for integrated assessment of the companies’ environmental reporting quality and to provide a criterion mandatory reports certification.

Conclusion

The study found that in the context of business increasing environmental responsibility, the involvement of Russian companies in the environmental reports submission is slow and unbalanced in various sectors of the economy.

The global environmental problems aggravation has led to the environment capital emergence as a new accounting object and an element of non-financial reporting for the Russian practice. This requires the scientific personnel accounting and analytical support in this area development.

It is established that the non-financial statements independent confirmation practice due to the distribution in Russia has not yet received, which affects the environmental reporting quality, not in all material aspects characterizing the organization for environmental protection activities. This circumstance requires increased attention from stakeholders and the professional community, the adoption of constructive measures in the environmental audit practice dissemination form, environmental ratings in Russia systematization and promotion.

The environmental reporting standards introduction at the legislative level, even in the recommended format and motivating measures on the part of public authorities, will contribute to enhancing the dialogue between Russian companies and investors, increase the company’s investment attractiveness and opportunities for sustainable growth.

References

- Bateman, I.J. (2013). Bringing Ecosystem Services into Economic Decision-Making: Land Use in the United Kingdom. Science, 341(6141), 45-50.

- Drayson, K., Wood, G., & Thompson, S. (2015). Assessing the quality of the ecological component of English Environmental Statements. Journal of Environmental Management, 160, 241-253.

- Environmental protection in Russia (2016) [Online]. Available: http://www.gks.ru/wps/wcm/connect/rosstat_main/rosstat/ru/statistics/publications/catalog/doc_1139919459344 [Accessed 15 October 2018

- EY (Ernst &Young) (2017). Clean technologies and sustainable development. Issue 2. Non-financial reporting of companies: in pursuit of success [Online]. Available: https://www.ey.com/Publication/vwLUAssets/EY-ccass-newsletter-may-2017/%24File/EY-ccass-newsletter-may-2017.pdf [Accessed 15 October 2018]

- Golovachev, S. (2013). Integrated reporting-an opportunity for Russian companies to catch up in the field of corporate reporting: interview with H. Drager [Online]. Available: http://ir.org.ru/mass-media/intervyu/45 [Accessed 15 October 2018

- Hoque, A., Clarke, A., & Huang, L. (2016). Lack of stakeholder influence on pollution prevention: A developing country perspective. Organization and Environment, 29(3), 367-385.

- Hossain, D.M., Bir, A.T., Tarique, K.M., & Momen, A. (2016). Disclosure of Green Banking Issues in the Annual Reports: A Study on Bangladeshi Banks. Middle East Journal of Business , 11(1), 19-30.

- Hui, S., Carol, A.T., & Pi-Shen, S. (2018). The Influence of the Government on Corporate Environmental Reporting in China: An Authoritarian Capitalism Perspective. Business & Society, 1, 1-41.

- Ilyicheva, E. (2009). Comparative characteristics of financial, tax, management and environmental accounting. Fundamental Research, 1, 66-67

- Lu, Y., Abeysekera, I., & Cortese, C. (2015). Corporate social responsibility reporting quality, board characteristics and corporate social reputation: Evidence from China. Pacific Accounting Review, 27(1), 95-118.

- Maes, J., Teller, A., Erhard, M., Grizzetti, B., Barredo, J.I., Paracchini, M.L., … & Werner, B. (2018). Mapping and Assessment of Ecosystems and their Services: An analytical framework for mapping and assessment of ecosystem condition in EU. Luxembourg, Luxembourg: Publications Office of the European Union

- Masko, L. (2014). Operations with environmental assets and liabilities audit methods. Audit Statements, 4, 63-75

- National Register and the Library of corporate non-financial reports. (2018) [Online]. Available: http://xn--o1aabe.xn--p1ai/simplepage/157 [Accessed 15 October 2018]

- Sapozhnikova, N., & Khudhur, M.A. (2014). Information on environmental activities in corporate accounting and reporting. International Accounting, 15, 22-29

- Theobald, D. (2013). A general model to quantify ecological integrity for landscape assessments and US application. Landscape Ecology, 28 (7), 1859-1874.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

20 March 2019

Article Doi

eBook ISBN

978-1-80296-056-3

Publisher

Future Academy

Volume

57

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1887

Subjects

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Potasheva, O., Arkhipova, N., & Shatunova, G. (2019). Company Environmental Reporting: Experience And Prospects Of Practice In The Russian Federation. In V. Mantulenko (Ed.), Global Challenges and Prospects of the Modern Economic Development, vol 57. European Proceedings of Social and Behavioural Sciences (pp. 790-800). Future Academy. https://doi.org/10.15405/epsbs.2019.03.78