Innovative Approach To Accounting Information Support Of The Management Of The Organization

Abstract

The article is dedicated to the issues of improving the systems of accounting and information support for the management of commercial organizations. The study of the used conceptual apparatus, content and organization of the information support of the organization’s management has led to the conclusion about the unresolved issues in the field of accounting theory and practice, its role, place and mechanism of formation of the informational flow. The necessity of the study is due to the lack of methodological developments, insufficient scientific and practical development of issues of adaptation of modern accounting systems to the requirements of improving the efficiency of management of the organization. Nowadays, many issues of accounting and information support remain unresolved or debatable. First of all, they include: insufficient adaptability of information needs to rapidly changing internal circumstances and the external environment; fragmentation, and sometimes, contradictory information received in the context of user groups; preferential focus on obtaining synthesis information when using unjustified conventions in the calculations; insufficient attention in the justification of the composition of expenses and methods of their accounting to the technical and organizational features of the organization. In accordance with this, the article proposed the author's vision of the concepts “information”, “accounting”, an approach to determining the structure and content of the accounting system, substantiating the possibility and expediency of harmonizing accounting subsystems and integrated processing of economic information.

Keywords: Informationaccountingaccounting systemaccounting and information supportinformation systems

Introduction

The development of society causes the need to improve the information management system of the organization. The problem of modern information support of management is due to the "information explosion" - an increase in the rate of appearance and amount of information. If in 2007 the amount of information in the world was 300 exabytes, in 2013 - 1200 exabytes, in 2017 - 16000 exabytes, in 2025 the planned amount of information will reach 163,000 exabytes. Researchers believe that by 2025, 60% of this information will be generated by companies using highly intelligent control systems.

In a digital economy and an actively developing information society, information becomes one of the most important assets of an organization. In this regard, there are questions about the content of the concept of “information”, the role and place of accounting in the system of formation of information flows of the organization. Accounting in the digital economy should cease to perform the functions of observing and recording the facts of economic life. The solution of these tasks is assigned to modern technical means of recording and transmitting information. Under these conditions, accounting and control tasks are assigned to the accounting, i.e. he himself becomes a consumer of information, and the transmission of information of a qualitatively different content in accordance with the requests of internal and external users. Transformation of the role and place of accounting in the management system implies the need to change the organization and content of accountants' workstations. The study showed that the workplace of an accountant is currently represented in the form of an automated workplace (AWP), which is an integral part of an automated control system (ACS). In the conditions of the automated workplace is the formation of a data system. Data systems have significantly simplified the transformation of information in accordance with incoming management requests by: centralizing current information, simplifying access to this information and the ability to present analytical and reporting information.

However, due to the increase in the array of information flows, the increased requirements for the speed of the decisions taken by the automated workplace as a subsystem of the ACS are not able to fully meet the requirements for information support of the organization’s management. In this regard, there is a need to solve the scientific and practical problems of changing perceptions about the content of the function of accounting in the management system and developing practical recommendations for its implementation in the practice of the organization.

Problem Statement

The development of a system of accounting and information support for the management of an organization occurs under conditions of increasing competition and the formation of a digital economy. Under these conditions, there is a need to solve a number of scientific and practical problems.

In the conditions of a sharp increase in the array of management information support and growth in the requirements for it, the problems of duplication of information flows, the formation of data systems, the exclusion of redundant data in them that were not demanded later by the management of the organization, are exacerbated. Until now, in the economic literature there is no clear definition of the interrelated concepts of “information”, “information” and “data”.

The study of information issues, its role in society, as well as issues of advanced information management systems were engaged in such scientists as Asatiani & Penttinen (2015), Strouhal, Horák, & Bokšová (2017) and a number of other scientists.

One of the main sources of information flow in the organization is accounting. The introduction of modern automation tools for collecting and processing information has significantly changed the role and place of accounting in the information management system. Accounting in modern conditions is not only an information provider, but also its user, since performs the function of solving analytical tasks. It is important to note that accounting is only part of the accounting system and is not able to solve the whole complex of tasks facing it.

Accounting and accounting systems have been the subject of research by a number of leading scientists, such as: Pyatov (2018), Ragulina, Suglobov, & Melnik (2018), Kostyukova, Vakhrushina, Shirobokov, Feskova, & Neshchadimova (2018), Ali, Omar, & Bakar (2016), Brown, (2007), Manyaeva, Piskunov & Fomin, (2016), Ponkin & Redkina (2018), Xing & Yan (2018) and others.

The study of the theory and practice of the mechanism for the implementation of accounting functions led to the conclusion that the further use of the AWS of the accountant is irrational due to the limited capacity and low efficiency of solving accounting and information support for the organization’s management. The study of the organization of control systems, based on the use of modern computing tools involved such scientists as: Rybina (2017), Magomedov (2015), Karelin (2011) and a number of other scientists.

Research Questions

Considering the need for further scientific and practical development of innovative approach to the development of accounting and information support for the management of an organization, the main areas of research in this article are as follows:

study of the possibilities of using accounting for the development of information support for the management of the organization;

study of issues of harmonization of accounting subsystems and integration of the processing of economic information in the framework of the accounting system based on the formation of intelligent jobs in the framework of the ICS.

Purpose of the Study

In accordance with the designated problem area defined research objectives:

to substantiate the author's content of the concepts “information”, “accounting”, to determine the content of the accounting system formed on the basis of harmonization of accounting subsystems

to recommend the introduction of an IWP of an accountant on the basis of the formation of a data system, a knowledge system and integrated information processing.

Research Methods

To solve the problems of organizing and implementing accounting and information support for managing an organization, in the study were used the following methods:

systematization - the collection and streamlining of information from the scientific literature and other sources, which made it possible to conclude that the role of accounting has changed and to propose the organization of information support for managing the organization.

modelling - building a model of information support for managing an organization on the basis of AWP and IWP;

method of complexity - research and proposal for the organization of information support based on the complexity of the objects of management;

dialectical method - the study of the content of the concepts “information” and “accounting” in the context of increasing volumes, speed of information processing, improving the capabilities of technical means.

Findings

In the conditions of the digital economy and rapidly growing volumes of information, researchers are increasingly interested in the content of the concept “information”. Until recently, information in the general sense was considered as information about the world in which we live, a characteristic of a certain object, a message about something. With the advent of electronic computers, the understanding of information has become transformed and interconnected with computers as a source and user of such information.

In Russia, the legitimate definition of information was enshrined in the Federal Law “On Information, Information Technologies and Information Protection”: this is data, messages submitted in various forms (Federal Law of 27.07.2006 N 149-FZ "On Information, Information Technologies and Information Protection"). In consequence, in the adopted Digital Economy Program of the Russian Federation for 2017-2024 indicated that the basis of such an economy is information as a resource, a kind of asset that has unique and value (The Digital Economy Program of the Russian Federation for 2017-2024 (approved by Of the Government of the Russian Federation of 28.07.2017 No. 1632-p).

Thus, the understanding of the content of information at various stages of the technological development of the management of an organization is transforming. The study of the information system for managing an organization has allowed the concept of “information” to be interpreted as “useful knowledge”, which is the result of intellectual activity — knowledge in a particular field, formed by selecting and interpreting an array of information about a particular object. Such knowledge can be transformed into other information, used, disseminated to achieve a specific goal and make an appropriate decision.

One of the main sources of economic information used to manage an organization is accounting. The introduction of modern information technology management practices significantly changes the role of accounting in the information support system. If earlier the accounting, mainly, played the role of observing and recording the facts of economic life, i.e. was a supplier of information, now in the conditions of using modern information management systems, it became a user of information.

Currently, the main function of accounting is information management support based on the implementation of control and analytical tasks. In this regard, in our opinion, accounting should be understood as the systematization and processing of information about the facts of economic life through the implementation of control and analytical functions that ensure the management of reliable and complete information in accordance with the requests of users in a timely manner to make management decisions.

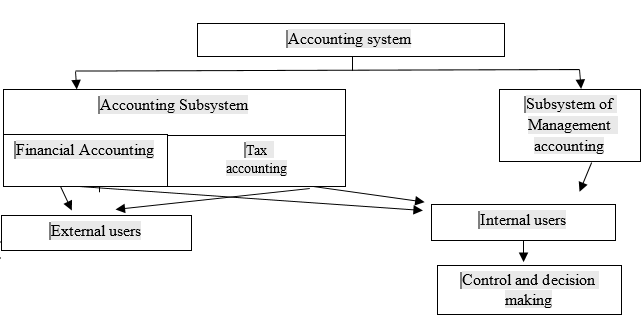

Taking into account that in the accounting system control and analytical functions can be implemented only in relation to the facts of economic life committed in the past, the study concludes that it is necessary to form an accounting system (Fig. 01) based on the harmonization of accounting subsystems (accounting, tax and management accounting) and integration of the processing system of the totality of information. It is the fulfilment of these requirements that will allow for an innovative approach to the information support of the organization's management.

Proposed in Fig.

The opinions of scientists about the independence of management accounting in the accounting system of a commercial organization are different. So, Kostyukova et al. (2018) in their scientific works indicate that management accounting is an independent area of accounting. The authors of this article have a different point of view and investigate management accounting as an independent accounting subsystem for the following reasons:

the possibility of reflecting in management accounting not only real facts of economic life, but also conditional, which may affect the change in the financial situation of the organization in the near future and are important for making management decisions;

particular requests of interested internal users;

confidential nature of information generated by management accounting;

dispositive nature of the implementation of management accounting, the lack of legislative regulation.

In the structure of the accounting system, the authors combine financial and tax accounting in the accounting subsystem by virtue of unity:

accounting methods: documentation, assessment, inventory, reporting, etc;

information users: internal users who are interested in information on tax calculations and obligations for making management decisions, external users in the face of regulatory authorities;

accounting objects: tax calculations and liabilities relate to accounting objects of both subsystems.

The proposed accounting system, based on the harmonization of accounting subsystems, allows generating information on real and conditional facts of economic life and implementing effective accounting and information support for interested users of information for making management decisions.

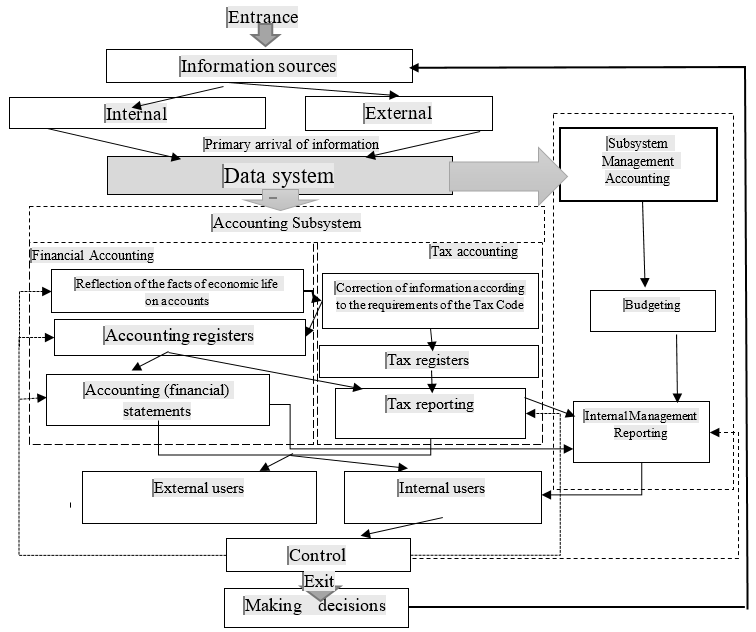

Until now, the main organizational form of accounting is the automated workplace (AWP), which is part of the model of accounting and information management support (Fig. 02). The organization of an automated workplace of the accountant, as a rule, based on the 1C Accounting software, which allows for fairly and reliably solving the accounting problems of all management objects and forming a system of data on the facts of economic life.

The presence in the organization of a formed data system greatly facilitates the transformation of information in accordance with user requests. This is due to:

centralization of current information about the facts of the economic life of the organization;

simplify access to this information;

providing reporting information in accordance with user requests.

Source: Authors

However, the 1C Accounting program, as well as the entire ACS system, built on a well-defined mathematical description of management in general and accounting in particular, does not allow fully harmonizing all accounting subsystems, providing an integrated information processing system and providing information on not previously provided requests when they cannot be unambiguously described.

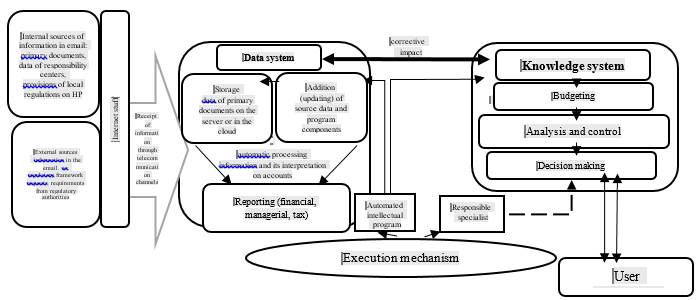

Further development of accounting should take place along the path of formation of an intelligent management system and intellectual accountant workplaces (IAWP), allowing to adapt to the working conditions and solve problems without direct human participation as experience (knowledge system) accumulates as a certain number of established corrections.

Fig.

Between the systems of knowledge and data, there is an inverse relationship, which is performed in the detection of inaccuracies, errors that require correction. The result of the interaction of a knowledge system and data systems is a completed task or an elaborated solution. The use of such a model of accounting and information support allows you to integrate information processing, harmonize all accounting subsystems and thereby increase the information content of the accounting data, the efficiency and reliability of the information necessary to make effective decisions.

Conclusion

As a result of the study, we made the following conclusions about solving the problems of an innovative approach to the formation of accounting and information support for the management of an organization:

one of the main resources of an economic entity in modern economic conditions is information, which is interpreted as “useful knowledge”, expressed as the result of intellectual activity — knowledge in a certain area. Such knowledge is formed by selecting and interpreting an array of information characterizing a particular control object;

the most important source of formation of accounting and information support for the management of an organization is an accounting system that includes: accounting (financial and tax) subsystems and management accounting. The article clarifies the content of accounting as a system of systematization and processing of information about the facts of economic life through the implementation of control and analytical functions that ensure the management of reliable and complete information in accordance with the requests of users in a timely manner for making management decisions. At the same time, the authors propose to include two subsystems in the accounting system: the financial and tax accounting subsystem. The proposed structure of the accounting system will ensure the harmonious development of all accounting subsystems;

in the conditions of a sharp increase in the volume of information and increasing requirements for it, there is a need for a critical assessment of the workstations used in practice and the formation of an integrated system for processing all the cumulative information necessary for managing an organization. The study made it possible to conclude that it is necessary to move from an automated data processing system to an intellectual one. In the conditions of an intellectual data processing system should be created intellectual workplaces (IWP), which are based on data systems and knowledge systems. Their interaction allows the accounting process to be carried out without direct human participation, which increases the objectivity, reliability and efficiency of the information provided to the interested user.

Thus, the development of accounting information management of the organization causes the need for further development of the accounting system based on the harmonization of accounting subsystems and information processing based on its integration. This, in turn, will serve as the basis for the innovative development of the information management of the organization based on the use of intelligent management systems, including intellectual accountant jobs. Solving the problem in the context of an ever-increasing flow of information and its processing speed reduces the subjectivity of the user perception of information, reduces the human factor in its processing and interpretation, and makes the decision-making process more objective and effective.

References

- Ali, B., Omar, W., & Bakar, R. (2016). Accounting Information System (AIS) and Organizational Performance: Moderating Effect of Organizational Culture. International Journal of Economics, Commerce and Management, 4, 138-158.

- Asatiani, A., & Penttinen, E. (2015). Managing the move to the cloud – analyzing the risks and opportunities of cloud-based accounting information systems. Journal of Information Technology Teaching Cases, 5 (1), 27-34.

- Brown, R. (2007). The Concise Guide to Mergers, Acquisitions and Divestitures. New York, NY: Palgrave Macmillan.

- Dam B., Dam, G., & Doan, V. (2017). The System of Management Accounting Information to Support Decision Making in Business. Accounting and Finance Research, 7 (1), 99-108.

- Karelin, V. (2011). Intellectual technologies and systems of artificial intelligence for decision-making support. Vestnik TUME, 2, 79-84. [in Rus].

- Kostyukova, E., Vakhrushina, M., Shirobokov, V., Feskova, M., & Neshchadimova, T. (2018). Improvement cost management system for management accounting. Research Journal of Pharmaceutical, Biological and Chemical Sciences, 2, 775-779.

- Magomedov, R. (2015). On the development of intelligent systems. The territory of science, 6, 39-44. [in Rus].

- Manyaeva, V., Piskunov, V., & Fomin, V. (2016). Strategic management accounting of company costs. International Review of Management and Marketing, 6 (5), 255-264.

- Ponkin, I., & Redkina, A. (2018). Artificial intelligence from the point of view of law. Vestnik RUDN. Jurisprudence, 22 (1), 91-109. https://dx.doi.org/10.22363/2313-2337-2018-22-1-91-109 [in Rus].

- Pyatov, M. (2018). Financial statements and new technologies. Accounting, 3, 82-91. [in Rus].

- Ragulina, J., Suglobov, A., & Melnik, M. (2018). Transformation of the role of a man in the system of entrepreneurship in the process of digitalization of the Russian economy. Quality - Access to Success, 2, 171-175.

- Rasporyazhenie Pravitelstva RF ot 28.07.2017 N 1632-r «Ob utverzhdenii programmy cifrovaya ehkonomika Rossijskoj Federacii» Retrieved from: http://www.consultant.ru/document/cons_doc_LAW_221756/ Accessed: 03.09.2018 [in Rus].

- Rybina, G. (2017). Intellectual technology for constructing training integrated expert systems: new opportunities. Open education, 4, 43-57. https://dx.doi.org/10.21686/1818-4243-2017-4-43-57. [in Rus].

- Strouhal, J., Horák, J., & Bokšová, J. (2017). Accounting Harmonization in V4-Countries and its Impact on Financial Data. International Advances in Economic Research, 23 (4), 431–432.

- Xing, X., & Yan, S. (2018). Accounting information quality and systematic risk. Finance and Accounting, 2, 1-19.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

20 March 2019

Article Doi

eBook ISBN

978-1-80296-056-3

Publisher

Future Academy

Volume

57

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1887

Subjects

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Piskunov, V., Bityukova, T., & Smagina, A. (2019). Innovative Approach To Accounting Information Support Of The Management Of The Organization. In V. Mantulenko (Ed.), Global Challenges and Prospects of the Modern Economic Development, vol 57. European Proceedings of Social and Behavioural Sciences (pp. 780-789). Future Academy. https://doi.org/10.15405/epsbs.2019.03.77