The article is devoted to the development of a model for assessing and reducing the financial risks of a company in modern conditions. The importance of study is determined by the need for the development of identification tools, measurement and management of financial risks, as well as theoretical and methodological approaches, which assessing the relationship of financial risks. The performance of companies and the practical significance of assessing the impact of financial risks on the performance of companies in order to develop strategies and tactics for effective development are also important. The purpose of the study is to develop the theoretical and methodological tools for assessing the impact of financial risks on the performance of Russian companies in the petroleum engineering industry, as well as managing financial risks for effectiveness’s growth. Based on the results of the work, an integrated risk management model was proposed for the company. The model includes a quantitative assessment of the positive performance of the company based on the probit-model and a management decision-making matrix based on an assessment of the impact of financial risks on the performance of companies using the method of scenario analysis. The article presents an integral model for evaluating the performance of companies, developed taking into account existing quantitative and qualitative assessment models.

In modern conditions of global economic and political uncertainty, a large number of factors, including industrial, technological, socio - economic and financial nature, influences the volatility of the conjuncture of world and national markets, the efficiency of companies. The impact of these factors is the cause of financial risks in the activities of companies.

Identification of methods and models of financial risk management to identify hidden threats and shortcomings in the activities of companies, to identify ways to overcome the crisis, to achieve high financial performance of companies is a pressing issue.

Regardless of the industry and the main activities of a commercial organization, the key criterion for assessing the significance of risk is the level of potential losses. The higher the probability of loss and the greater their magnitude, the more significant the impact of the relevant risk factors on the company's operations.

We used the methods of scientific abstraction, comparison, classification, mass observations, scientific synthesis, grouping, statistical and graphical analysis, expert assessments, etc. In addition, the study applied the methods of mathematical modeling, correlation and regression analysis.

Problem Statement

To assess the current and potential changes in the company's financial position, to justify the assessment of various management decisions, it is necessary to assess the level of possible losses or lost profit.

Research Questions

Consideration of the methodological tools for assessing the financial condition and risk of bankruptcy of companies and the development of an integrated model of risk management of the company.

Purpose of the Study

The purpose of the study is to develop the theoretical and methodological tools for assessing the impact of financial risks on the performance of russian companies in the petroleum engineering industry, as well as managing financial risks for effectiveness’s growth.

Research Methods

Methods for assessing the financial condition of companies

Comprehensive analysis and systematization of methodological approaches to assessing the financial standing of the company represented in the works of russian (

Bulava & Shamsurdinova, 2016;

Evstratov, 2012;

Shumilova & Karataev, 2012;

Yasnitsky, Ivanov, & Lipatova, 2014) and foreign authors (

Almamy, Aston, & Ngwa, 2016;

Angels Fito, Plana-Erta, & Llobet, 2018;

Boda & Uradnicek, 2016;

Issah & Antwi, 2017;

Klepáč & Hampel, 2018;

Manzaneque, Priego, & Merino, 2016;

Postolov et al., 2016;

Tinoco & Wilson, 2013) allowed to develop the detailed classification of these methods.

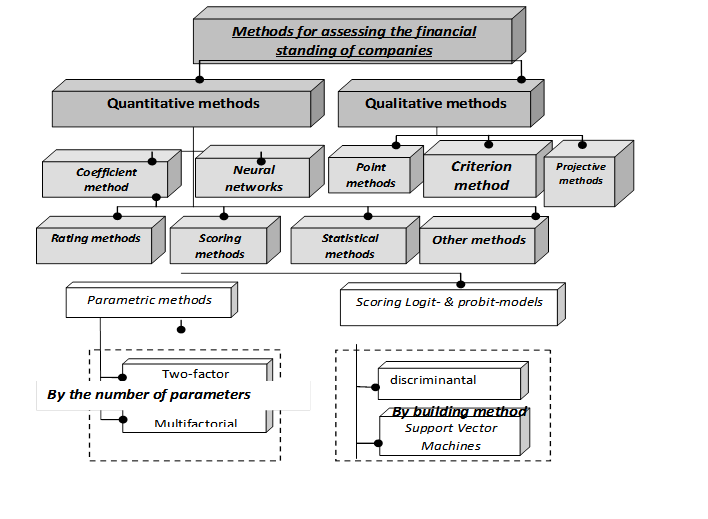

The classification of methods for assessing the financial standing of the companies is presented in the Figure

1

.

The study showed that the majority of modern models for evaluating the effectiveness of companies are built to more accurately assess their risks, which leads to the prevalence of bankruptcy risk assessment models or the probability of default. These models consider the company's activities from the standpoint of the inefficiency of its activities, while insufficient attention is paid to the definition of the company's performance.

Figure 1: Classification of methods for assessing the financial standing of companies

At the same time, the assessment of profitability or efficiency, as a rule, is one of the components of the assessment, and many models take into account only the presence of the total profit at the date of the assessment. This approach does not take into account the history and development prospects of the company, as well as the long-term interests of its employees, owners and investors. Current studies show that to correctly forecast the financial performance of companies, it is necessary to build complex models using the tools of the economic, mathematical and statistical sciences.

Review of the current practice of bankruptcy risk assessment of companies

The analysis of foreign and Russian works in the field of companies ’default risk assessment allowed grouping statistical models used for risk assessment into 2 main categories (see figure

01

.):

Most of the parametric models for evaluating companies are built on the basis of a total assessment of the influence of individual factors on the resulting indicator, as a result of which their distribution into two-factor and multifactorial factors seems reasonable. (figure

01

). In general, most of the parametric models for estimating the probability of default are described by following mathematical formula:

(1)

x

i

– various company performance indicators;

c

i

– weights.

At the same time, as shown in diagram 01, parametric assessment models can be grouped by methods of their construction, dividing into discriminant methods and SVM-models.

It is known that in 1966 Beaver (

1966) developed a five-factor model for predicting a company's bankruptcy. The scientific novelty of this model was to use the ratios of financial indicators to predict a possible default. At the same time, the financial indicators used in this system were not weighed. This discriminant method also does not provide an opportunity to calculate the immediate probability of a simulated event.

Altman (

1968) proposed the calculation of the composite index of financial condition later. Based on several financial indicators and weights, the resulting (integral) indicator-Altman index is calculated.

This index is formed using a multifactor discriminant analysis (MDA) and allows you to identify potential bankrupts from among commercial companies. Then it is compared with empirically established values, the excess of which means a high or low probability of the company's default.

Altman index (Z-score) can be represented as an equation:

(2)

;

;

;

;

;

After the described models, discriminant analysis was used to create a variety of models for estimating the probability of companies' default by foreign and russian scientists.

For developed on the basis of discriminant analysis of models for evaluating companies, relatively high accuracy is typical.

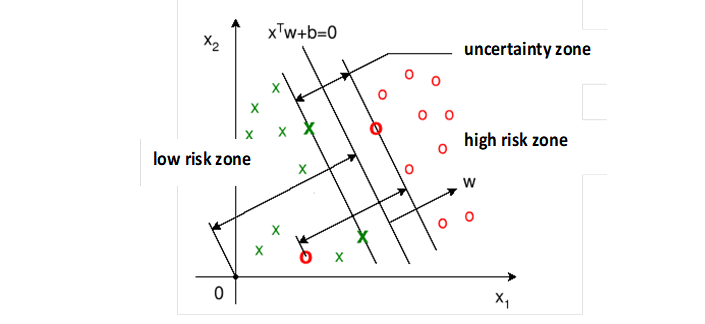

Statistical Support Vector Machines (SVM-models) provide a fairly low forecast error in combination with a small number of factors used to assess the company's financial position. To build an SVM model, you need to create a function:

(3)

Where:

supporting vectors;

weights.

For each value of the function f (x) there is only one value of the probability of company default. As shown in Figure

2

, a straight line

separates classes of companies with high and low risk of bankruptcy.

An important advantage of the SVM-model is the ability to take into account the qualitative characteristics of the studied companies by introducing additional variables. An example of such a model is the work of Härdle, Moro, & Schäfer (

2005).

Statistical models, where the probability of occurrence of an event is estimated using available information, are scoring. Thus, scoring can be attributed to models that involve the calculation and summation of data of private indicators, taking into account the assigned weights to obtain a common summary assessment - score.

The scoring and rating risk assessment models are most widely used to assess banking risks, which indicates the practical applicability and reliability of such methods.

The analysis of statistical models for evaluating companies will not be complete if it does not affect the so-called neural networks.

Neural networks are mathematical prediction methods based on available information about previously observed states and \ or anticipated system changes.

One of the most relevant is the method called “Kohonen network clusters” (KCN).

Currently, neural network modeling shows the greatest accuracy of the results. At the same time, this approach requires the use of internal company information and specially developed software products (otherwise the results will not be accurate), which makes analysis of companies very difficult.

In addition, in practice, various scoring methods are often used. Currently, such systems are used in the largest holdings in the USA and Western Europe due to their versatility and high efficiency. In addition, banks often use the methods of comprehensive assessment of bankruptcy risk of companies.

Logit and probit models are usually combined into a special group of models for evaluating company performance. These models have been widely used since the 80s ХХ century.

A team of authors of Lancaster University Management School, Minussi, Soopramainen, & Worthington (

2007) presented the most relevant example of logit models in 2007.

This model was created on the basis of financial indicators of Brazilian companies, whose economy is similar to the Russian one, which causes additional scientific interest for Russian researchers on this topic.

Risk assessment of companies based on the model under consideration assumes the substitution of source data into the following expressions.

(4)

;

Where:

F/OWKSA – ratio of short-term capital to revenue;

FINLEV – leverage;

INTCOV – security of interests;

OWKSA – own working capital / revenue;

NWKSA – required working capital / revenue.

The formula of logit regression proposed by I.B. Kopelev (

2016) is one of the most relevant scoring models.:

(5)

With its help, the fact of the company's default on the time horizon of 2-3 years can be predicted. A distinctive feature of this method can be the inclusion in the model of additional factors that allow to take into account external economic conditions. For example, by taking into account the dynamics of stock index fluctuations.

The study revealed that most modern models for evaluating the effectiveness of companies are built to more accurately assess their risks, which largely determines the prevalence of bankruptcy risk assessment models or the probability of default. These models consider the company's activities from the standpoint of the inefficiency of its activities, while insufficient attention is paid to the definition of the company's efficiency.

In the models discussed above, the assessment of profitability or efficiency is one of the components of the assessment, and many models only take into account the presence of total profit on the date of assessment. This approach does not take into account the history and development prospects of the company, as well as the long-term interests of its employees, owners and investors.

Development of a probit-model for assessing the company's financial position

The purpose of the article is to present a model for evaluating a positive financial result. Accordingly, from a quantitative point of view, a binary definition is sufficient whether a company is profitable or not. The most accurate estimate of binary values is presented in probit-regression models, since their mathematical properties maximally simplify the answer to the basic question, without considering further changes to other factors.

One of the most well-known probit-models used to assess the financial position of a company is the model proposed by M. Zmievsky in 1983 (

Zmijewski, 1983). It is based on three financial indicators for a sample of 40 bankrupt companies and 800 operating companies whose shares were traded on the New York Stock Exchange (NYSE) in the years 1972-1978. According to this model, the probability of a company's bankruptcy is given by a function of the variable Z:

(6)

P = f(Z)

Х1 – net profit to asset ratio;

Х2 – ratio of liabilities to assets;

Х3 – current assets to current liabilities;

f – standard normal distribution function (has a mean of 0 and standard deviation of 1).

Р – probability of bankruptcy.

To identify the main factors of a positive assessment of the effectiveness of companies, a probit model was built, as in the framework of this study it was necessary to construct combinations of factors with the highest probability leading to a positive assessment of the company’s activities.

It is impossible to draw a precise line by dividing companies into good and bad. However, it is necessary to minimize the probability of error. So the parameters of the model were selected, in which the change in the model risk factors would be the maximum possible probability for the model being constructed to change the measured indicator – the company's performance.

As a result, a model was developed that has the following form:

(7)

Simulated coefficients for each of the parameters were calculated in the framework of the model approbation:

– company assets;

– company capital;

– revenue;

– investments.

The constructed multi-factor model for assessing the impact of financial risks on the performance of companies (the scoring model) involves not only the selection of the most significant factors, but also the selection of simulated coefficients and the calibration of the scoring model.

When testing the model, the following results were obtained. In the presented model, there is no heteroscedasticity (non-constant dispersion of random error), which often manifests itself in the case of heterogeneity of observations. The presence of heteroscedasticity leads to ineffective estimates. Errors are distributed according to normal law. This model gives the correct assessment of the effectiveness of the company in 722 cases out of 965 observations (results of 193 companies for each of 5 consecutive years). This corresponds to a confidence level of 75% (722:965=0,748186).

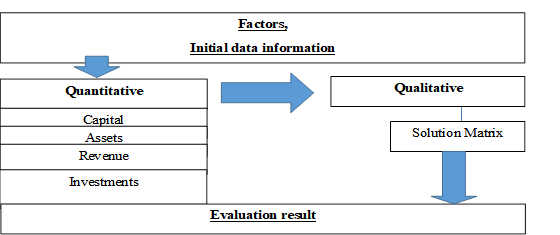

Management decision-making scheme based on identified financial risks

In addition to the quantitative assessment presented in the developed model, a qualitative solution is proposed based on the decision matrix, which is presented in figure

03

.

The proposed scheme of management decision making by the management and owners of the company consists of 5 stages.

Stage I. Collection of quantitative information. At this stage, it is necessary to prepare the initial quantitative data for the scoring model. To do this, the manager must collect accounting, management and / or analytical reports that are relevant at the time of evaluating the company's activities.

Stage II. Entering quantitative data and evaluating it with a probit model. At this stage, it is necessary to enter into the scoring model the information collected in Stage I. This information should contain data on such financial indicators as:

Figure 3: The structure of data factors for a multifactor model for assessing the impact of financial risks on the performance of companies

The result of this stage is a quantitative assessment of the probability of obtaining a positive financial result.

Stage III. Depending on the result of the quantitative assessment, the manager assesses the need to adjust the company's work. Obviously, the need for adjustment increases as the probability of obtaining a positive financial result decreases on a scale from 0 to 100%.

Stage IV. Preparing a decision matrix. Based on the criteria in Table

01

, a decision matrix is built. Subsequent options are evaluated based on established criteria.

For each of the selected criteria of the decision matrix, the corresponding column is filled in with an assessment of the impact on the company's financial performance. As a result, we obtain a formalized matrix for evaluating the effectiveness of the company’s activities and options for its improvement.

To obtain the resulting indicator in points, the values from the “Significance” column are multiplied by the corresponding criterion scores and the values obtained are added together.

For example, the final score for the “Leaving the industry” is calculated as follows:

In the future, the results obtained in the process of applying the scoring model and using the decision matrix can be compared and used together to make a decision on the company's activities in terms of quantitative and qualitative characteristics. Such a comparison allows both to reasonably determine the quantitative parameters of improving the efficiency of companies, as well as to determine the most preferable options for the company's owners.

Findings

The developed model of the influence of risk factors on the performance of companies has been developed in accordance with international approaches to assessing the level of risks taken by companies (Integrated Risk Management Model, SOSO ERM), and the principles of providing information on the financial position and performance of companies based on International Financial Reporting Standards (IFRS).

A management decision-making matrix based on identified financial risks has been developed. The matrix is the relation of indicators affecting the performance of the company of petroleum engineering, and the possible directions of changes in the company’s activities. It allows you to create different scenarios for the development of the company (less risky or the most effective).

A set of tools for managing financial risks taking into account the assessment of the impact on the performance of petroleum engineering companies.

Conclusion

The article presents an integral model for evaluating the performance of companies, developed taking into account existing quantitative and qualitative assessment models.

A multi-factor model for assessing the impact of financial risks on the performance of companies has been developed.

A management decision-making matrix based on the level of financial risks taken has been developed, which allows, based on stress testing, to apply scenario analysis to make optimal management decisions from the standpoint of improving the efficiency of companies.

An integrated approach allows the timely development of a package of anti-crisis measures aimed at improving the efficiency of companies and, thus, increasing financial stability, economic security of enterprises, the economy of the country as a whole.

References

Almamy, J., Aston, J., & Ngwa, L.N. (2016). An evaluation of Altman's Z-score using cash flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the UK. Journal of Corporate Finance, 36, 278-285.

Altman, E.I. (1968). Financial rations. Discriminent analysis, and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589-609.

Angels Fito, M., Plana-Erta, D., & Llobet, J. (2018). Usefulness of Z scoring models in the early detection of financial problems in bankrupt Spanish companies. Intangible Capital, 14(1), 162-170.

Beaver, W.H. (1966). Financial rations and predictions of failure. Empirical research in accounting: Selected studies, 4, 71–102.

Boda, M., & Uradnicek, V. (2016). The portability of Altman’s Z – score model to predicting corporate financial distress of slovak companies. Technological and Economic Development of Economy, 22(4), 532-553.

Bulava, I.V., & Shamsurdinova, E.R. (2016). Enterpreneurial risks and their connection with financial results. Economy and Entrepreneurship, 1-2(66), 907-911.

Evstratov, R.M. (2012). Analysis of the main economic and mathematical models for assessing the financial risks of commercial organizations. Vector Science of Togliatti State University. Series: Economics and Management, 4(11), 56-59.

Härdle, W., Moro, R.A., & Schäfer, D. (2005). Predicting bankruptcy with support vector machines. SFB 649, Economic Risk. Discussion Paper 2005-009. Berlin: CASE - Center for Applied Statistics and Economics, HumboldtUniversität, German Institute for Economic Research (DIW). URL: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.633.4182&rep=rep1&type=pdf.

International Risk Management Standard COSO ERM (Enterprise Risk Management - Integrated Framework). URL: https://www.coso.org/Pages/erm-integratedframework.aspx. Accessed: 21/08/2018.

Issah, M., & Antwi, S. (2017). Role of macroeconomic variables on firms’ performance: Evidence from the UK. Cogent Economics & Finance, 5(1), 1-18. URL: https://www.tandfonline.com/doi/pdf/10.1080/23322039.2017.1405581?needAccess=true.

Klepáč, V., & Hampel, D. (2018). Predicting bankruptcy of manufacturing companies in EU. E+M Ekonomie a Management, 1(21), 159-174

Kopelev, I.B. (2016). Evaluation and prediction of the risk of financial insolvency of the company (Doctoral dissertation). Moscow: Financial University under the Government of the Russian Federation.

Manzaneque, M., Priego, A.M., & Merino, E. (2016). Corporate governance effect on financial distress likelihood: Evidence from Spain. Revista de Contabilidad – Spanish Accounting Review, 19(1), 111-121.

Minussi, J., Soopramainien, D., & Worthington, D. (2007). Statistical modelling to predict corporate default for Brazilian companies in the context of Basel II using a new set of financial ratios. Working Paper 2007/008. Lancaster, U.K.: The Department of Management Science Lancaster University Management School.

Postolov, K., Milenkovic, I., Milenkovic, D., & Lliev, A.J. (2016). Influence of market values of enterprise on objectivity of the Altman Z-Model in the period 2006-2012: Case of the Republic of Macedonia and Republic of Serbia. Journal of Central Banking Theory and Practice, 5(3-3), 47-59.

Shumilova, V.M., & Karataev, A.S. (2012). Information model for assessing financial risks. Modern Problems of Science and Education. Penza: Publishing House "Academy of Natural History".

Tinoco, H. M., & Wilson, N. (2013). Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. International Review of Financial Analysis, 30, 394-419.

Tinoco, M.H., & Wilson, N. (2013). Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. International Review of Financial Analysis, 30, 394-419.

Yasnitsky L.N., Ivanov D.V., & Lipatova D.V. (2014). Neural network system for assessing the probability of bank failure. Business Informatics, 3 (29), 49-56

Zmijewski, M. E. (1983). Essays on corporate bankruptcy (Doctoral dissertation). State University of New York at Buffalo.

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Bulava,

I.,

Mingaliev,

K.,

&

Shamsutdinova,

E.

(2019). Integrated Risk Management Model Of The Company. In

V.

Mantulenko

(Ed.),

Global Challenges and Prospects of the Modern Economic Development, vol 57. European Proceedings of Social and Behavioural Sciences (pp. 137-147).

Future Academy. https://doi.org/10.15405/epsbs.2019.03.14

We use cookies or similar technologies to access personal data, including page visits and your IP address.

We use this information about you, your devices and your online interactions with us to provide, analyse and improve our services.

This may include personalising content or advertising for you. You can find out more in our

privacy policy and

cookie policy and

manage the choices available to you at any time by going to ‘Privacy settings’ at the bottom of any page.

Manage My Preferences

You have control over your personal data. For more detailed information about your personal data, please see our

Privacy Policy and Cookie Policy.

These cookies are essential in order to enable you to move around the site and use its features, such as accessing secure areas of the site.

Without these cookies, services you have asked for cannot be provided.

Third-party advertising and social media cookies are used to

(1) deliver advertisements more relevant to you and your interests;

(2) limit the number of times you see an advertisement;

(3) help measure the effectiveness of the advertising campaign; and

(4) understand people’s behavior after they view an advertisement.

They remember that you have visited a site and quite often they will be linked to site functionality provided by the other organization.

This may impact the content and messages you see on other websites you visit.