Corporate Social Responsibility In Russia: Motives And Features

Abstract

The concept of corporate social responsibility (CSR) has evolved over the past few decades. The researchers focus on the issues of interaction between society and business, the relationship of CSR with corporate strategy, the impact of CSR on business performance indicators. Despite the numerous research works in this area, there is uncertainty in understanding the essence, goals, directions and tools of CSR by various groups of stakeholders. In addition, changes in the political, economic and technological conditions of the development of modern society affect the content and effectiveness of CSR. A separate issue is the information transparency of companies, their public openness and documentation of CSR. CSR issues are relatively new for Russia. At present, there is an increase in the public activity of Russian companies that implement social projects, participate in charitable activities and share information about the funds allocated and the results obtained. Along with financial statements, over the past few years, representatives of large Russian businesses have published reports on sustainable development, which include data on CSR. However, not all companies, including public ones, place such information. The goals and motives for CSR of Russian companies are not clear. Several hypotheses are tested in the present study on the basis of comparison with the results of CSR research in other countries and the analysis of social reporting of Russian companies. The study aims to identify specific features of CSR in Russia, to determine objectives and reasons for CSR, the influence of key stakeholder groups.

Keywords: CSRsocial enterpriseCSR reportingcorporate philanthropy

Introduction

Sustainable formation of social and ethical approach to business occurred in the 1940s, when there was a growing opinion about the obligations of business to society and the need for companies to direct part of their funds for its development. Н. Воwen first formulated the term “social responsibility of a businessman” and presented its interpretation in his work of the same name. In his opinion, businessmen are obliged to pursue the policy, to make decisions, or to follow the goals that are desirable in terms of the goals and values of the whole society (Воwen, 1953).

The strongest criticism of the socio-ethical approach was made by supporters of “corporate egoism” approach, namely by T. Levitt and Nobel laureate M. Friedman. In his article “Threats to social responsibility” Levitt (1958) argues that business will have a significantly greater chance of survival if it abandons such an absurd view on its own goals, leaving profit maximization as the only long-term goal both in theory and in practice (Levitt, 1958). Mr. Friedman's phrase “business of business is business” illustrates his strong opinion that to achieve socially responsible position means to organize production in the most effective way (Friedman, 1970, p. 17.). Supporters of the “corporate altruism” approach formed, perhaps, as a response to the work by M. Friedman, provide a new rationale for corporate social policy. А. Freeman, in his work “Strategic management: stakeholder approach” (Freeman, 1984), suggests the concept of stakeholders. A. Phillips discloses the “equity principle of stakeholders” (Phillips, 2003). J.Post notes that the corporation is involved in the mobilization of productive resources in order to create welfare for their own stakeholders and the company competitive advantages (Post, 2002).

An important stage in the development of the concept of social responsibility of business is the development of bilateral relations, when the company responds quickly to social needs of society and stakeholders. Ackerman (1975) considers corporate social activity as a necessary operational reply on stakeholders requests. Windsor (2001) proposed an alternative approach to CSR, in terms of “global corporate citizenship” and “economic concept of responsibility”.

CSR definition by Carroll (1991), implying compliance with the economic, legal, ethical and discretionary expectations imposed by society on the company in a given period, became widespread. Later, the author presented a triangular model that reflects the multilevel responsibility: economic, legal, ethical and philanthropic. Carroll model (1991) presents not only the ordered content of CSR, but also the systematization of the “normative levels”. Economic and social responsibility are obligatory for business, they meet strict public requirements; the ethical responsibility of society is expected, while the philanthropic one is only desirable.

The model embodied in the concept of corporate social activity was recognized both by scientific and business communities (corporate social performance – CSP). This concept was developed successively by Carroll (1991), Wartick & Cochran (1985) and implemented in the works by Wood (1991), and Swanson & Orlitzky (2017). Wood (1991) noted that corporate social activity is a system of company’s principles of social responsibility, social sensitivity and interaction with the company's stakeholders.

A systematic approach that combines the principles of social responsibility and corporate values is relevant for today.

Problem Statement

As evidenced by the Laws of Hammurabi (XIIIV century BC), the Pentateuch of Moses, and other ancient sources, issues of social responsibility arose before humanity for thousands of years. The centuries-old experience of non-profit organizations activities and private philanthropic practices in the fields of health, poverty and hunger combating, children protection, ecology, refugee assistance, social entrepreneurship, etc. is reflected in the historical memory and culture of people. Why is the concept of social responsibility becoming so relevant for business only now?

Modern researchers consider CSR through the prism of stakeholders' interests (Fu, Boehe, Orlitzky, & Swanson, 2018; Lim & Grennwood, 2017; Martínez, Fernández, & Fernández, 2016; McCarthy, Oliver, & Song, 2017; Park, Joon, & Kwon, 2017). What do customers, experts and professional investors mean by CSR? Are Russian companies ready to respond to social demand of the society and stakeholders?

Wartick & Cochran (1985) believe that corporate social activities are carried out through “social policy” and should be considered as a fundamental relationship between the principles of social responsibility of business, the process of social sensitivity and corporate strategy. Do Russian companies develop strategies in the field of philanthropy and sustainable growth? Is the practice of documented consolidation of these strategies common?

Carroll (1991) in the article “Four facets of corporate citizenship” writes that company is expected to show responsibility, just as it is expected from other citizens. The problems of social responsibility become relevant not only for companies, but also for the State (Boulouta & Pitelis, 2014; Solke, 2014; Khairov & Khametov, 2014). A number of authors study the decision-making within the framework of corporate social responsibility and corporate social irresponsibility (CSI) (Armstrong & Green, 2013), as well as the impact of CSR and CSI on the perception and efficiency of business (Kuratko, McMullen, Hornsby, & Jackson, 2017; Price & Sun, 2017). How do companies try to change corporate behavior in order to meet prevailing social norms, values and expectations? Does this correspond to leading researchers’ opinion on corporate social sensitivity?

Research Questions

The following hypotheses are tested in the study:

Business cannot exist in isolation from society, business must respond to social problems.

Social responsibility of business is view as an opportunity to achieve strategic benefits, including competitive advantages.

CSR in Russia has specific features that make it different from other foreign countries practices.

Relationship between business and society

Questions to be researched:

How does society influence business?

What expectations do people have?

CSR and the concept of sustainable development

Questions to be researched:

How do stakeholders influence CSR decisions?

Is CSR activity documented?

Features of CSR in Russia

Questions to be researched:

What are the reasons, objectives, directions and expected results of CSR in Russia?

Are there any specific features of CSR in Russia?

Purpose of the Study

-

To test hypotheses on the mutual influence of business and society.

-

To identify the reasons for interest in CSR activity in Russia, as well as the objectives and directions of this activity.

-

To determine the specific features of CSR in Russia.

Research Methods

The analysis and synthesis of fragmented data on the activity of Russian companies in the field of CSR are used as research methods. Comparative evaluation to identify the causes and objectives of CSR in the Russian market is based on a comparison of the results of the content analysis of CR reports placed by Russian companies and the results of external studies.

Systematization of data on the basis of analytical companies’ research

To compare CSR activities of Russian companies with foreign CSR practice, the research reports of Deloitte, KPMG and Aflac, the Association of grant-making organizations in Russia "Donor Forum" were used. Deloitte and KPMG surveys cover respondents from different business areas on all continents. The National Survey on Corporate Social Responsibility. Consumers, Professional Investors and CSR executives. Findings and executive summary (Analytical statement, 2018a) study collected assessments of CSR executives, investment professionals and consumers aged 18 years and older from USA.

Participants in the "Forum of Donors" research in 2017 were 52 companies that provided data on corporate philanthropy in Russia for 2016.

Assessment of the degree of institutionalization of the social responsibility of business in the Russian Federation on the basis of the analysis of company reporting

The methodological basis for assessing the formation of the institution of social responsibility of business in the Russian Federation was the identification of the existence of companies’ activities aimed at the development of society and the improvement of life quality, as well as the factors of its development.

Selection of companies that placed CSR reports in open sources

The assessment of changes in public reporting of companies was made as an evidence of the need to adopt new rules and regulations for business, as a response to social request of the society and stakeholders.

Non-financial reporting of Russian companies in the field of CSR and sustainable development was studied. 16 companies operating in different industries with annual revenues of more than 100 billion rubles ($1.7 bln) (according to 2017 data) were selected. The list of companies is presented in Table

The research included only publicly available non-financial and integrated reports for 2017.

** Operating income before provisions

Findings

The studies reflect the changes in the minds of business leaders worldwide. For example, in the Deloitte study (The 2018 Deloitte Global Human Capital Trends) the phenomenon of a social enterprise is considered. A social enterprise is an organization whose mission combines revenues and profit growth with the need to consider and support the interests of the community and stakeholders. It is responsible for its actions both inside and outside the organization, acting as a role model and promoting a high degree of cooperation at all levels of the organization. Other studies show uneven changes in the social activity of companies around the world (Analytical statement, 2017a) and ambiguity in the attitudes of individual groups of stakeholders (Analytical statement, 2018b), but reflect a trend of increasing interest in CSR and greater openness in information exchange.

Despite the growing interest in CSR over the past 10 years, the understanding of the need for CSR activity in Russia is still being formed, the tools and directions used are limited, projects in the field of social entrepreneurship are few.

Opinions and attitudes towards CSR among the participants of the world market

According to National Survey on Corporate Social Responsibility (Analytical statement, 2018a) consumers, professional investors and CSR executives have different views on motives, purposes, directions and expected results of CSR (Table

Comparison of opinions of experts, consumers and professional investors shows the principal differences between them in the understanding of CSR:

There is no universal CSR definition and system of assessment of CSR results among professionals.

The reasons that determine CSR are related to the growth of business transparency and pressure of stakeholders, including consumers, employees, shareholders.

Consumers are more likely to get results in the form of benefits for society, professionals are focused on the benefits for companies (experts) or stakeholders (investors).

Consumers are interested in what they can get from CSR activities of companies, and companies are interested in what they can lose if they are not engaged in CSR.

Social responsibility of business is taken into account when assessing the feasibility of investments.

According to the KPMG Survey, CR reporting is standard practice for large and mid-cap companies around the world. There was a strong growth in CR reporting across a number of countries between 2015 and 2017. As for Russia it recorded increase by 7 percentage points from 66% up to 73% with CR reporting rate higher than the global average (Analytical statement, 2017b).

Social activity of business increases for the following reasons (The rise of the social enterprise. 2018 Deloitte Global Human Capital Trends):

The importance of the individual is growing, and Millennials are putting increasing pressure on business. Young people question the basic prerequisites of corporate behavior, economic and social principles that guide it (The 2017 Deloitte millennial survey: Apprehensive millennials: Seeking stability and opportunities in an uncertain world). For this group, social capital plays a huge role in deciding where they work and what they buy, and 86% believe that business success should be measured not only by financial indicators.

It is expected that business will fill the vacuum of political leadership. People have less confidence in their political and social institutions and expect business leaders to fill this gap. This expectation puts enormous pressure on companies, but also creates opportunities. Organizations that interact with people and demonstrate that they are trustworthy, improve their reputation and influence traditional public policy mechanisms. On the other hand, companies that seem alienated face negative media reactions, unflattering social media reviews, and difficult questions from stakeholders.

Technological changes have an unintended impact on society, even when it creates opportunities for sustainable growth. Information and technological changes allow people to observe companies in real time, expressing their opinions to a wide audience, uniting in social communities and influencing decision-making.

Thus, being a socially responsible company means to listen carefully to external and internal environment, business partners and customers, as well as the society, the company influences and is influenced by. According to “The business case for inclusive growth: Deloitte Global’s inclusive growth survey report” (Analytical statement, 2018b), 65% of companies’ executives rated “inclusive growth” among top-three strategic concerns. This is important for maintaining the reputation of the company; involvement and retention of critical workers; customer loyalty growth. Being a social enterprise also means to invest in a broader social ecosystem, starting with the company's own employees, including all workers – on- and off-balance-sheet.

Opinions and attitudes towards CSR among the participants of the Russian market

Since 2008 the “Leaders of Russia” project, organized by the Association of grant-holders with the support of PwC, has been implemented in Russia. The project involves Russian companies that carry out CSR activities, participate in charity and share information with the fund. 52 Russian and international companies, with a total turnover of more than 100 million rubles ($1.5 mln) in 2016, took part in the study (Boldyireva, 2017). According to the data provided, they spent more than 43.8 billion rubles ($652 mln) on charity and social support. For comparison: 11.8 billion rubles ($401 mln) were spent to support social initiatives in 2011, 13.4 billion rubles ($426 mln) - in 2012-2013, 19.9 billion rubles ($325 mln) - in 2015.

Motives

More than half of the respondent companies (54%) give moral reasons to justify their charitable activities. The desire to help socially unprotected segments of the population, to be realized in society outside the sphere of business, to use the resources more responsibly are motives for these companies. Respondent companies are more sensitive to social problems that are visible to society (help to orphanages, people with serious diseases, solving environmental problems), but to a lesser extent try to link corporate charity with the overall corporate strategy. In most cases, the strategy and policy of corporate philanthropy are broadcast by parent companies operating in foreign markets.

Involuntary reasons for corporate philanthropy are named by a third of respondents. This implies the presence of stimulating expectations from outside stakeholders. Among such expectations are proposals from state and municipal authorities; requests from non-profit organizations and individuals; expectations of real and potential business partners, especially foreign ones, for whom corporate charity is one of the system-forming practices; additional attention to business from consumers and local communities in connection with the specificity of the product (for example, tobacco and alcohol products). Besides, involuntary reasons are named by city-forming enterprises that are the main employers in their regions. They are forced to respond to social problems of employees, otherwise they may face difficulties in hiring, motivating and retaining staff.

29% of the respondents indicate the economic reasons for charitable activities. Companies associate charity with ensuring the sustainability of the company through long-term investments in the standard of living of local communities. There is also a reputational component of charity and its role in the formation of corporate culture.

Directions

The choice of directions, as a rule, corresponds to the general global strategy, although the companies often have the opportunity to further respond to the requests of local communities. Almost all respondent companies (94%) note the need to address their chosen social problems. More than half of the companies (58%) consider it important to increase business sustainability through the development of regions where they operate. A third of respondents (35%) indicate the enhancement of reputation in the market of goods/services as one of the goals of corporate philanthropy, others think about their brand’s enhancement in the labor market (27%) and relationships with business partners (23%). Employees competencies and corporate culture enhancement, noted by 37% of respondents, is linked mainly with the development of corporate volunteering programs.

Expected results

Almost all of the respondents are in one way or another guided by the creation of social values. As for commercial value, 72% of companies note the need to generate it in one form or another.

Most companies consciously work to create “shared” value through charitable programs, with more than half of them emphasizing the relationship between sustainable business development and sustainability of local communities. With regard to the so-called “mixed” value (blended value) emerging from intersectoral collaboration, almost half of the respondents note the need for partnership efforts to solve social problems.

Management/stakeholders support

More than 70% of the respondents note the importance of stakeholders such as employees (94%), beneficiaries (90%), shareholders, non-profit organizations (87%), local communities (81%) and authorities (79%). Other stakeholders include business partners, media, professional communities.

Shareholders, beneficiaries and local communities are named as key stakeholders. This is because shareholders are the recipients of commercial value, beneficiaries are the recipients of social value, and the role of local communities is considered by companies through the concept of sustainable development and correlates with the creation of common value.

Analysis of Russian companies CSR reporting

The analyzed reports on corporate social activities have different names: social reports (VTB Bank, Nestle Russia), reports on sustainable development (NOVATEK, Rosneft, Rostelecom), report on social responsibility and corporate sustainable development (ROSSETI). Sometimes they are included as a separate part in the company's annual report (PHOSAGRO, X5 Retail Group).

More than half of the reports contained data on the amount of the company's investments in society development programs (Table

Environmental activities of companies are also paid attention to in all reports. At the same time, the most detailed data on compliance with environmental requirements, the description of environmental policy and environmental measures are presented by companies of chemical and mining industry, ferrous and nonferrous metallurgy, gas production and gas and oil refining.

All reports but in different degrees contain information on the participation of companies in charitable activities. Only a few respondents reflect the amount of money allocated for charity, show the real results of targeted assistance.

The reports also reflect the results of the organization of charitable actions, which essentially initiate charity from citizens (X5 Retail Group) and sponsorship (Rosneft, Sberbank, GAZPROM). In general, such activities certainly benefit society, but also perform marketing functions for organizations (promotion, PR).

According to the reports, the companies have different degrees of involvement in volunteer projects. A low degree of involvement is often due to concentration on corporate social projects, the work of corporate charitable foundations.

** The size of the social benefits fund for employees – 265.63 $mln

*** Cumulative data from 2013– 18.37 $mln

**** Data on the corporation as a whole – 107 million Swiss francs

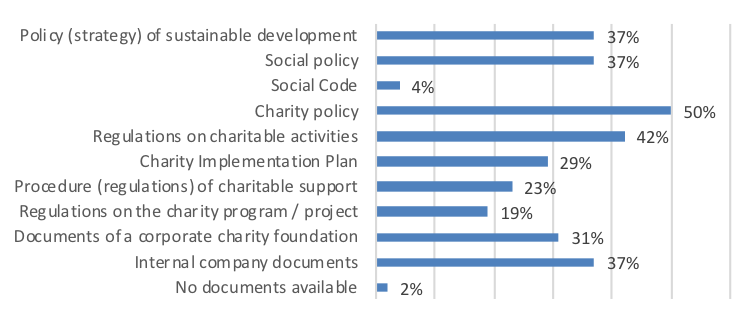

Documented consolidation of the strategy and policy of the charitable activities

The result of adopting a socially responsible approach in business is the adoption of an appropriate corporate culture and development strategy, support for charitable projects, and social entrepreneurship. All this requires a clear formulation and consolidation of values, goals and objectives of socially directed activities.

Figure

The sustainable development policy (strategy) as the document that most widely interprets the role of business in society and formulates the general goals of corporate social activity, as a rule, is present in divisions of large international companies.

Comparative assessment of motivation and goals of socially responsible activity

Distinctive features of the practice of Russian companies in the field of CSR can be identified for all major assessment criteria under consideration.

First, the majority of companies involved in CSR and publishing social reports are businesses with foreign capital or the state participation. The CSR activity in Russia is caused largely by ethical aspects but not corporate or strategic ones.

Second, the main stakeholders are regulators, foreign partners, local communities and consumers.

Third, the goals and directions of CSR efforts cover the formed range of issues related to solving social problems in education, culture, sports, social support of employees, while companies expect reciprocal involvement of the society. Differences in people's expectations should also be noted. Unlike the US and Europe, Russian society does not assign the function of solving social problems to business, sharing the power of the state and the opportunities of entrepreneurs.

Fourth, there is practically no assessment of CSR activities results in Russia. Companies are reluctant to share information about business goals and expectations.

Nevertheless, the expansion of corporate social programs, the increase in expenditures for CSR, the growth of publications on social and charitable projects of companies indicate an understanding of the importance of business participation in the life of society and the need to take into account its interests.

Conclusion

Russian business, on a par with the world one, is aware of the need to change its attitude to social needs of society and stakeholders. It accepts the rules of “corporate citizenship”, but is not sufficiently ready to shift to new values, to form a new corporate culture, to change business processes. The phenomenon of social entrepreneurship, which can be considered as a qualitatively new form of integration of social, production and market functions of business is understudied yet. The essential characteristics and the role of socially responsible marketing in changing the value basis of market interaction between counterparties are not defined (Bozhuk & Maslova, 2012; Inoue, Funk, & McDonald, 2017).

Particularly relevant is the issue of institutionalization of social responsibility of business. It is associated with the lack of clear rules and regulations governing the behavior of subjects within the framework of social-economic institution. This is confirmed by the results of Russian scientists’ studies (Dolgopyatova & Tomashuk, 2013; Blagov, Kabalina, Petrova-Savchenko, & Sobolev, 2015; Belousov, 2017).

An important direction in the research development can be the study of the prerequisites for the development of applied tools for CSR in managing of business sustainability and socially responsible marketing.

References

- Ackerman, R. (1975). The Social Challenge to Business. Cambridge, Massachusetts, London: Harvard University Press.

- Analytical statement. (2017a). The road ahead. The KPMG Survey of Corporate Responsibility Reporting (KPMG). Retrieved from https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf.

- Analytical statement. (2017b). The 2017 Deloitte millennial survey: Apprehensive millennials: Seeking stability and opportunities in an uncertain world (Deloitte Global). Retrieved from https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-deloitte-millennial-survey-2017-executive-summary.pdf.

- Analytical statement. (2018a). National Survey on Corporate Social Responsibility. Consumers, Professional Investors and CSR executives. Findings and executive summary (Aflac). Retrieved from https://www.aflac.com/docs/about-aflac/csr-survey-assets/2016-csr-survey-deck.pdf.

- Analytical statement. (2018b). The business case for inclusive growth: Deloitte Global’s inclusive growth survey report. (Deloitte Global). Retrieved from https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-abt-wef-business-case-inclusive-growth-global%20report.pdf.

- Analytical statement. (2018c). The rise of the social enterprise. 2018 Deloitte Global Human Capital Trends (Deloitte Global). Retrieved from https://www2.deloitte.com/content/dam/insights/us/articles/HCTrends2018/2018-HCtrends_Rise-of-the-social-enterprise.pdf .

- Armstrong, J., & Green, K. (2013). Effects of corporate social responsibility and irresponsibility policies. Journal of Business Research, Elsevier, 66(10), 1922-1927.

- Belousov, K. Yu. (2017). Sotsialnaya otvetstvennost biznesa kak faktor ustoychivogo razvitiya. Sankt Peterburg, SPb: Sankt-Peterburg State University.

- Blagov, Yu.E., Kabalina, V.I. Petrova-Savchenko A.A., & Sobolev I.S. (2015). Sozdaniye tsennosti dlya biznesa i obshchestva: analiz korporativnoy sotsialnoy deyatelnosti rossiyskikh kompaniy. Rossiyskiy zhurnal menedzhmenta, 2, 67-98.

- Boldyireva A. (2017). All about the leaders of 2017: based on the project "Leaders of corporate charity – 2017". Moscow: Donor Forum.

- Boulouta, I., & Pitelis, C.N. (2014). Who Needs CSR? The Impact of Corporate Social Responsibility on National Competitiveness. Journal of Business Ethics, 119, 49-364.

- Воwen, Н. (1953). Social Responsibilities of the Businessman. N. Y.: Наrper & Row.

- Bozhuk, S.G., & Maslova, T.D. (2012). Razvitiye instrumentariya sotsialno-otvetstvennogo marketinga. Problemy sovremennoy Ekonomiki, 1 (41), 199-203. [in. Rus.].

- Carroll, A. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48.

- Dolgopyatova, T.G., & Tomashuk, I.O. (2013). Upravleniye rossiyskimi predpriyatiyami s inostrannymi sobstvennikami: empiricheskiy analiz. Rossiyskiy Zhurnal Menedzhmenta, 11, 3-30. [in Rus.].

- Freeman, E. (1984). Strategic management: A stakeholder approach. Boston: Pitman

- Friedman, M. (1970). The Social Responsibility of Business is to Increase its Profits. The New York Times Magazine, 13, 17-21.

- Fu L., Boehe D., Orlitzky, M., & Swanson, D.L. (2018). Managing stakeholder pressures: Toward a typology of corporate social performance profiles. Long Range Planning, 8. 54-61.

- Inoue, Y., Funk, D.C., & McDonald, H. (2017). Predicting behavioral loyalty through corporate social responsibility: The mediating role of involvement and commitment. Journal of Business Research, 75, 46-56.

- Khairov, B.G., & Khametov D.G. (2014). Optimizatsiya vzaimodeystviya vlastnykh i predprinimatelskikh struktur v reshenii problem effektivnosti i sotsialnoy otvetstvennosti. Vestnik Samarskogo gosudarstvennogo ekonomicheskogo universiteta, 3(113), 6-12. [in Rus.].

- Kuratko, D.F., McMullen, J. S., Hornsby, J.S., & Jackson C. (2017). Is your organization conducive to the continuous creation of social value? Toward a social corporate entrepreneurship scale. Business Horizons, 60, 271-283.

- Levitt, T. (1958). The dangers of social responsibility. Harvard Business Review, 36(5), 41–50.

- Lim, J.S., & Greenwood, C.A. (2017). Communicating corporate social responsibility (CSR): Stakeholder responsiveness and engagement strategy to achieve CSR goals. Public Relations Review, 43, 768-776.

- Martínez, J.B., Fernández, M.L., & Fernández, M.R. (2016). Corporate social responsibility: Evolution through institutional and stakeholder perspectives. European Journal of Management and Business Economics, 25, 8-14.

- McCarthy S., Oliver B., & Song S. (2017). Corporate social responsibility and CEO confidence. Journal of Banking & Finance, 75, 280-291.

- Park, E., Joon, K.K., & Kwon, S.J. (2017). Corporate social responsibility as a determinant of consumer loyalty: An examination of ethical standard, satisfaction, and trust. Journal of Business Research, 76, 8-13.

- Phillips, R. (2003) Stakeholder legitimacy, Business Ethics Quarterly, 13(1), 25-41.

- Post, J. (2002). Redefining the Corporation: Stakeholder Management and Organizational Wealth, Stanford: Stanford University Press.

- Price, J.M., & Sun, W. (2017). Doing good and doing bad: The impact of corporate social responsibility and irresponsibility on firm performance. Journal of Business Research, 80, 82-97.

- Solke, H. (2014). Education, economic inequality and the promises of the social investment state. Socio-economic review. H. 2: special issue: The political economy of skills and inequality, Busemeyer; Torben Iversen, 12, 269-297.

- Swanson, D., & Orlitzky, M. (2017). Toward a conceptual integration of corporate social and financial performance. Handbook of integrated CSR communication, 8, 129-148.

- Wartick S., & Cochran P. (1985). The evolution of the corporate social performance model. Academy of Management Review, 10, 4. — Access:

- Windsor, D. (2001). The Future of Corporate Social Responsibility. The International Journal of Organizational Analysis, 9, 225-256. https://dx.doi.org/10.1108/eb028934.

- Wood, D. (1991). Corporate Social Performance Revisited. Academy of Management Review, 16(4), 691–718.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

20 March 2019

Article Doi

eBook ISBN

978-1-80296-056-3

Publisher

Future Academy

Volume

57

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1887

Subjects

Business, business ethics, social responsibility, innovation, ethical issues, scientific developments, technological developments

Cite this article as:

Agafonova, A., Yakhneeva, I., & Nikitina, I. (2019). Corporate Social Responsibility In Russia: Motives And Features. In V. Mantulenko (Ed.), Global Challenges and Prospects of the Modern Economic Development, vol 57. European Proceedings of Social and Behavioural Sciences (pp. 1055-1068). Future Academy. https://doi.org/10.15405/epsbs.2019.03.105