Islamic Work Ethics And Corporate Sustainability Performance: An Empirical Study

Abstract

Sustainability issue has been given great attention from many stakeholders which include Malaysian manufacturers. Manufacturing organizations face the sustainability issue which leads manufacturers to realize the importance of achieving corporate sustainability performance and various steps have been taken in achieving the organization sustainability performance. Islamic work ethics provide guidelines for employees in sustaining the organization in a sustainable manner while carrying out the manufacturing activities. Malaysian government has highlighted the importance for every individual to have good ethical values. The objective of this paper is to examine the effect of Islamic work ethics on corporate sustainability performance which comprises of economic, environmental and social sustainability performance. Questionnaires are distributed to the employees from middle to top level of management in chemical manufacturing organization. This study uses multistage sampling technique and the data is analysed using Partial Least Square (PLS) analysis. The findings indicate that there is a positive effect of Islamic work ethics on the three dimensions of corporate sustainability performance which are economic, environmental and social sustainability performance. This study contributes to the body of knowledge on sustainable manufacturing by investigating the effect of Islamic work ethics on corporate sustainability performance. This study will guide employees in achieving corporate sustainability performance by the implementation of Islamic work ethics in the work place.

Keywords: Islamic work ethicscorporate sustainability performancechemical manufacturing

Introduction

Throughout the world, there are many businesses that appear to be responding to the call of governments and societies to be economically, socially and environmentally responsible (Nooraslinda, Rohana, Safawi, Marziana & Wan, 2016; Mani, Gunasekaran, Papadopoulos, Hazen & Dubey, 2016; Muhammad, Zulkipli & Haseeb, 2016). In order to achieve corporate sustainability performance, Islamic work ethics must be practiced by the employees in the organization (Abbasi, Rehman & Bibi, 2011). Organization’s success is no longer measured by short-term profit maximization as Islamic work ethics is important in achieving corporate sustainability performance (Dina, Amr & Akrum, 2017; Nooraslinda et al., 2016). There are many researchers who agreed on the adoption of the Islamic work ethics in managerial, business operations and economic activities (Dina et al., 2017, Nooraslinda et al., 2016, Kalsom & Ahmad, 2014; Abdus, Kashif & Shakir, 2012). Islamic work ethics shown by organization contributed to the organizational success as it promotes well-being for society and creates wealth for stakeholders (Jalil, Azam & Rahman, 2010). Ethics are important in achieving sustainability as Malaysian government highlighted the importance of every individual to have good ethical values (Eleventh, Malaysia Plan, 2015). In order to do so, the government will enhance the involvement of all stakeholders in building a more ethical and moral society especially for religious institutions and community based (Eleventh Malaysia Plan, 2015). Hassan (2016) stated that Islamic approach is more agreeable with issues associated with sustainability and therefore businesses should have serious commitment to Islamic work ethics.

Islamic Work Ethics

The Islamic work ethics is rooted in the principle of Islamic Shariah and towards a work orientation (Dina et al., 2017; Mohamed, Siti & Nor, 2014). Since 1980s, ethics concept has been received many important attentions from researchers (Ali, 1988). The sayings and practices of the Prophet Muhammad (S.A.W) and Quran are the main sources of Islamic work ethics (Dina et al., 2017; Ali & Al-Owaihan, 2008). According to Salih, Zumrut and Ozkan (2012), Islam’s main religious text which guides mankind is known as Al-Quran, which is the last revelation to prophet Muhammad (S.A.W). While the oral tradition which related to Prophet Muhammad’s (S.A.W) deeds and words are known as hadith (Abdus et al., 2012). The good values in feeling, thinking, behaviour or action are from the perspective of Islamic ethics (Hayaati, 2007). Most of the researchers argued that in Islamic work ethics, work is a desirability quality in the person‘s need and is an obligatory activity in creating strength of social and individual life (Ali &Al Owaihan, 2008). As stated by Nooraslinda et al. (2016), in doing business, acting ethically is essential in Islam which involved all the morally correct factors including production, business processes and an organization‘s behaviour with its customers and the communities in which it operates.

Jalil et al. (2010) stated that Islamic work ethics strengthens the qualities such as trust, loyalty, honesty, flexibility and solidarity. Besides, a number of good behaviours are gained by executing Islamic work ethics like hard work, dedication to work, fair compositeness in the workplace, commitment and cooperation (Kumar & Rose, 2010). Some of the Islamic values which have been stated in the traditions of Prophet are timeliness, cooperation, piety, cleanliness, transparency, honesty, capability, competence, benevolence, trustworthiness, accountability, responsibility, promise-keeping, fairness, perfectionism, punctuality and consultation (Kalsom & Ahmad, 2014). Hafiz, Shakir, Mushtaq and Yasir (2015) stated that in every aspect of life, a sound and complete ethical system is provided by Islam. As stated by Hafiz et al. (2015), Islam explicitly eliminating unfairness, misuse, inequity and oppression.

Corporate Sustainability Performance

There is no common definition of corporate sustainability (Koc & Durmaz, 2015). Corporate sustainability refers to a dynamic state that arises when the organization develops continuous shareholders and stakeholders‘value which maintains the well-being of the economy, environment and society for a long-term goal (Mohammad, Rahimi, Norani & Rushami, 2016; Hassini et al., 2012). Corporate sustainability is being describes as conducting operations in a manner that meets existing needs, without comprising the ability of future generations to meet their needs and has regard to the impacts that the business operations have on the life of the community in which it operates (Hart & Milstein, 2013). According to Koc and Durmaz (2015), corporate sustainability is essential in achieving organization‘s vision without losing competitive advantage while ensuring company’s economic growth, environmental stewardship and providing social responsibilities without contradicting from its mission and goals. The components of corporate sustainability performance are the triple bottom lines which are economic sustainability performance, environment sustainability performance and social sustainability performance (Gomes, Kneipp, Kruglianskas, Rosa & Bichueti, 2015).

Problem Statement

Manufacturing sector is an important sector to Malaysia as it contributes to the gross domestic product of the Malaysian economy (Adebambo, Abdulkadir, Mat, Alkafaagi & Kanaan, 2013; Mohammad et al., 2016). However, Malaysian manufacturing sector face the sustainability issue in terms of environment, economy and social sustainability (Mohammad et al., 2016). The impact of global warming, natural disasters, wars and environmental problems made a sustainable business in manufacturing a crucial issue (Gunasekaran & Spalanzani, 2012). Nowadays, the limitation of natural resources, environmental problem, and waste management issues challenge the manufacturing sector to stick to strict environmental regulations (Ghazilla et al., 2015). It also shows that the environmental problems brought by industry or individual organization resulted in the negative effects towards society and environment (Mohammad et al., 2016).

Manufacturing operations in Malaysia do not only give huge implications to the environment but also to the workers which affects the social sustainability. According to Maliza (2012), industrialization which caused “sinister killers” that contains of poisonous chemicals, dust, extreme heat, gases, noise and vibrations that are slow and occasionally unrecognizable are the cause of 300 to 400 of 200,000 Malaysian industrial workers are reported deaths and another 13,000 are disabled every year. This is supported by the Department of Safety and Health (DOSH) which stated that the highest number of occupational accidents occurred in manufacturing sector (DOSH, 2016). Table

Besides that, there is a lack of studies which consider the triple bottom line dimensions (social, environmental and economic) simultaneously of sustainability performance (Muhammad et al., 2017; Mani et al., 2016). Hence, this study is important as it focuses on all dimensions of corporate sustainability performance as most of previous studies focus on the three dimensions separately (Muhammad et al., 2017). Employees in important sector like manufacturing sector has to take serious action in achieving corporate sustainability performance by focusing on the three dimensions of corporate sustainability performance.

Further research on the Islamic work ethics need to be done in developing countries as there are few studies in this area (Ahmad, 2011; Rokhman, 2010; Kumar & Rose, 2010). It is important to understand the possible linkages of ethics towards sustainable performance but however, the research of Islamic work ethics on the performance of corporate sustainability has been seen to be limited (Nooraslinda et al., 2016; Salih et al.,2012). The literature on ethics and sustainability mainly focused on public listed organization in the context of developing countries like Malaysia (Nooraslinda et al., 2016) and thus the study on manufacturing organizations are lacking. As there is limited study of Islamic work ethics in developing countries, it constitutes the foundation to study the effects of Islamic work ethics on corporate sustainability performance in manufacturing organizations.

Research Questions

The research questions are as below:

What is the effect of Islamic work ethics on economic sustainability performance?

What is the effect of Islamic work ethics on environmental sustainability performance?

What is the effect of Islamic work ethics on social sustainability performance?

Purpose of the Study

The objective of this paper is to examine the effects of Islamic work ethics on corporate sustainability performance which comprises of economic, environment and social sustainability performance.

Research Methods

Chemical manufacturing industry has been chosen in this study due to the high sustainability issues occurred in this industry (Ta, Meng, Mokhtar, Ern, Alam, Sultan & Ali, 2016). Employees from middle to top level management have been selected as the sample. This study is a pilot study of the actual survey in examining the effects of Islamic work ethics on corporate sustainability performance. Fifty questionnaires were distributed to the employees in 14 chemical manufacturing organizations which were listed in Federation of Malaysia Manufacturing. In order to guarantee the content validity of the measurement in this study, discussions have been done with the experts in the field and employees from the chemical manufacturing industry. This study used multistage sampling technique and the data was analysed using partial least square (PLS) analysis. The proposed hypotheses are as below:

H1:There is a significant effect of Islamic work ethics on economic sustainability performance.

H2: There is a significant effect of Islamic work ethics on environmental sustainability performance.

H3: There is a significant effect of Islamic work ethics on social sustainability performance.

Findings

This study analyzed 50 respondents which 32% respondents are male and 68% respondents are female. The highest percentage for races is Malay which is 56%, while Chinese is 34%, Indian is 8% and other races are 2%. Most of the workers age are ranging from 31 to 40 (42%) and the least is 51 and above (8%). Most of the workers have working experience less than 5 years (48%) and the least is more than 21 years (10%). For education level, the highest percentage is Bachelor’s Degree (52%).The respondents consist of 28% from general manager or manager and others are executives.

Reliability

Composite reliability is used to measure the internal consistency. As stated by Bagozzi and Yi (1988), composite reliability should be higher than 0.7. Table

Convergent Validity

The suggested loadings values for all items are 0.7 or higher (Fornell & Larcker, 1981; Salwa et al., 2017). Therefore for this study, 14 items from 50 items were deleted due to low loading below 0.7. The loading value is ranging from 0.711 to 0.917. According to Bagozzi and Yi (1988) average variance extracted (AVE) should be 0.5 or higher. From Table

Discriminant validity

The discriminant validity is assessed through the Fornell-Larcker criterion which is shown in Table

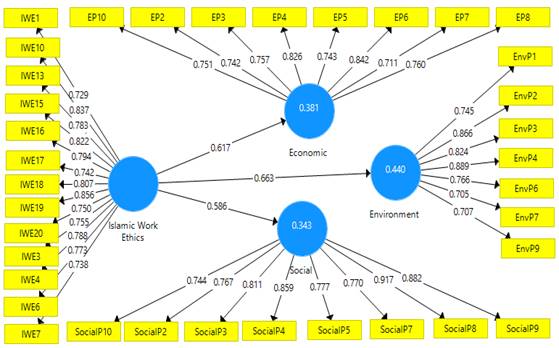

Structural Model

Figure

The result in table

Conclusion

In recent years, sustainability in manufacturing has received great attention. There are many researchers who agree on the adoption of Islamic work ethics in sustaining the organization. This is supported by Nooraslinda et al. (2016) and Dina et al. (2017) which stated that in today‘s challenging world, success is no longer measured by short-term profit maximization as to be seen as sustainable, Islamic work ethics must be integrated into decision making and strategy in achieving sustainability. Islamic work ethics must be inculcated in culture of the organization in order to achieve sustainable business performance as it is the global economic crisis remedy (Nooraslinda et al., 2016; Abdus et al., 2012). People who are practicing Islamic work ethics in the organizations are also tend to be more responsible and attached for the success of the organization (Salih et al., 2012). The objective of this paper is achieved by investigating the effect of Islamic work ethics on corporate sustainability performance. The result shows that Islamic work ethics has positive effects on the three dimensions of corporate sustainability performance which are economic, environment and social sustainability performance in chemical manufacturing organization. The findings of this study contributed to the body of knowledge of Islamic work ethics and corporate sustainability performance in a developing country, which may be different in developed countries. The findings also can be used as a guideline by manufacturers and policymakers who consider the importance of achieving corporate sustainability performance.

Acknowledgments

This research wishes to acknowledge the Ministry of Education (MOE) for the fund granted through the Fundamental Research Grant Scheme (FRGS), under grant number FRGS/1/2016/SS03/UNITEN/01/1.

References

- Abbasi, A. S., Rehman, K., & Bibi, A. (2011). Islamic work ethics: How it affects business performance. Actual Problems of Economics. Retrieved April 15, 2016, from http://ssrn.com/abstract=1992008.

- Abdus, S. A., Kashif, U. R. & Shakir, H. A. (2012). Islamic work ethics: How they affect shareholder value. Science International (Lahore), 24(4), 521–530.

- Adebambo, H. O., Abdulkadir, R. I., Mat, N. K. N., & jihad Alkafaagi, A. A. (2013). Drivers of sustainable environmental manufacturing practices and financial performance among food and beverages companies in Malaysia. American Journal of Economics, 3(2), 127-131.

- Ahmad, M. S. (2011). Work ethics: An Islamic prospective. International Journal of Human Sciences, 8, 850–859.

- Ali, A. J. & Al-Owaihan, A. (2008). Islamic work ethic: A critical review. Cross Cultural Management: An International Journal, 15(1), 5.

- Bagozzi, R. P., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the academy of marketing science, 16(1), 74-94.

- Department of Safety and Health (DOSH) (2016). Occupational accidents statistics by sector. Retrieved May 20, 2016, from http://www.dosh.gov.my/index.php/en/list-of-documents/statistics/occupational-accident-2016/2342-occupational-accidents-statistics-by-sector-until-august-2016/file.

- Dina, M. A., Amr, K., & Akrum, H. (2017). Eco-Islam: Beyond the principles off why and what, and into the principle of how. J Bus Ethics.

- Eleventh Malaysia Plan (2015). Pursuing green growth for sustainability and resilience. Retrieved March, 14, 2016, from http://rmk11.epu.gov.my/book/eng/Elevent-Malaysia-Plan/RMKe11%20Book.pdf.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of marketing research, 39-50.

- Ghazilla, R. A. R., Sakundarini, N., Abdul-Rashid, S. H., Ayub, N. S., Olugu, E. U., & Musa, S. N. (2015). Drivers and barriers analysis for green manufacturing practices in Malaysian SMEs: A preliminary findings. Procedia CIRP, 26, 658-663.

- Gomes, C. M., Kneipp, J. M., Kruglianskas, I., da Rosa, L. A. B., & Bichueti, R. S. (2015). Management for sustainability: An analysis of the key practices according to the business size. Ecological Indicators, 52, 116-127.

- Gunasekaran, A., & Spalanzani, A. (2012). Sustainability of manufacturing and services: Investigations for research and applications. International Journal of Production Economics, 140(1), 35–47.

- Hafiz, M. F. Z., Shakir, U. K., Mushtaq, A., Yasir, M., R. (2015).Islamic Values and Ethical System Towards Business : Does Islam Provide Best Framework To the Corporate World?, International Journal of Economics, Commerce and Management (2), 1–10.

- Hart, S. L., & Milstein, M. B. (2013). Creating sustainable value. RAE-executivo Acad. Manag. Exec. 17 (2), 56-69.

- Hassan, A. (2016). Islamic ethical responsibilities for business and sustainable development. Humanomics, 32(1), 80-94.

- Hassini, E., Surti, C., & Searcy, C. (2012). A literature review and a case study of sustainable supply chains with a focus on metrics. Int. J. Prod. Econ. 140 (1), 69-82.

- Hayaati, S. I. (2007). Values and ethics towards quality public delivery system of malaysia: An Islamic perspective. Journal Syariah, 15 (2), 25-43.

- Jalil, A., Azam, F. & Rahman, M. K. (2010). Implementation mechanism of ethics in business organizations. International business research, 3(4), 45-151.

- Kalsom, A. W. & Ahmad, R. (2014). Measuring small firm entrepreneur performance based on al-falah. World Applied Sciences Journal, 29(12), 1532–1539.

- Koc, S., & Durmaz, V. (2015). Future oriented corporate leadership model. Journal of Global Strategic Management, 9 (1), 55-64.

- Kumar, N., & Rose, R. C. (2010). Examining the link between Islamic work ethic and innovation capability. Journal of Management Development, 29(1), 79-93.

- Maliza, D. K. Z. (2012). The environmental ethical commitment (eec) of the business corporations in Malaysia. Social and Behavioral Sciences, 36, 565–572.

- Mani, V., Gunasekaran, A., Papadopoulos, T., Hazen, B., & Dubey, R. (2016). Supply chain social sustainability for developing nations: Evidence from India. Resources, Conservation and Recycling, 111, 42-52.

- Mohamed, F. A., Siti, F. W., & Nor, Z. M. R. (2014). The impact of Islamic work ethics on job performance and organizational commitment. Proceedings of 5th Asia-Pacific Business Research Conference, 17 – 18.

- Mohammad, G. H., Rahimi, A., Norani, N. & Rushami,Z. Y. (2016). GSCM practices and sustainable performance: A preliminary insight. Journal of Advanced Management Science.

- Muhammad, Z., Zulkipli, G., & Haseeb, U. R. (2017). Sustainable Education: A Buzzword of Universiti Teknologi PETRONAS, Malaysia. In Managerial Strategies and Solutions for Business Success in Asia (255-279). IGI Global.

- Nooraslinda, A. A., Rohana, A., Safawi, A. R. Marziana, M. M. & Wan, C. & Yusof W. M. (2016). Ethical codes as instruments for cooperative sustainability. Social and Management Research Journal, 13(1), 30-43.

- Rokhman, W. (2010). The effect of Islamic work ethics on work outcomes. Electronic Journal of Business Ethics and Organization Studies, 15(1), 21–27.

- Salih, Y., Zumrut, H. S., & Ozkan, D. (2012). An investigation into the implications of Islamic work ethic (Iwe) in the workplace. Journal of Economics and Behavioral Studies, 4(11), 612–624.

- Ta, G. C., Meng, C. K., Mokhtar, M., Ern, L. K., Alam, L., Sultan, M. M. A., & Ali, N. L. (2016). Enhancing the regulatory framework for upstream chemicals management in Malaysia: Some proposals from an academic perspective. Journal of Chemical Health and Safety, 23(3), 12-18.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

31 July 2018

Article Doi

eBook ISBN

978-1-80296-043-3

Publisher

Future Academy

Volume

44

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-989

Subjects

Business, innovation, sustainability, environment, green business, environmental issues, industry, industrial studies

Cite this article as:

Asha’ari, M. J., & Daud, S. (2018). Islamic Work Ethics And Corporate Sustainability Performance: An Empirical Study. In N. Nadiah Ahmad, N. Raida Abd Rahman, E. Esa, F. Hanim Abdul Rauf, & W. Farhah (Eds.), Interdisciplinary Sustainability Perspectives: Engaging Enviromental, Cultural, Economic and Social Concerns, vol 44. European Proceedings of Social and Behavioural Sciences (pp. 392-400). Future Academy. https://doi.org/10.15405/epsbs.2018.07.02.42