Study On Young External Public Auditor

Abstract

The idea of this study came as a consequence of the Romanian Court of Accounts' participation to the second YES EUROSAI Conference for young external public auditors from the supreme audit institutions member of EUROSAI, held in 2015 in Jerusalem (http://reg.co.il/yes2/index.ehtml). The context in which this study was conducted is defined by the situation that will face the supreme audit institution of Romania (the Romanian Court of Accounts) in the near future, given the large number of retirements among specialized personnel (external public auditors). The study is based on quantitative research method of questionnaire, considering that this method highlights best the objectives proposed in shaping the young external public auditor' profile. The questionnaire contains 27 questions, classified in 3 sections and was filled by a representative sample of 48% of the total number of participants to the EUROSAI YES Conference. The results of this study can be used not only by the Romanian Court of Accounts but also by other supreme audit institutions when recruiting new young personnel, taking into account that are highlighted the main characteristics, needs and expectations that young people under 35 years have when opting for a career in a supreme audit institution.

Keywords: Supreme audit institutionsperformancemotivatoryoung auditorspublic sector

Introduction

The ability to attract and motivate young people trained in public sector auditing will be a key element that will influence the future institutional development, human resources being essential from the point of view of performing a quality activity in the Supreme Audit Institutions (SAI, Supreme Audit Institution).

Also, to ensure an efficient management of human resources in this field, the decision makers of Supreme Audit Institutions must take into account a number of sociological factors, specific to the generation of young people aged under 35. The young people under 35, namely the current generation of young people born in the 80s, is significantly different from other generations, having a number of specific characteristics: they want to be clearly distinguished from other individuals, want stand out, they have self-confidence (http://www.generationy.com/about-generation-y-in-the-workforce/characteristics/), are very attracted to new technologies (https://en.oxforddictionaries.com/) and are constantly focusing on personal development.

For adapting to the present realities, the heads of the supreme audit institutions must take into account of these features for an efficient management of future human resources composed of young people.

Problem Statement

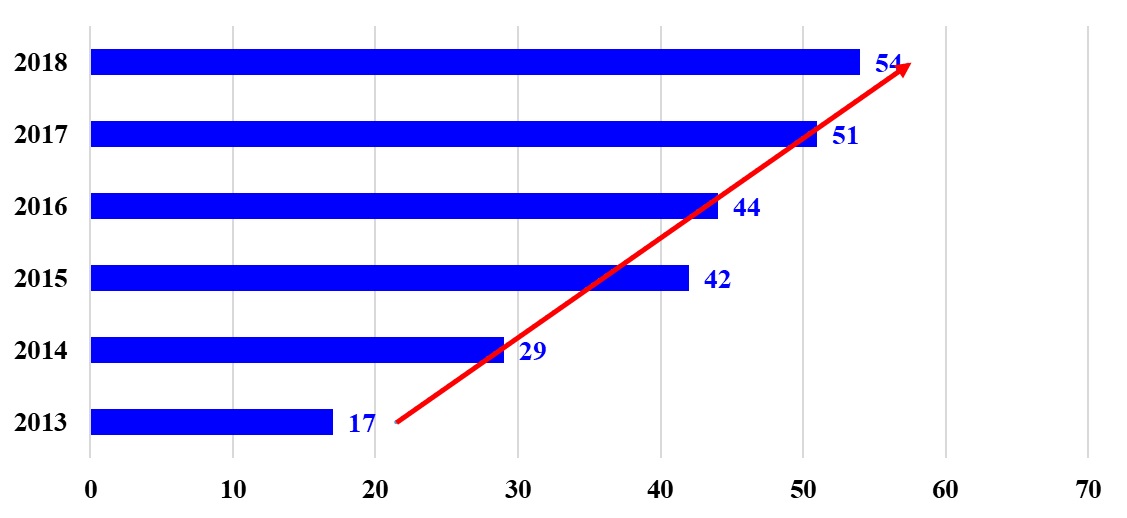

The idea of the study came as a consequence of the situation that the Romanian Court of Accounts will face in the near future, namely the upward trend in the number of pensioners, shown in the chart below (Curtea de Conturi, 2015, p. 55):

The large number of retirements reflected in the chart above can be a real problem that the Romanian Court of Accounts will face during the period mentioned, namely 2013-2018. In order to see what factors may influence young people to pursue a career in public external audit or lead them to remain in the supreme audit institutions, I considered useful to undertake a study reflecting the main factors mentioned above.

In order to identify the factors mentioned above, I established two working hypotheses that will be tested in the study:

H1: Professional development is a key element in retaining young external public auditors in the SAIs.

H2: The financial factor regarding the rewarding of performance is the most effective for young external public auditors.

The results of this study can be used by all Supreme Audit Institutions, given the sample used, comprising young auditors from the SAIs members of EUROSAI.

Research Questions

Through the questionnaire drawn up, I tried to answer a series of questions such as:

3.1. To what extent the supreme audit institutions fail to attract, motivate and retain young people with real qualities and skills for public sector auditing?

3.2. What are the main motivational factors of the young generation of external public auditors?

Purpose of the Study

The aim of this study is to identify those factors that highlight the needs, characteristics, aspirations and expectations of young people aged under 35 when opting for a career in the supreme audit institutions.

Research Methods

The methodology used to conduct this study was based on the quantitative method (Shaughnessy, Zechmeister, & Jeanne, 2011, pp. 161–175), and the instrument used was a questionnaire comprising 27 questions which have been classified into 3 sections:

The research was conducted on a sample of 35 people (48% of the total number of elements of the population), which I consider is representative. The 35 people were 20 women and 15 men. The questionnaire was distributed in paper format during the Conference, being returned by respondents to the delegation of the Romanian Court of Accounts.

The data collected were processed through the Excel Office programme and SPSS for validity and verifying the working hypotheses. Then, the results were analysed and interpreted by the author.

The research limitations consist in the fact that this questionnaire was sent to the external public auditors under 35 who are part of the SAIs members of EUROSAI (European Organisation of Supreme Audit Institutions), other regional groups of INTOSAI not being included in the sample, the Conference following which the data were collected being organized only for SAIs members of EUROSAI.

Findings

From all 27 questions addressed, I selected the most relevant of them in order to emphasize those features, needs and expectations that young people have when are choosing to pursue a career in public external audit.

After analyzing the answers given by respondents to question 3

The question 5

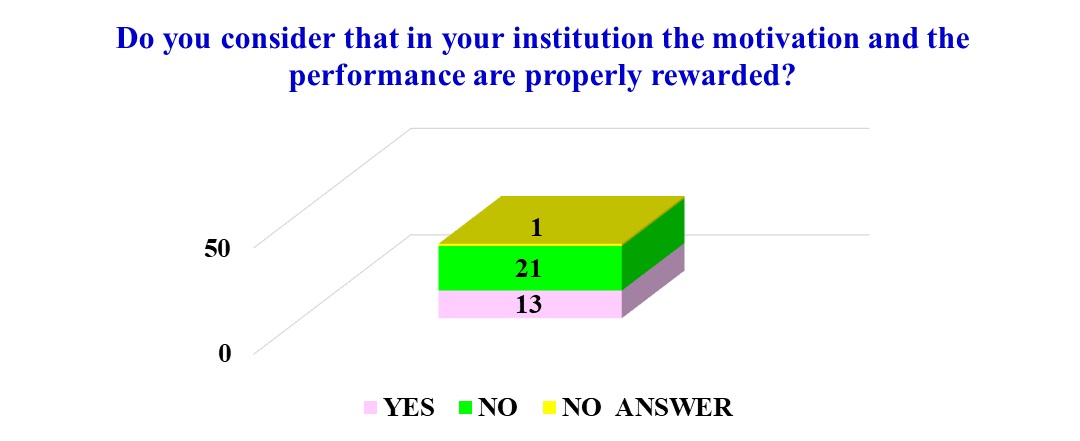

According to the answers provided, 60% of young auditors consider that they are not properly motivated within their supreme audit institutions, that their performance is not rewarded according to their expectations, although all respondents believe that they perform their tasks according to the job descriptions, furthermore, 49 % answered that they are always available for work.

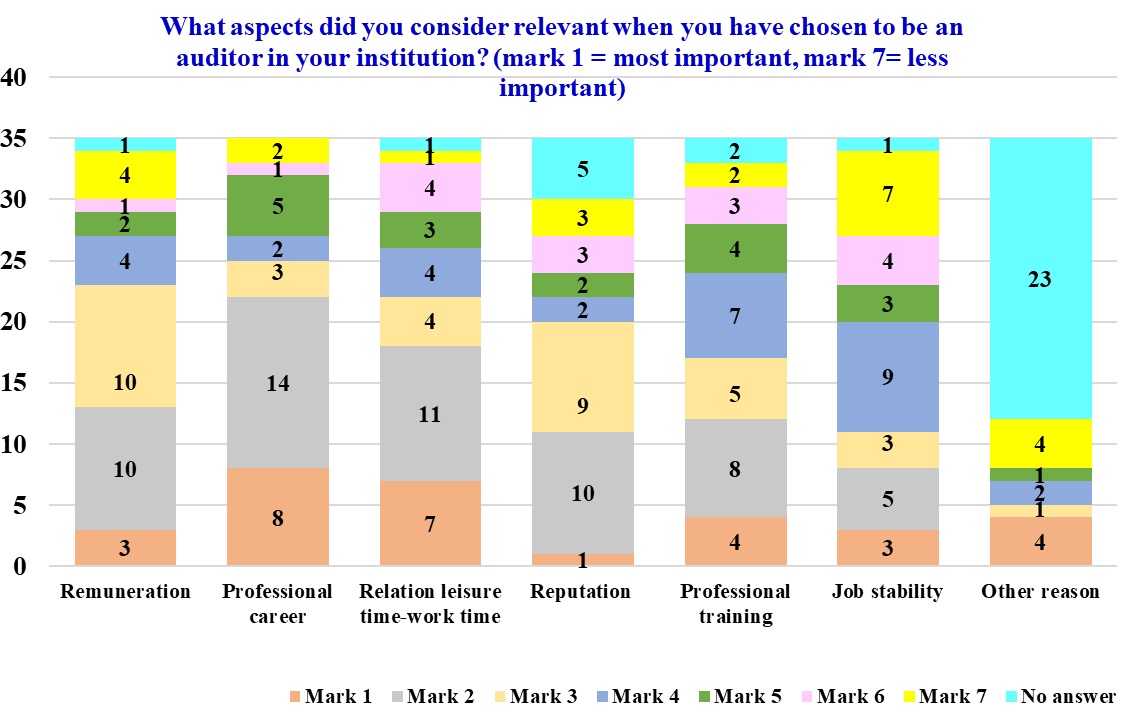

Next, I analyzed the relevant factors for young people when they opted for a position of external public auditor within their institution.

According to the chart above, the relevant factors for young people when they opted for a position of external public auditor in their supreme audit institution after analyzing the replies given to the question "What aspects did you consider relevant when you have chosen to be an auditor in your institution? (mark 1 = the most important, mark 7= the less important)" are the following:

The respondents considered

Thus, in the context in which young people belonging to

Taking into account that, in our country, the remuneration of personnel performing specific activities of the Romanian Court of Accounts (external public auditors) and of the support personnel is very strictly stipulated, the salary bonuses not being covered in the current legislation, the remuneration remains a decisive factor in attracting and retaining young generation of auditors.

The balance between work and personal life refers to the combination of work and personal life so that both can be met successfully. Getting this balance is benefic both to the health and wellness of employees, as well as for the organization's performance (improved employee retention rate, quality of work, etc.).

The balance between work and personal life was considered

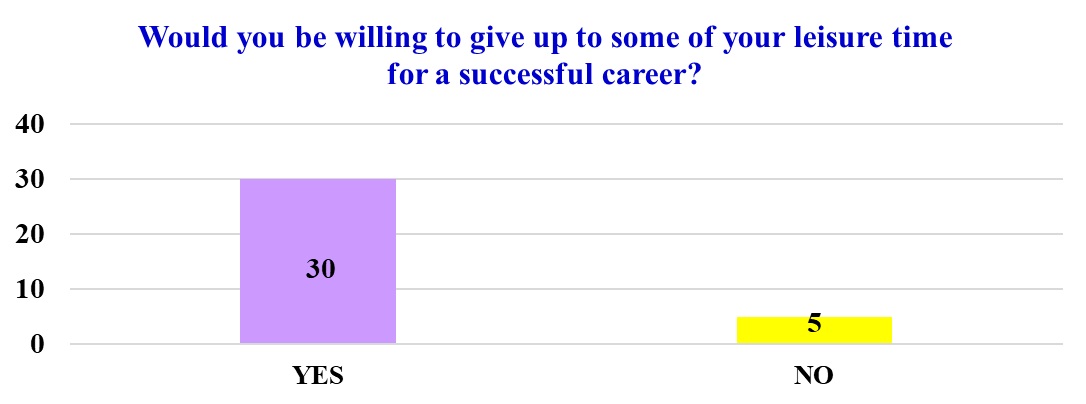

Moreover, 89% of respondents considered important and relevant the relationship between time spent at work and leisure time remaining. However, the career remains very important for young auditors participating in this study as respondents, according to the answers they provide, 86% of them saying that they would be willing to give up some free time for a successful carreer.

Based on the responses to questions, it can be concluded that the generation of young auditors expect a more diversified range of benefits that derive from or are related to work, one of them being considered and remained the free time available to them or extra-professional activities.

The supreme audit institution should recognize the special impact that the reputation has on society in general, and must identify the elements, peculiarities that may be useful in attracting, motivating and keeping young auditors among these institutions.

Also, by the answers to the questions was aimed to highlight the motivational factors considered relevant by young people to remain in the organization and continuing the external public audit activity within their supreme audit institutions.

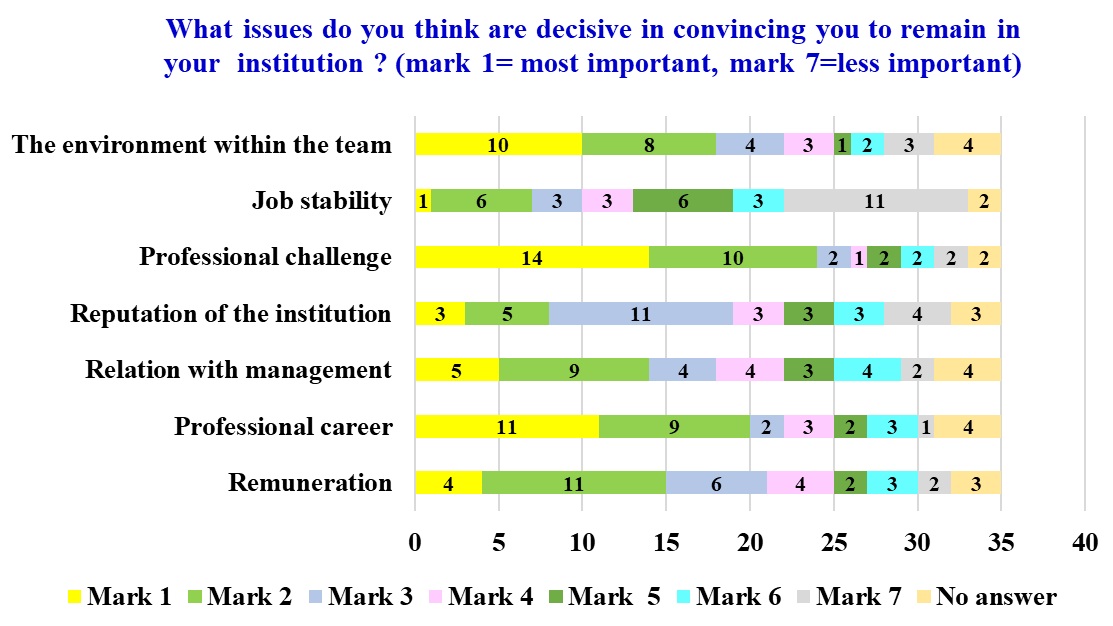

Next, I analyzed the responses to the question "What issues do you think are decisive in convincing you to remain in your institution? (mark 1 = the most important, mark 7 = the less important)"?. Not surprisingly, the remuneration is considered as the most important decision factor for keeping young people in the supreme audit institution, this being characteristic, in fact, to the Generation Y in general.

The ability of the organizations to provide professional challenges, as a part of professional development, is considered the most important factor for keeping young people in the supreme audit institutions.

The atmosphere within the group is also considered a decisive motivator. A pleasant atmosphere within the organization determinesthe employees to work with pleasure, which leads to an increased efficiency and quality of work. But the atmosphere is closely linked to the auditor-management relationship and merit recognition.

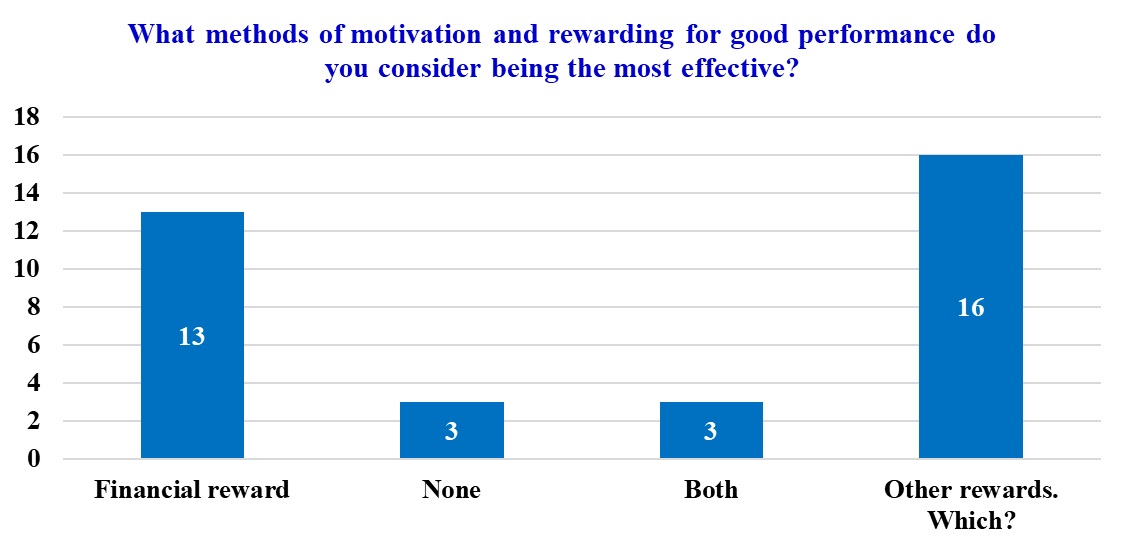

Regarding other forms of reward, the respondents indicated that these may be: awards, career, challenges, recognition from superiors, professional development, obtaining positive feedback from superiors, participation in international conferences, sessions, providing leadership positions, sense of professional fulfillment, creativity, training, control of own work, good atmosphere at work, freedom in choosing audit topics, participation in international missions.

According to the responses obtained through the application of questionnaires, in respondents' opinion the non-financial motivations are at least as effective as salary bonuses or other consideration, when aiming to build a long term relationship with the employees.

Besides the material advantages, consisting of salary bonuses, the young auditors need security, they need to be offered a sense of belonging to a group, which can be ensured by creating a good working environment, a good atmosphere at work.

In young external public auditors' opinion, a form of rewarding performance, expected and desired by them, can be the very positive feedback from superiors, recognition by these of young auditors merits.

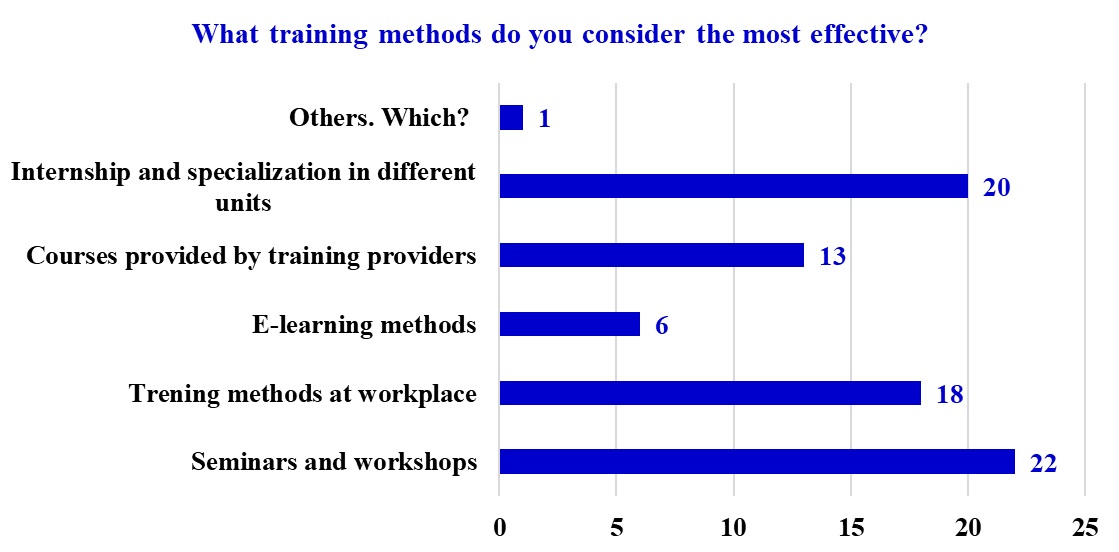

Regarding training methods, the respondents indicated that the most efficient in their view are seminars and workshops, butalso training courses organized in other units. Also, the methods of traning at workplace were considered useful.

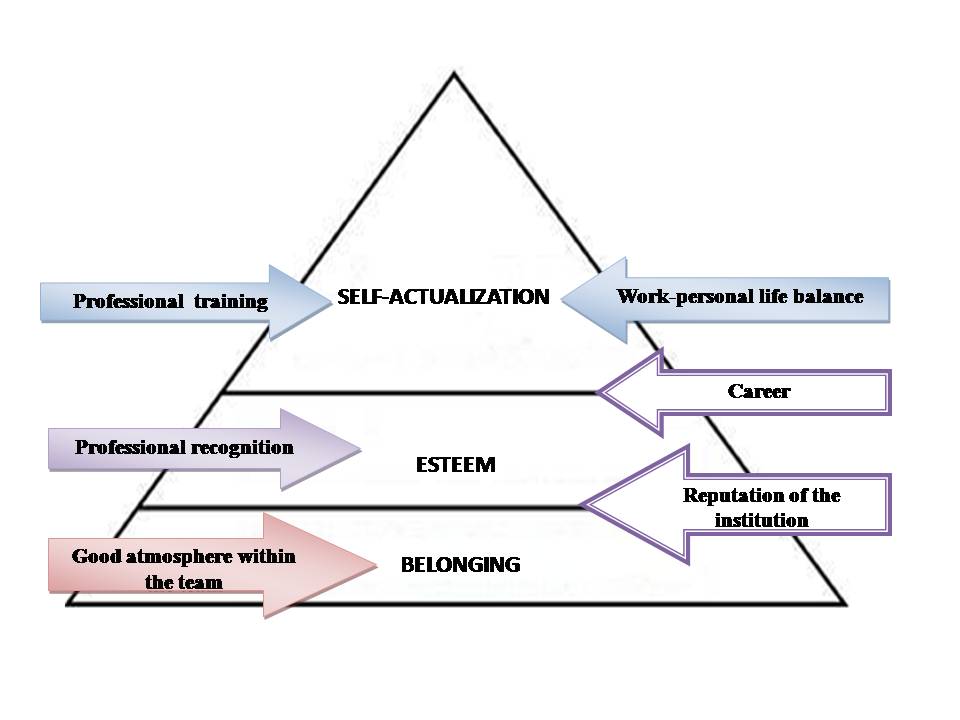

After analyzing the data presented in this study, it can be achieved a pyramid of needs of young external public auditors, after Maslow model, but eliminating the first two levels, namely physiological needs and security needs, which are found to all human (Maslow, A. H. (1943), p. 370-385).

Following the analysis of the responses to the questionnaire, a pyramid of needs of young external public auditors can be represented as follows:

If we look at this pyramid, we see that some of the issues outlined above in our study can meet not only at one level, but in two of the three levels of the pyramid. Therefore, the reputation of the supreme audit institution satisfies the need of belonging to the individual but also the need regarding the esteem and the auditor's professional career can satisfy both the need for esteem and the sense of self-actualization. Also was noted, based on this analysis, that not always the financial factor is the most important motivator, but also the non-financial factors.

The employees can be motivated in different non-financial ways and the employers must adjust their rewards to the labour force. Because it can be difficult to choose the best non-financial ways of motivation, staff consultation about the rewards they would like to receive is an option.

Conclusion

By the questions addressed in this study, I tested two hypotheses presented in its debut, namely:

H1: Professional development is a key element in retaining young external public auditors in the SAIs.

H2: The financial factor regarding the rewarding of performance is the most effective for young external public auditors

Regarding the first working hypothesis, after analysing the responses, I found that it is true, the respondents to the questionnaire mentioning the professional development as the main factor that lead the young public external auditors to remain within the SAI, 40% of them considering the professional development very important, and approx. 30% important.

Regarding the second working hypothesis, it is not true, since the responses showed that the external public auditors appreciate more other ways to reward their performance than the financial ones. Thus, 46% said that non-financial rewards (awards, participation in international conferences, professional development opportunities, recognition from superiors, etc.) are more important than financial rewards. This is true even in light of Generation Y, which focuses more on personal development, on the ability to choose for themselves the benefits it will have, on creativity etc.

The findings of this study reflect once again the features of Generation Y: remuneration is not regarded as the most important decision factor for maintaining young external public auditors in supreme audit institutions, the career remains very important for them, professional training, the control over their activities, all these the characteristic being, in fact, characteristic to the Generation Y, in general.

In order to ensure an effective management of human resources within the supreme audit institutions in the context of the new generation, their managers must take into account these factors and also the specific factors of Generation Y, both in terms of recruiting and maintaining this young generation within the supreme audit institutions.

References

- Curtea de conturi. (2015). Raportul de activitate al Curții de Conturi pe anul 2015.

- http://reg.co.il/yes2/index.ehtml

- http://www.generationy.com/about-generation-y-in-the-workforce/characteristics/

- https://en.oxforddictionaries.com/

- Maslow, A. H. (1943). A theory of human motivation. Psychological review, 50 (4), p. 370-385.

- Shaughnessy, J., Zechmeister, E., Jeanne, Z. (2011). Research methods in psychology (9th ed.). New York: McGraw Hill.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

30 July 2017

Article Doi

eBook ISBN

978-1-80296-026-6

Publisher

Future Academy

Volume

27

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-893

Subjects

Teacher training, teaching, teaching skills, teaching techniques,moral purpose of education, social purpose of education, counselling psychology

Cite this article as:

Pleșa, I. T. (2017). Study On Young External Public Auditor. In A. Sandu, T. Ciulei, & A. Frunza (Eds.), Multidimensional Education and Professional Development: Ethical Values, vol 27. European Proceedings of Social and Behavioural Sciences (pp. 629-638). Future Academy. https://doi.org/10.15405/epsbs.2017.07.03.74