Environmental Management Accounting Practices: A Review of the Literature

Abstract

The objectives of this research is to carry out a systematic search strategy to review literature that addresses ‘What drives environmental management accounting practices in businesses?’ and to present findings of environmental management accounting practices based on industry. The search strategy was conducted on published literature from 2015 up to 2020 that fulfils specific criteria such as articles must be in the English Language, for example. The final literature ready for review was 72 articles out of 750 papers identified. The articles were analysed for emerging themes. The themes derived were industry, tools applied, drivers and barriers to implementation. As environmental management accounting practices are not mandatory or regulated, companies are free to implement or disregard. Most of the literature were based on manufacturing industry, agriculture and hospitality. Material flow cost accounting was found to be the most recorded tool applied. Drivers and barriers to environmental management accounting implementation were also identified.

Keywords: Environmental, management, accounting, practice, implementation

Introduction

Conventionally, management accounting information gathered for decision-making is for the sole benefit of the decision maker and used internally. It would have excluded information on impacts these decisions will have on stakeholders. Environmental management accounting (EMA) framework will be able to aid decision makers to have on hand relevant information on environmental activities that is material to both the organisation and the stakeholders. This is because a company may appear to be environmentally committed on paper while in fact the company is a poor environmental performer as evident in a research by Mohd Khalid et al. (2012). Thus, it is imperative to build companies that are environmentally responsible and sustainable. Burritt et al. (2002) also asserted that conventional management accounting does not process and incorporate environmental activities for decision-making purposes. Consequently, there is a need for companies to take into consideration the environmental monetary and physical information.

It is argued that sustainable practices may be adapted in companies when awareness and best practices are introduced at the initial stage in a business. For example, it was discovered the agricultural practices introduced by corporate farm extension workers to small scale farmers about good agricultural practices were able to help them increase their income through improved resource efficiency (water, fertiliser, energy) and reduce greenhouse gas emissions. Corporate farm extension workers are essentially government workers who provide technical assistance in best farming practices. The finding infers that government agencies pro-activeness in disseminating awareness and knowledge is key in building awareness and transferring knowledge on sustainable practices (such as EMA) in order for corporate players to embrace and implement it companywide.

Burritt et al. (2019) who conducted a systematic review of EMA for cleaner production based on Schaltegger et al. (2013) and Tsui (2014) iterate that these literature reviews provide evidence that an exploration into how EMA exists in organisations is needed. They commented that EMA for cleaner production will not be achieved by implementing a single EMA application such as material flow cost accounting, but requires a combination of applications.

Therefore, this research aims to conduct a systematic search strategy to uncover themes from the literature that explain how EMA is implemented in companies and discover the drivers and barriers of EMA implementation.

Method

I conducted a systematic search strategy (SSS) to get a good coverage of current literature on EMA. The SSS process focused on two main research questions, namely: i) How are EMA practices implemented in companies? ii) What are the drivers and barriers of EMA implementation? An analysis of articles from 2015 to 2020 was very helpful in providing information for the research objectives, research population and sample, themes, methodology, theories underpinning the research as well as results. The search strategy is performed through the identification, screening and eligibility steps to ensure rigorous and systematic searching.

Identification process

The identification process refers to searching specific terms, synonyms and variation for the main keywords of the research questions. Each question goes through rigorous screening process. A researcher is required to generate a list of possible keywords based on RQ1 and RQ2 in order to grow options for selected databases and finding specific articles to review. These keywords were generated via Thesaurus.com, other keywords used in the literature, keywords suggested by the database, and keywords suggested by experts (refer Table 1). I used selected leading and supporting databases to acquire the articles either by using advanced searching methods - which is by using Boolean operator, phrase searching, truncation, wild card, and field code functions separately or by combining these searching techniques into full searching string. Manual searching techniques such as handpicking and snowballing were also employed.

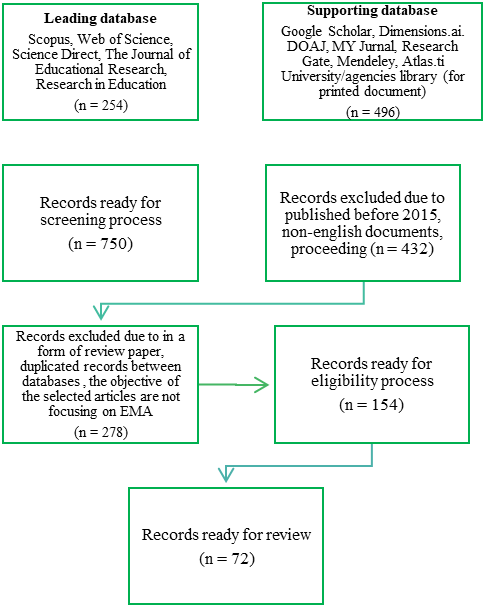

Scopus, Web of Science (WoS) and Science Direct were the databases used to identify articles and documents for the review, as suggested by Gusenbauer and Haddaway (2020). They confirmed that the three searching sources offer advanced searching function abilities, are multidisciplinary and they control articles quality. Further, in terms of database size, Scopus, WoS and Science Direct have over 70 million, 73 million and 15 million records respectively.

Other sources were also utilised as supporting database namely: Google Scholar, DOAJ, MY Jurnal, Research Gate and University/agencies library (for printed document). The supporting databases are important to gain additional sources of non-indexed journals or articles that are not available in the leading databases (Xiao & Watson, 2017). This measure is carried out following Bates et al. (2017) assertion that some databases may not be precise in reaching all related articles. Further, although the other five databases are supporting databases to the three leading ones, they have their own merits. For example, according to Gusenbauer and Haddaway (2020) Google Scholar database alone holds 389 million records and has the ability to recognise highly-cited papers effectively (Martin-martin et al., 2017). I administered Google Scholar search through Harzing’s Publish or Perish software. The software helped in managing the list of references saved through string search (Harzing & Van der Wal, 2008). The searching process of the databases resulted in 750 articles.

Screening process

The articles will automatically be selected by the databases via their sorting function based on the inclusion and exclusion criteria, depicted in Table 2. Some of the 750 articles went through the inclusion and exclusion process manually, as some of the databases sorting function were unavailable.

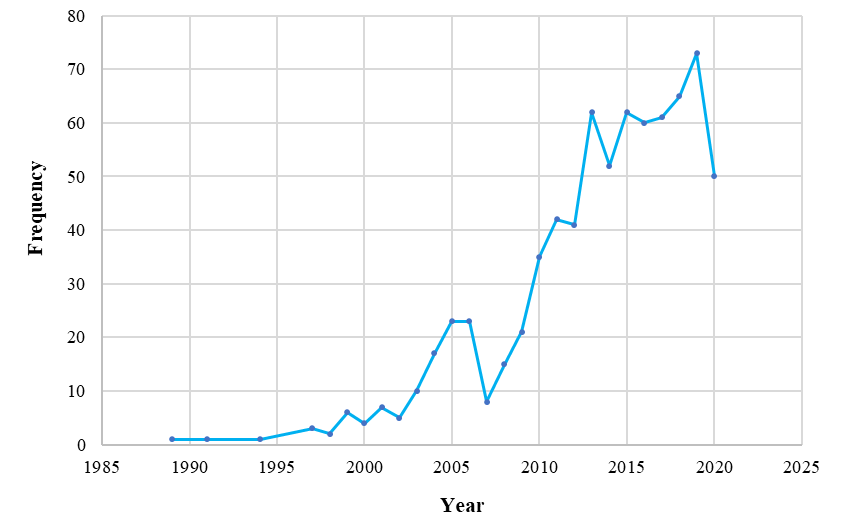

Okoli (2015) suggests for researchers to determine the range of period that they are able to review (here being 2015 to 2020). Nonetheless, Higgins and Green (2011) reminded that restriction on timeline publication should be activated only if it is known that related studies could only have been reported during a specific period. Figure 1 provides a snapshot of article frequency based on the systematic search strategy performed. The positive trend in number of articles provides evidence that the topic is gaining much attention, except for 2014 when the number of articles dropped to 52, but it picked up to 62 articles in 2015. The rising trend in the research of EMA implementation may be a result of research interests. Nonetheless, it might also be due to the release of special issues for the particular topic as identified by Schaltegger et al. (2013).

The current research covers literatures within 2015 to 2020 only, as reported in Table 2. In addition, only articles from journals, book, chapters in book and written articles in government agencies were considered to ensure quality of review. Apart from that, the search strategy also accepted articles published in the English language were included for review to avoid language barriers. This procedure omitted 596 articles for not adhering to the inclusion criteria. Only 154 articles remained went through the eligibility process.

Eligibility process

Based on the Figure 2, the title and abstract of the remaining 154 articles were manually skimmed through. An article’s content will be examined if further reading is needed to understand the content and view its relevance. The process excluded 82 articles in the form of review paper, duplicated records between databases and articles that focused on reporting, social accounting or auditing and non-English language. Finally, 72 selected articles were ready for review.

The final literature was then analysed to generate themes via natural language processing (NLP) with word cloud. This method is used to analyse existing research work (Rabiei et al., 2017), where repetitive words were picked up from the literature text gathered via SSS. Themes generated from the NLP process are discussed in the following section.

Results

The following presents some findings of literature on EMA practices in various themes, namely practices in the manufacturing industry, agriculture, hospitality, EMA tools used in industry, drivers and barriers to EMA implementation. The drivers and barriers will be discussed in each of the industry presented.

EMA practices in manufacturing

EMA practices in manufacturing industry were extensively researched between 2015 to 2020. Some companies were found to manage pollution prevention activities in order to fulfil legal requirements and due to stakeholder pressure (Yassin & Ali, 2020); contrasting to Ijeoma (2015) who discovered that the manufacturing firms were not pressured to incorporates environmentally friendly practices. However, Chowdhury and Uddin (2015) learnt that EMA system were not maintained in the tannery, paper, fertiliser, textile and paint manufacturing facilities that they examined.

It was also established that company size was not an important factor for EMA implementation, as compared to environmental strategy and culture (San et al., 2018). In contrast, Le and Nguyen (2019) claim that larger manufacturing companies in Vietnam display higher level of commitment than smaller companies. Literature further established manufacturing companies that adopted ISO14001 (environmental management system) displayed improvements in financial performance, increased production level and reduction in energy consumption and waste (San et al., 2018; Zamani & Ghaemmaghami, 2018). San et al. (2018) added manufacturing companies that disregarded environmental considerations in their operations faced production inefficiencies. With regards to ISO14001 certification, non-certified companies were reported to be active in incorporation environmental considerations in their decision-making similar to companies awarded with certification (Ong et al., 2016). Further, Ong et al. (2018) revealed that manufacturing companies took up ISO14001 certification for business and image reasons. Conversely, Wachira and Wang’ombe (2019) discovered less than half of the respondents (26%) in their research utilised EMA information for decision-making and companies that implemented EMA achieved significant reduction in environmental costs.

Another research of manufacturing companies in Malaysia discovered that government’s intervention is a driver that affects the intent and inclination of companies to implement EMA (Muhammad Jamil et al., 2015). They also concluded that financing of environmental activities did not deter EMA implementation as one would think. Another driver of EMA implementation is government intervention, as mentioned by Chathurangani and Hemathilake (2019) who that government intervention is significant in managing environmental issues. Regulatory compliance was also found to influence EMA practice as asserted by Wachira and Wang’ombe (2019). Further, stakeholder pressure and fulfilling legal requirements were other drivers of EMA implementation through management of pollution prevention activities (Yassin & Ali, 2020).

On the other hand, the negative attitude towards environmental requirements, lack of enforcement from inspectors and high level of corruption were found to be the barriers of EMA implementation in Egypt (Yassin & Ali, 2020). Further, Le and Nguyen (2019) also discovered there were limitations in reporting environmental costs and assessing environmental performance, as they were considered unimportant. The fact that there is no reporting of environmental costs, led companies to disregard environmental impact in their decision-making.

EMA practices in agriculture

Environmental issues relating to agricultural activities is a concern nowadays. While farmers are trying to monitor and control their agricultural and environmental costs, the rest of the world are scrutinising agricultural practice. It is important for agricultural players to improve and equip themselves with needed competence and technology to increase efficiency and reduce costs without burdening the environment. With the world population getting close to 9.7 billion in 2050 (Skaf et al., 2019), food demand will significantly increase. The significant increase in food demand and “intensive agricultural activities” (Skaf et al., 2019) may have a detrimental effect on the environment if agricultural players are indifferent, negligent and do not have expertise to manage and practice sustainably. The following are sample research by Chetthamrongchai et al. (2019), Skaf et al. (2019) and Tashakor et al. (2019) that provide empirical evidence from Thailand, Lebanon and Australia on agriculture and sustainability practices and implementing EMA.

Chetthamrongchai et al. (2019) for example, reported that Thailand attempt to mitigate environmental concerns through introducing agricultural extension service (AES) to agriculture players such as farmers. AES was found to negatively affect agricultural environmental costs at the onset because farmers had to pay for training and purchase of technology, but the cost incurred resulted in positive environmental effects in long run.

In another EMA research of the agricultural industry, a multi-criteria accounting framework was used to examine the type of agricultural production that would achieve the best environmental performance (Skaf et al., 2019). They saw a need to ensure that the limited resources are utilised efficiently and sustainably through estimating direct and indirect material resources consumed throughout the product or service life.

EMA implementation requires commitment from farmers especially to ensure its success and should not be driven by external entities because these farmers already understand the importance of environmental conservation (Tashakor et al., 2019). Farmers should be concerned about whether they have the required farm resources than be influenced by external opinions. In contrast, less environmentally friendly farmers were found to be driven by economic factors (such as technology, knowhow and funds) to implement EMA practices.

EMA practices in hospitality industry

EMA research on the service industry from developing countries is scarce (Gunarathne & Lee, 2015); especially ones that delve into design, development and use of environmental information for decision-making (Nyide, 2016). However, Gunarathne and Lee (2015) discovered from a research conducted at a hotel, that management accounting knowledge and expertise of using EMA information in decision-making had resulted in positive financial performance. The hotel applied selective EMA practices to reduce costs at a time when it was in a financial crisis. In addition, due to the success that they achieved from their first attempt, the hotel management extended EMA practice companywide. Stakeholder engagement was also found to be a factor for EMA success in the hotel. In another research of the hotel industry, Nyide and Lekhanya (2016a) discovered that water, energy and occupancy were the environmental costs being reported in the accounts, with energy efficiency projects and water management being most concentrated on.

In another hotel-based research, Nyide and Lekhanya (2016b) revealed that cost reduction and leadership commitment were drivers for EMA implementation. Apart from that, strict environmental regulations and stakeholder pressures (such as guests) were among the drivers of EMA practices in the hotel. They further asserted that lack of knowledge about EMA, an absence of appraisal system, lack of proper dissemination of information and inconsistent application of environmental technology across the company were among the internal barriers to EMA practice. Similar to previous research, lack of enforcement and support from the government were found to result in non-implementation.

EMA application investigated in the literature

EMA application by companies for decision-making purposes are diverse, such as material flow cost accounting (MFCA), environmental cost management accounting (ECMA), gross energy requirement (GER), emergy accounting, water management, carbon accounting and emissions accounting. The following are literature, investigating EMA application in companies as recorded from the systematic search strategy from 2015 to 2020.

As shown in the Table 3, the more popular tool investigated was MFCA. This is probably due to its ability to keep track of financial and non-financial implications in operations. Further, MFCA was established as ISO14051 in 2011 (Kokubu & Kitada, 2015), which solidify its effectiveness as an EMA tool.

MFCA for example, manages and monitors the use of energy, water and wastes both financially and non-financial. Nonetheless, other emerging issues being investigated and discussed are on emergy, carbon and emissions – and quite recently circular economy. Notwithstanding, these themes or issues are environmentally related and require attention.

Research on MFCA adoption and application in companies can be considered extensive, for example research conducted by Debnath (2017), Kokubu and Kitada (2015), Nyide (2016) and Sulong et al. (2015), to name a few.

Conclusion

The aims of the research were twofold. Firstly, it aims to conduct a systematic search strategy to uncover themes based on 2015 to 2020 literature that explain how EMA is implemented in companies and to discover its drivers and barriers.

Systematic search strategy has helped uncover the literature themes that looks into EMA implementation in different industries/ sectors in this research such as the manufacturing industry, agriculture and the hospitality sectors. In terms of industry, manufacturing, agriculture and hospitality were predominant. It was apparent that the industry players would only engage in EMA when they are convinced that it would lead to reduced costs. Further, it can be emphasized that some companies only would engage in EMA practice with governmental enforcement. Other players would only practice EMA with the influence of external parties such as people close to them or due to shareholders pressure.

Drivers for EMA implementations among others were: to adhere to government regulation and compliance (Chowdhury & Uddin, 2015; Le & Nguyen, 2019; Mohamad & Mohamed, 2018; Wachira & Wang’ombe, 2019). Other than that, cost reduction attempts were found to drive companies to implement EMA (Gunarathne & Lee, 2015; Marelli, 2015; Nyide & Lekhanya, 2016b; Wachira & Wang’ombe, 2019; Wahyuni et al., 2019). Apart from that, government-linked companies were seen to implement higher level of EMA implementation than their non-GLC counterparts (Huong et al., 2017).

Other than drivers, barriers to EMA implementation are varied. For example, absence of policies and regulations by the government (Debnath, 2017; Nyide & Lekhanya, 2016b) would impede the development and spread of EMA in countries. Prior research also discovered that the inability to appreciate the importance of EMA would not result in EMA implementation (Asiri et al., 2020; Doorasamy, 2015; Le et al., 2019; Muhammad Jamil & Mohamed, 2017). Apart from that, companies’ staff were also lacking in knowledge to structure related EMA procedures (Asiri et al., 2020; Doorasamy, 2015; Dumitru, 2018; Mokhtar et al., 2016), size of the organisation (Le & Nguyen, 2019). Finally, poor documentation was a reason for not implementing EMA (Mokhtar et al., 2015). Poor documentation was found to be partly barriers of EMA implementation as environmental related documentation were unavailable to support managerial evaluations. Further, management’s skepticism against environmental measurement tools further impede the diffusion of environmental related management accounting (Kokubu & Kitada, 2015). Another factor found to be a barrier to implementation is the perception that the exercise is time consuming as well as resistance to change (San et al., 2018). Inconsistent application of EMA technology was also considered as a barrier as only specific part of the company is granted full access whilst others in the same company, were not given the same attention (Nyide & Lekhanya, 2016b). These inconsistencies impede sharing of information across divisions to monitor and control of environmental activities. Further, lack of transparency in processes and incomplete documentation of environmental activities may delay full implementation of EMA in companies (Burritt et al., 2019).

The systematic search strategy has identified unchartered territories that can be further explored. For example, majority of the research on EMA implementation were conducted via questionnaire survey (based on closed ended questions). The research sample used was predominantly random selection, and focused on a particular industry (specifically manufacturing). Thus, it is recommended that future research would use other research method such as qualitative, to get a better perspective of the research findings. For example, an exploration of EMA practices in an agricultural perspective, will enrich literature on the current subject. Additionally, exploration based on qualitative case study has the ability to bring the researcher closer to the phenomenon and provide the opportunity for the researcher to better understand the phenomenon and would best serve as a medium to gather information from the perspective of the industry.

Acknowledgments

The author would like to convey her deepest gratitude to UNITEN’s iRMC for funding this research and providing an opportunity to share valuable research discoveries in this conference.

References

Asiri, N., Khan, T., & Kend, M. (2020). Environmental management accounting in the Middle East and North Africa region: Significance of resource slack and coercive isomorphism. Journal of Cleaner Production, 267, 121870.

Bates, G., Begley, E., Tod, D., Jones, L., Leavey, C., & Mcveigh, J. (2017). A systematic review investigating the behaviour change strategies in interventions to prevent misuse of anabolic steroids. Journal of Health Psychology, 1–18.

Bowe, C., & van der Horst, D. (2015). Positive externalities, knowledge exchange and corporate farm extension services; a case study on creating shared value in a water scarce area. Ecosystem Services, 15, 1–10.

Burritt, R., Hahn, T., & Schaltegger, S. (2002). Towards a comprehensive Framework for Environmental Management Accounting - Links between Business Actors and Environmental Management Accounting Tools. Australian Accounting Review, 12(2), 39–50.

Burritt, R., Herzig, C., Schaltegger, S., & Viere, T. (2019). Diffusion of environmental management accounting for cleaner production: Evidence from some case studies. Journal of Cleaner Production, 224, 479–491.

Chathurangani, H., & Hemathilake, D. (2019). Relationship Between Institutional Pressures and Environmental Management Accounting Adoption with Special Reference to Small and Medium Manufacturing Entities in Anuradhapura District. Iconic Research and Engineering Journals, 2(7), 84–93.

Chetthamrongchai, P., Foosirib, P., & Jermsittiparsert, K. (2019). Mitigating Agricultural Environment cost through Agricultural extension services: The Mediating role of Environmental Accounting. International Journal of Innovation, Creativity and Change, 7(2), 231–252.

Chowdhury, M. A. A., & Uddin, K. M. O. (2015). Areas of Corporate Environmental Accounting and its Practice in Manufacturing Industries: A Study on Some Selected Manufacturing Industries in Bangladesh. HRD Journal, 6(1), 27–42.

Debnath, S. (2017). Implementing environmental management accounting (EMA). Corporations and Sustainability, March, 28–48.

Doorasamy, M. (2015). Theoretical Developments in Environmental Management Accounting And The Role And Importance Of MFCA. Foundations of Management, 7, 37–52.

Dumitru, A. P. (2018). The Importance of Environmental Costs in the Current International Economic Context. Global Economic Observer, 6(1), 81–87.

Garcia, S., Cintra, Y., Torres, R. de C. S. R., & Lima, F. G. (2016). Corporate sustainability management: a proposed multi-criteria model to support balanced decision-making. Journal of Cleaner Production, 136, 181–196.

Gibassier, D. (2015). Implementing an EMA Innovation: The Case of Carbon Accounting. Corporate Carbon and Climate Accounting. https://link.springer.com/chapter/

Gunarathne, N., & Lee, K.-H. (2015). Environmental Management Accounting (EMA) for environmental management and organizational change an eco-control approach. Journal of Accounting and Organizational Change, 11(3), 362–383.

Gusenbauer, M., & Haddaway, N. R. (2020). Which academic search systems are suitable for systematic reviews or meta-analyses? Evaluating retrieval qualities of Google Scholar, PubMed, and 26 other resources. Res Syn Meth, 11, 181– 217.

Harzing, A. W. K., & Van der Wal, R. (2008). Google Scholar as a new source for citation analysis. Ethics in science and environmental politics, 8(1), 61-73.

Higgins, J. P., & Green, S. (Eds.). (2011). Cochrane Handbook for Systematic Reviews of Interventions (5.1). https://handbook-5-1.cochrane.org/

Huong, N. T. T., Indra, A., Thuc, V. T., & Tram, N. T. (2017). Factors Affecting Environmental Management Accounting: A Case of Companies in Vietnam. Proceedings of the 8th International Scientific Conference Finance and Performance of Firms in Science, Education and Practice, 789–801.

Ijeoma, N. (2015). Evaluation of Companies Environmental Practices in Nigeria. Social and Basic Sciences Research Review, 3(7), 349–364.

Kokubu, K., & Kitada, H. (2015). Material flow cost accounting and existing management perspectives. Journal of Cleaner Production, 108, 1279–1288.

Le, T. T., & Nguyen, T. M. A. (2019). Practice environmental cost management accounting: The case of Vietnamese brick production companies. Management Science Letters, 9, 105–120.

Marelli, A. (2015). The evolving role of environmental management accounting in internal decision-making: A research note. International Journal of Accounting, Auditing and Performance Evaluation, 11(1), 14–47.

Martin-martin, A., Orduna-malea, E., Harzing, A., & López-cózar, E. D. (2017). Can we use Google Scholar to identify highly-cited documents? Journal of Informetrics, 11(1), 152–163.

Mohamad, D., & Mohamed, B. (2018). Acceptance towards tourism development: The case of Perhentian Island. Planning Malaysia, 16(4), 117–129.

Mohd Khalid, F., Lord, B. R., & Dixon, K. (2012). Environmental Management Accounting Implementation in Environmentally Sensitive Industries in Malaysia. 6th NZ Management Accounting Conference, Palmerston North, October, 22–23.

Mokhtar, N., Jusoh, R., & Zulkifli, N. (2016). Corporate characteristics and environmental management accounting (EMA) implementation: evidence from Malaysian public listed companies (PLCs). Journal of Cleaner Production, 136, 111–122.

Mokhtar, N., Zulkifli, N., & Jusoh, R. (2015). The implementation of environmental management accounting and environmental reporting practices: A social issue life cycle perspective. International Journal of Management Excellence, 4(2), 515–521.

Muhammad Jamil, C. Z., & Mohamed, R. (2017). Antecedent Factors of Environmental Management Accounting Practice. International Journal of Economic Research, 16(2), 543–553.

Muhammad Jamil, C. Z., Mohamed, R., Muhammad, F., & Ali, A. (2015). Environmental Management Accounting Practices in Small Medium Manufacturing Firms. Procedia - Social and Behavioral Sciences, 172, 619–626.

Nyide, C. J. (2016). Material Flow Cost Accounting as a Tool for Improved Resource Efficiency in the Hotel Sector: A Case of Emerging Market. Risk Governance & Control: Financial Markets & Institutions, 6(4).

Nyide, C. J., & Lekhanya, L. M. (2016a). Environmental Management Accounting (EMA) in the developing economy: A case of the hotel sector. Corporate Ownership & Control, 13(4), 575–582.

Nyide, C. J., & Lekhanya, L. M. (2016b). Environmental Management Accounting practices: Major Control Issues. Corporate Ownership & Control, 13(3), 476–483.

Okoli, C. (2015). A Guide to Conducting a Standalone Systematic. Communications of the Association for Information Systems, 37.

Ong, J., Noordin, R., Kassim, A. W. M., & Jaidi, J. (2018). Factors influencing environmental management accounting practices in Malaysian manufacturing industry: Exploratory findings. ASM Science Journal, 11(Special Issue 3), 98–103. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85062479073&partnerID=40&md5=e01267e6e9d0cc79849e56b832874b22

Ong, T. S., Teh, B. H., Ng, S. H., & Soh, W. N. (2016). Environmental management system and financial performance. Institutions and Economies, 8(2), 26–52. https://www.scopus.com/inward/record.uri?eid=2-s2.0-84964253015&partnerID=40&md5=f5c5b49b05fdf3ac52aa8012452a8d52

Pacheco, J. R. R., Almeida1, C. M. V. B., Agostinho, F., Sevegnani, F., Giannetti, B. F., & Liu, G. (2019). Assessing footwear factories under emergy and material flow accounting tools after implementing cleaner production practices. Journal of Environmental Accounting and Management, 7(4), 429–448.

Qian, W., Hörisch, J., & Schaltegger, S. (2018). Environmental management accounting and its effects on carbon management and disclosure quality. Journal of Cleaner Production, 174, 1608-1619.

Rabiei, M., Hosseini-Motlagh, S.-M., & Haeri, A. (2017). Using text mining techniques for identifying research gaps and priorities: a case study of the environmental science in Iran. Scientometrics, 110(2), 815–842.

San, O. T., Heng, T. B., Selley, S., & Magsi, H. (2018). The relationship between contingent factors that influence the environmental management accounting and environmental performance among manufacturing companies in Klang Valley, Malaysia. International Journal of Economics and Management, 12(1), 205–232. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85050930307&partnerID=40&md5=661bcd0ade12f041b6428888be83e486

Schaltegger, S., Gibassier, D., & Zvezdov, D. (2013). Is environmental management accounting a discipline? A bibliometric literature review. Meditari Accountancy Research, 21(1), 4–31.

Skaf, L., Buonocore, E., Dumontet, S., Capone, R., & Franzese, P. P. (2019). Food security and sustainable agriculture in Lebanon: An environmental accounting framework. Journal of Cleaner Production, 209, 1025–1032.

Sulong, F., Sulaiman, M., & Norhayati, M. A. (2015). Material Flow Cost Accounting (MFCA) enablers and barriers: the case of a Malaysian small and medium-sized enterprise (SME). Journal of Cleaner Production, 108, 1365–1374.

Tashakor, S., Appuhami, R., & Munir, R. (2019). Environmental management accounting practices in Australian cotton farming: The use of the theory of planned behaviour. Accounting, Auditing and Accountability Journal, 32(4), 1175–1202.

Tsui, C. S. (2014). A literature review on environmental management accounting (EMA) adoption. Web Journal of Chinese Management Review, 17(3), 1-19.

Wachira, M. M., & Wang’ombe, D. (2019). The Application of Environmental Management Accounting Techniques by Manufacturing Firms in Kenya. Advances in Environmental Accounting & Management, 8, 69–89.

Wahyuni, W., Meutia, I., & Syamsurijal, S. (2019). The Effect of Green Accounting Implementation on Improving the Environmental Performance of Mining and Energy Companies in Indonesia. Binus Business Review, 10(2), 131.

Xiao, Y., & Watson, M. (2017). Guidance on Conducting a Systematic Literature Review. Journal of Planning Education and Research, 39(1), 93–112.

Yassin, M., & Ali, S. A. (2020). Survival of new institutional sociology theory: The case of environmental management accounting in the Egyptian context. International Journal of Customer Relationship Marketing and Management, 11(1), 50–63.

Zamani, M., & Ghaemmaghami, K. (2018). Investigating Environmental Accounting and its Role in Reducing Environmental Costs (Case Study: Iran Noubaft Textile Company). Journal of Accounting Finance and Auditing Studies (JAFAS), 4(4), 185–202.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

18 August 2023

Article Doi

eBook ISBN

978-1-80296-963-4

Publisher

European Publisher

Volume

1

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1050

Subjects

Multi-disciplinary, Accounting, Finance, Economics, Business Management, Marketing, Entrepreneurship, Social Studies

Cite this article as:

Khalid, F. M. (2023). Environmental Management Accounting Practices: A Review of the Literature. In A. H. Jaaffar, S. Buniamin, N. R. A. Rahman, N. S. Othman, N. Mohammad, S. Kasavan, N. E. A. B. Mohamad, Z. M. Saad, F. A. Ghani, & N. I. N. Redzuan (Eds.), Accelerating Transformation towards Sustainable and Resilient Business: Lessons Learned from the COVID-19 Crisis, vol 1. European Proceedings of Finance and Economics (pp. 186-198). European Publisher. https://doi.org/10.15405/epfe.23081.16