Accounting Information System and Organizational Effectiveness: Evidence From SMEs Manufacturing Companies

Abstract

Accounting Information System (AIS) is an accounting device that is directly linked to economic and financial outcome as well as productivity of small medium-sized companies. This study aims to investigate the impact of AIS on the organizational effectiveness of manufacturing company categorised under small medium enterprises (SMEs). Generally, it is crucial for manufacturing organizations to have an effective technology so that business operating activities can be well-managed. However, most organizations only focus on some parts of AIS, which could lead to the ineffective utilization of AIS. Thus, this study intended to determine the impact of AIS elements on organizational effectiveness, mainly manufacturing companies. In this study, the updated IS Success Model developed by DeLone and McLean was used as it thoroughly describes all the components in the AIS. Questionnaires were distributed to 827 companies and 213 questionnaires were successfully collected. Findings show that AIS elements comprising of System Quality, Information Quality, Service Quality and System Use have a significant influence on organizational effectiveness. Therefore, this indicates that implementation of AIS by manufacturing companies is important to increase organizational effectiveness.

Keywords: Accounting information system, organizational effectiveness, organizational performance, manufacturing companies, SMEs

Introduction

The emergence of Information Technology (IT) and increasing transparency of the financial sector in the new era has become the major driver in business operations and its performance (Doms et al., 2003). These cross-industry forces compel transformations that have significant economic and social effects on organizational effectiveness. Accounting Information System (AIS) is a tool that utilizes the information technology component to help a firm manage its economic-financial aspects (Alnajjar, 2017). The global economy’s rapid development reflected in rapid changes in the production process, development of IT, market competition and consumer sophistication have enlightened AIS’s role in effective management (Alnajjar, 2017). AIS’s function is vital in providing the support for economic decisions by contributing to the upgrading of a business organization’s value chain and improving its target performance (Qatanani & Hezabr, 2015). According to Chang (2001) firms tend to systematically customize their AIS design to support its strategies, believing that AIS has the capability to enhance organizational performance and facilitate strategic management. Furthermore, AIS can be used as a mechanism for generating the required business information by identifying, evaluating, and designing the dynamics that affect the firm’s financial state and activities (Özer & Uyar, 2010). AIS has important functions, such as collecting and recording data about activities; processing data and transforming it into information, helping users in decision making to plan and provide adequate controls for business assets (Amidu et al., 2011).

Organizations use the application of AIS and the consciousness of their importance based on the nature of the business (Abdallah, 2013). AIS is an important tool that supports manufacturing operations in the manufacturing industry. In addition to automating and securing the manufacturing business process, it helps to provide pertinent and responsive information for important decision at various layers of the organization's hierarchy. Malaysian manufacturing companies in the small medium enterprise (SMEs) category adopt information systems to boost the capabilities and efficiencies of their business operations. However, the limited resources possessed by SMEs for implementing information systems is one of the most significant obstacles in the adoption of information systems. A special grant has been provided by the Malaysian Government with numerous initiatives to assist Malaysian SMEs in the adoption of information system software. Consequently, the adoption of AIS can equip SMEs with the necessary capabilities and resources to achieve these goals. It was found that SMEs use the AIS do increase their firm performance product (Kharuddin et al., 2010)

Despite the usefulness and benefits of AIS, some manufacturing industries have declined its adoption, while some others have low levels of adoption. In addition, some firms that have adopted AIS do not know the benefits accruing from its adoption (Adenike & Michael, 2016). Furthermore, most organizations are not fully aware of the elements in the system. The function of each element is not fully understood by the management, and this leads to the ineffective application of AIS. An ineffective system that manages all the management transactions will cause problems for the company in the future. The transactions might not be fully recorded, mistakes might happen, data could be omitted, and numerous disputes might occur.

Therefore, this study aimed to examine the impact of AIS elements on organizational effectiveness. Each AIS element, which includes of System Quality, Information Quality, Service Quality and System Use, are further investigated to determine how they significantly affect the organization’s effectiveness and thus, to indicate how important it is for the management have a well implemented AIS in their business practice.

Literature review

Implementation of accounting information system in SMEs

Based on contemporary technology, it is crucial for organizations or any companies to be aware of the latest developments and improvements to contemporary technology so that they can compete and provide a better service or product to others (Hussein, 2011). It has become a survival factor for any organization, including SMEs, to have an effective AIS (Ortiz de Guinea et al., 2005). SMEs are vital to the economic growth process and play a significant role in the nation's production network. The success of some advanced economies is due to the important role of SMEs in the economy, since it contributes to over 98% of total establishments, 65% of employment and over 50% of the gross domestic product (Kharuddin et al., 2010). The information system is proven to aid the operation and enhancement of organizational performance since AIS has a huge impact on SMEs, either in industrialized or developing countries (Hussein, 2011). Ismail and Mat Zin (2009) found that Malaysian SMEs have poor control, and most companies make ad-hoc business decisions. According to Jamaludin and Mohamad Hasun (2007), the failure rate among SMEs is a little worrying. Findings demonstrate that most Bumiputra SMEs are still not aware of the importance of accounting information for their business. Some of them stated that they still use the traditional accounting method because they believe it is sufficient, besides lacking the funds to acquire and use that software in their organization. The deployment of AIS would allow a better accounting procedure, which imparts some positive effects on SME managers (Amidu et al., 2011). The organization should be ready to change its strategy at any time in order to match current developments and the environment, hence, enhancing organizational performance (Budiarto & Prabowo, 2015).

Organizational effectiveness

According to Malik et al. (2011), organizational effectiveness refers to how effectively an organization achieves its intended outcomes. It is an abstract concept that is essentially unmeasurable. Instead of measuring organizational effectiveness, the organization determines surrogate measures to represent it, which include items such as management efficiency, employee performance, core competencies, number of people served, type and size of population segment served. Moreover, Alhaji and Wan Yusoff (2012) stated that techniques to improve work motivation, organizational commitment, and effectiveness may differ based on type of task, organization, and individuals. Increased commitment will result in greater efficiency and outputs, which every organization needs to acquire.

Theoretical Framework and Hypothesis Development

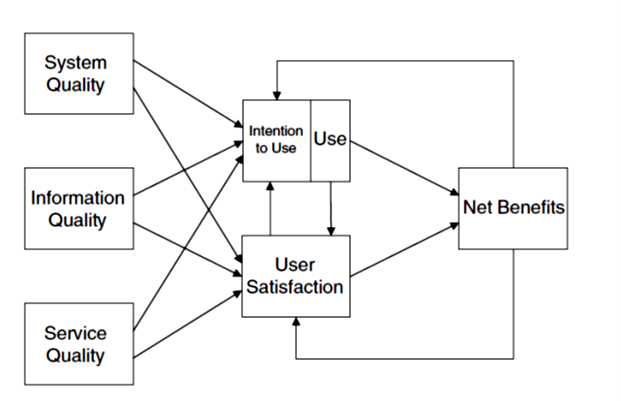

This study is conducted based on updated theory of Information System (IS) Success Model developed by DeLone and McLean (2003) which emphasizes on a comprehensive understanding of IS success by identifying, describing, and explaining the relationships among six variables with some modification from the original version, as illustrated in Figure 1 (Petter et al., 2008). Each variable has its own roles in measuring the information system. Figure 1 shows the modified IS Success Model made by DeLone and McLean (2003). One reason for the changes was innumerable critics of the old version mentioned in previous studies. The community seems to reject the original version due to its ignorance of emerging new economic activities (Chen & Cheng, 2009) as well as the lack of relevance to its adoption by current practices (Wang & Lios, 2008). Thus, this model is the most suitable for this research since it vividly describes all the components used for measuring information system dimensions.

Accounting information system and organizational effectiveness

The relationship between the accounting information system and organizational effectiveness is reflected in the hypotheses developed. The aim of developing the hypotheses is to illustrate whether it supports the relationship between Accounting Information System (AIS) and Organizational Effectiveness. In addition, AIS dimensions are measured by using four variables, namely System Quality, Information Quality, Service Quality and System Use.

System quality and organizational effectiveness

System quality is related to desirable characteristics in information system. For instant, simplicity of use, system adaptability, system dependability, and ease of learning (Petter et al., 2008). Al-Mamary et al. (2014) found that there is significant relationship between system quality and the acceptance of a system. Thus, the acceptance leads to an increase in the efficiency and effectiveness of organizational performance. Anggraeni and Winarningsih (2021) stated that quality of a well-designed accounting information system can produce quality accounting information. A good quality system that is better integrated, accessible, and flexible, tends to produce relevant, accurate, complete, and timely information. In addition, Grande et al. (2011) found that one of the advantages of using the AIS is that it enhances the speed of processing a task. Thus, the speed of processing a task, which is categorized as the quality of a system, is incredibly important, especially for a manufacturing company that aims to ensure a system’s efficiency that requires the recording of a lot of transactions. A system that possesses a speedy task processing system will be extremely useful to the organization compared to using the manual accounting system. Thus, the first research hypothesis is as stated below:

H1: There is a significant relationship between system quality of AIS and the organizational effectiveness.

Information quality and organizational effectiveness

Management often engages in numerous activities requiring high-quality and trustworthy data (Soudani, 2012). Information quality is a desirable characteristic of a system’s output (i.e., management report and web pages) (Petter et al., 2008). The information’s output should be relevant, understandable, accurate, complete and contain all the required elements to support the information needs (Al-Mamary et al., 2014). The system’s effectiveness critically depends on the quality of the information delivered (Xu, 2010). Key benefits of a company using AIS effectively includes better management of distance transactions, improved ability to react to changing environments, and a high level of competitiveness. Makau et al. (2017) concluded that information quality has significant influence on firm performance. It also found that firms need to ensure that their supply chain practices are aligned with information quality in order to increase business performance. In addition, Argyropoulou et al. (2018) found that information quality has a significant positive influence on innovation, marketing performance and financial performance. Hence, based on previous findings, the second research hypothesis is:

H2: There is a significant relationship between information quality of AIS and organizational effectiveness.

Service quality and organizational effectiveness

Information System (IS) service quality can be defined as the support quality provided to system users by the AIS department and IT support personnel (Petter et al., 2008). It is the degree of discrepancy between customers’ expectation and their perception of service performance (Gorla et al., 2010). For example, For instance, the staff's inherent responsiveness, accuracy, dependability, technical proficiency, and empathy. The service quality’s influence is evident from its impact on organizational performance. Gorla et al. (2010) found that the information’s service quality is related to the ability to provide immediate and high-quality services to users, enable firms to achieve a better performance. Moreover, Soudani (2012) explains that business organizations frequently employ AIS to provide decision support services. This might include the financial analysis conducted using AIS technology, which can produce numerous electronic documents for owners and managers (Vitez & Baligh, 2011). Thus, the third hypothesis is:

H3: There is a significant relationship between service quality of AIS and organizational effectiveness.

System use and organizational effectiveness

System use refers to the extent and the way employees and customers utilize the capabilities of an information system (Petter et al., 2008), such as the extent, purpose, and frequency of system usage. In addition, Cho (2007) revealed that managers tend to stimulate increased use of information systems in a business when they devote a huge number of resources to support information technology. The management could implement some incentive programs to encourage personnel to use an information system. Thus, employees are significantly more likely and prefer to use an information system in given circumstances. The entire business performance will also increase as a result of improvements in individual performance. Thus, the fourth hypothesis is:

H4: There is a significant relationship between system use of accounting information system and organizational effectiveness.

Research methods

Data collection and variables measurement

The study’s target population comprised Small Medium Enterprises (manufacturing companies) in Selangor. Focus was on the manufacturing industry as it has a strong influence on the country’s economy (Bank Negara, 2015). 98% of SMEs in this country provide approximately 65% of employment opportunities to Malaysian citizens, while contributing more than 50% of the Gross Domestic Product (GDP). Malaysian SMEs’ total contribution towards the GDP is valued at 47.3%. SMEs also have also been recognized as the backbone of the Malaysian economic due to its strong contribution and endogenous growth in the industry’s expansion and development (Kharuddin et al., 2010). In efforts to narrow the scope of this research, the Food and beverage sector was chosen as a more specific sector for this research due to its highest number of manufacturing companies in Malaysia compared to other sectors. Thus, respondents were randomly selected from a total of 827 SMEs (manufacturing companies) in the food and beverage sector in Selangor, Malaysia. Data were collected using questionnaires and the person directly in-charge of the accounting information system in the company was selected as a respondent and overall, 213 respondents were obtained for the final sample. The questionnaire was divided into three parts, consisting of Section A, B and C. Every section was detached at different parts to segregate the different types of information. Section A concerned the respondent’s demographic profile, Section B focused on assessing the accounting information through four variables, namely system quality, information quality, service quality and system’s use and Section C focused on assessing organizational effectiveness. Both dependent and independent variables were measured using the Likert Scale. The final results of the data analysis was calculated to determine the average score for each element. Data were gauged on a scale of one to five, starting with strongly disagree (score 1), disagree (score 2), neutral (score 3), agree (score 4) and strongly agree (score 5). The score of the data was derived by calculating the average score for each element.

Data Analysis

To examine the association between independent variables and organizational effectiveness or the dependent variable, a regression analysis was conducted. The following empirical models are used to test the hypotheses:

AP = β0 + β1SysQuality + β 2InfoQuality+ β 3ServQuality+ B4SysUse + e

Where,

OE=Organizational Effectiveness

β 1SysQuality=System Quality

β 2InfoQuality=Information Quality

β 3ServQuality=Service Quality

β 4SysUse=System use

e=Error term

Findings

Descriptive analysis

Table 1 depicts respondents’ backgrounds based on position, department, education level, experience of current position and total working experience. Out of 213 respondents, 3.80 percent are directors and majority (44.6 percent) of them are normal staff. Whereas 46 percent of the respondents were from other departments besides the accounting department, such as Human Resources (16.6 percent) or Finance departments. As for level of education, 39.9 percent possessed a Diploma and only 2.3 percent possessed a Postgraduate qualification. Based on years of experience at current position, majority (54.5% percent) of respondents had less than 3 years’ experience at the current position. Respondents with more than 10 years’ experience at the current position were only 6.6 percent. As for total working experience, 45.5 percent of respondents had less than 3 years total working experience, while 22.1 percent had 6 to 10 years total working experience.

Normality test of data (see Table 2) shows that data are not normal and therefore Spearman correlation is conducted for multicollinearity test. Data were transformed to normal scores to meet the requirement of linear regression (Young, 1998). Using normal scores has an advantage of producing results with accurate statistical features, as the significance threshold can be precisely calculated. In addition, the regression coefficients from the results are more interpretable (Field, 2013)

Correlation analysis

From correlation analysis (see Table 3), it shows that coefficient between variables were not exceed 0.8. Thus, the multicollinearity is not strong that would reduce the statistical power of regression (Gujarati, 1992).

Regression analysis

Multiple regression analysis as shown in Table 4, involving the independent variables and the dependent variable. The findings indicate a significant positive association of system quality towards organizational effectiveness in the SMEs (manufacturing companies). This might be because the accounting information system is well designed and implemented, thus, leading to relevant, accurate, complete and timely information (Anggraeni & Winarningsih, 2021). The results are also consistent with Gorla et al. (2010), that found significant positive influence of system quality towards acceptance of the system, leading to a positive impact on organizational effectiveness. According to Grande et al. (2011), quality of the AIS could expediate the processing task and thus, benefitting the manufacturing companies, which usually have innumerable transactions that need to be recorded within a short period of time. According to the results, it is proven that the AIS’s quality has enhanced the SMEs’ (manufacturing companies) organizational effectiveness. Therefore, Hypothesis 1 (H1), on the relationship of the system’s quality towards organizational effectiveness is supported.

Furthermore, the results indicate that the relationship between information quality and organizational effectiveness is also significant since the p-value is lower than 0.01. Hence, Hypothesis 2 (H2), regarding the relationship between information quality and organizational effectiveness, is accepted. This is consistent with Makau et al. (2017) and Argyropoulou et al. (2018), who found a significant influence imparted by information quality on firm performance, which highlights its importance in business practice. Furthermore, Soudani (2012) explained that good quality information is essential for a company as management is involved in various tasks, and the success of AIS depend on the accuracy of the data provided (Hongjiang Xu, 2010).

Similarly, results also shows that service quality significantly influences organizational effectiveness. Thus, Hypothesis 3 (H3), on the relationship of service quality towards organizational effectiveness, is proven. This finding is consistent with Gorla et al (2010), who found a positive influence by service quality on better organizational performance. This resulted from the system’s ability to provide prompt, accurate, relevant and high-quality service to users. In line with this statement, Megeid (2013) found that service quality has a positive influence on company performance because of its ability to increase customer satisfaction. Thus, management should concentrate on providing prompt and relevant IS service to its customers.

Finally, the result indicates that there is a significant relationship between system use and organizational effectiveness. Therefore, it can be concluded that Hypothesis H4, which states that there is a relationship between system use and organizational effectiveness, is accepted. This is consistent with Cho (2007), who found that utilization of the system could lead to better company performance as it enables an improvement in individual job performance. In addition, Jalagat and Al-Habsi (2017) also observed a positive relationship between system use and organizational performance, specifically concerning target achievement, financial performance, accountability and efficiency of operation.

Discussion and Conclusion

This study is aimed to examine the impact of the accounting information system on organizational effectiveness. The sample population comprised 213 SMEs (manufacturing companies) in the food and beverage industry in Selangor. Findings indicate that the independent variables and the dependent variable are strongly interrelated. There are significant positive influences from all variables. An increase in the utilization of AIS elements had directly improved organizational effectiveness. This study encourages SMEs to adopt AIS in order to enhance organizational effectiveness and competitiveness. Furthermore, manufacturing companies may be able to identify which AIS components contribute the most and least impact to the organization. Therefore, manufacturing companies should grab the opportunity to fully utilize components that provide significant benefits and avoid threats from components that might be deleterious to the company.

Limitation and Suggestion for Future Research

The study’s sample size focused only on SMEs (manufacturing companies) in the Food and Beverage sector located in Selangor. Future studies should expand the sample population to a wider setting as this allows for a wider generalization of the findings. For example, instead of focusing on the manufacturing sector, future research should focus on other industries, such as service, construction or mining industries, which adopt AIS tools in their operation. Thus, a larger sample size allows for more reliable data and more significant findings.

Acknowledgments

Authors would like to thank IRMC of UNITEN for awarding Pocket Grant for this research.

References

Abdallah, A. A. J. (2013). The Impact of Using Accounting Information Systems on The Quality of Financial Statements Submitted to The Income and Sales Tax Department in Jordan. European Scientific Journal, 1, 41-48

Adenike, A., & Michael, A. (2016). Effect of Accounting Information System Adoption on Accounting Activities in Manufacturing Industries in Nigeria.

Alhaji, I. A., & Wan Yusoff, W. F. (2012). Does Motivational Factor Influence Organizational Commitment and Effectiveness? A review of literature. Journal of Business Management and Economics, 3(1), 1-9.

Al-Mamary, Y. H., & Shamsuddin, A., & Nor Aziati, A. H. (2014). The Relationship between System Quality, Information Quality, and Organizational Performance, International Journal of Knowledge and Research in Management & E-Commerce, 4(3), 07-10.

Alnajjar, M. I. M. (2017). Impact of Accounting Information System on Organizational Performance: A Study of SMEs in the UAE. Global Review of Accounting and Finance, 8(2), 20-38.

Amidu, M., Effah, J., & Abor, J. (2011). E-Accounting Practices Among Small & Medium Enterprises in Ghana. Journal of Management Policy & Practice, 12(4), 146-155.

Anggraeni, A. F., & Winarningsih, S. (2021). The effects of accounting information system quality on financial performance. Economic Annals-XXI, 193(9-10), 128-133.

Argyropoulou, M., Reid, I., Wilkins, P., & Loannou, G. (2018). Information Quality, Reporting and Organisational Performance. 22nd Proceedings of 22nd EurOMA Conference, Neuchâtel, Switzerland.

Bank Negara. (2015). BNM National Summary Data Page.

Budiarto, D. S., & Prabowo, M. A. (2015). Accounting Information Systems Alignment and SMEs Performance: A Literature Review. International Journal of Management, Economics and Social Sciences, 4(2), 58-70.

Chang, Y. W. (2001). Contingency Factors and Accounting Information System Design in Jordanian Companies. Journal of Accounting Information System, 8, 1-16.

Chen, C. T., & Cheng, H. L. (2009). A Comprehensive Model for Selecting Information System Project Under Fuzzy Environment. International Journal of Project Management, 27(4), 389-399.

Cho, V. (2007). A Study of the Impact of Organizational Learning on Information System Effectiveness. International Journal of Business and Information, 2(1), 127-158.

DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information systems success: a ten-year update. Journal of management information systems, 19(4), 9-30.

Doms, M. E., Jarmin, R. S., & Klimek, S. D. (2003). IT Investment and Firm Performance in U.S Retail Trade, 1-17.

Field, A. (2013). Discovering statistics using SPSS for Windows. SAGE Publications Ltd.

Gorla, N., Somers, T., & Wong, B. (2010). Organizational impact of system quality, information quality, and service quality. Journal of Strategic Information Systems, 19, 207–228.

Grande, E. U., Estebanez, R. P., & Colomina, C. M. (2011). The impact of Accounting Information Systems (AIS) on Performance Measures: Empirical Evidence in Spanish SMEs. The International Journal of Digital Accounting Research, 11, 25-43.

Gujarati, D. (1992). Essentials of Econometrics. McGraw-Hill.

Hussein, A. M. (2011). Use Accounting Information System As Strategic Tool To Improve SMEs' Performance in Iraq Manufacturing Firms. A Thesis of College of Business Master of Science (International Accounting), 1-27.

Ismail, N. A., & Zin, R. M. (2009). Usage of Accounting Information Among Malaysian Bumiputra Small and Medium Non-Manufacturing Firms. Journal of Enterprose Resource Planning Studies, 2009(2009), 1-7.

Jalagat, R., & Al-Habsi, N. (2017). Evaluating the impacts of it usage on organizational performance. European Academic Research, 5(9), 5111-5164.

Jamaludin, Z., & Mohamad Hasun, F. (2007). The Importance of Staff Training to the SMEs Performance. Proceedings of 2nd International Colloquium on Business and Management. Bangkok.

Kharuddin, S., Ashhari, Z. M., & Nassir, A. M. (2010). Information System and Firms' Performance: The Case of Malaysian Small Medium Enterprises. International Business Research, 3(4), 28-35.

Makau, S., Lagat, C., & Bonuke, R. (2017). The Role of Information Quality on the Performance of Hotel Industry in Kenya. European Scientific Journal, 13, 20.

Malik, M. E., Ghafoor, M. M., & Naseer, S. (2011). Organizational Effectiveness: A Case Study of Telecommunication and Banking Sector of Pakistan. Far East Journal of Psychology and Business, 2(1), 37-48.

Megeid, N. S. A. (2013). The impact of service quality on financial performance and corporate social responsibility: Conventional versus Islamic banks in Egypt. International Journal of Finance and Accounting, 2(3), 150-163.

Ortiz de Guinea, A., Kelley, H., & Hunter, M. G. (2005). Information Systems Effectiveness in Small Businesses: Extending a Singaporean Model in Canada. Journal of Global Information Management, 13(3), 55-79.

Özer, G., & Uyar, M. (2010). Data Quality in Accounting Information Systems and Reflections on Financial Reports. The 9th National Management Congress, 310-320.

Petter, S., DeLone, W., & McLean, E. (2008). Measuring Information Systems Success: Models, Dimensions, Measures, and Interrelationships. European Journal of Information Systems, 17, 236-263.

Qatanani, K. M., & Hezabr, A. A. (2015). The Effect of Using Accounting Information Sytems to Improve The Value Chain in Business Organizations - Empirical Study. European Journal of Accouting Auditing and Finance Research, 3(6), 1-11.

Soudani, S. N. (2012). The Usefulness of an Accounting Information System for Effective Organizational Performance. International Journal of Economics and Finance, 4(5), 136-145.

Vitez, O., & Baligh, H. H. (2011). Organization Structures: Theory and Design, Analysis and Prescription. Information and Organization Design Series. Springer.

Wang, Y. S., & Lios, Y. W. (2008). Assessing E-Government Systems Success: A Validation Of The Delone and Mclean Model Of Information Systems Success. Government Information Quarterly, 25, 717-733.

Xu, H. (2010). Data Quality Issues For Accounting Information Systems Implementation: Systems, Stakeholders and Organizational Factors. Journal of Technology Research, 1-11.

Young, S. (1998). The determinants of managerial accounting policy choice: Further evidence for the UK. Accounting and Business Research, 2, 131-143.

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

18 August 2023

Article Doi

eBook ISBN

978-1-80296-963-4

Publisher

European Publisher

Volume

1

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1050

Subjects

Multi-disciplinary, Accounting, Finance, Economics, Business Management, Marketing, Entrepreneurship, Social Studies

Cite this article as:

Johari, N. H., Khairudin, N. N., Mohd Rasidi, N., Yuhana, I. S., & Norbadirim, N. A. (2023). Accounting Information System and Organizational Effectiveness: Evidence From SMEs Manufacturing Companies. In A. H. Jaaffar, S. Buniamin, N. R. A. Rahman, N. S. Othman, N. Mohammad, S. Kasavan, N. E. A. B. Mohamad, Z. M. Saad, F. A. Ghani, & N. I. N. Redzuan (Eds.), Accelerating Transformation towards Sustainable and Resilient Business: Lessons Learned from the COVID-19 Crisis, vol 1. European Proceedings of Finance and Economics (pp. 108-119). European Publisher. https://doi.org/10.15405/epfe.23081.10